INTRODUCTION

Money is the most important discovery of modern times. It is very difficult to imagine the modern economic life without money. It is the basic necessity of all economies.

BARTER SYSTEM

Before money was invented, the primitive world’s trade was carried out according to the barter system of exchange.

MEANING OF BARTER EXCHANGE

In the beginning of civilization, human needs were simple and limited. People used to exchange goods with each other to satisfy their wants. Barter Exchange refers to exchange of goods for goods. An economy, where there is a direct barter of goods and services, is called a ‘Barter Economy’ or ‘C-C Economy’ (where C stands for commodity).

Limitations of Barter Exchange

The major limitations of Barter Exchange are:

- Lack of Double Coincidence of Wants:- Barter system can work only when both buyer and seller are ready to exchange each other’s goods. For example, A can exchange goods with B only when A has what B wants and B has what A wants. However, such double coincidence is very rare.

- Lack of Common Measure of Value – In the barter system, all commodities are not of equal value and there is no common measure (unit) of value of goods and services, in which exchange ratios can be expressed. For Example- If A has wheat and B has rice, then it is difficult to decide, how much wheat is needed to exchange with one kilogram of rice. In the absence of common measure, the exchange ratio is fixed randomly, in which one of the party generally sufferes.

3. Lack of Standard of Deferred Payment – Under barter system, contracts involving future payments or credit transactions cannot take place with ease

because of following reasons:

- The borrower may not be able to arrange goods of exactly same quality at the time of repayment.

- There may be conflicts regarding which specific commodity is to be used for repayment.

4. Lack of Store of Value – Under barter system, it is difficult for people to store wealth for future use because:

- Most of the goods (like wheat, rice, vegetables, etc.) do not possess durability, i.e. their quality deteriorates with passage of time.

FUNCTIONS OF MONEY

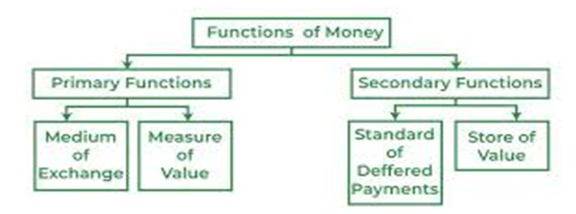

The function of money can be broadly categorized under two heads:

- Primary Functions (Main or Basic Functions)

- Secondary Functions (Subsidiary or Derivative Functions)

- Primary Functions – Primary functions include the most important functions of money, which it must perform in every country. These are:

(i) Medium of Exchange – Money, as a medium of exchange, means that it can be used to make payments for all transactions of goods and services. It is the most essential function of money. Money has the quality of general acceptability. So, all exchanges take place in terms of money.

- This function has removed the major difficulty of lack of double coincidence of wants and inconveniences associated with the barter system.

- Use of money allows purchase and sale to be conducted independently of one another.

(ii) Measure of Value (Unit of Value) – Money as a measure of value means that money works as a common denomination, in which values of all goods and services are expressed.

- By reducing the value of all goods and services to a single unit (i.e. price), it becomes very easy to find out the exchange ratios between them and comparing their prices.

- This function facilitates maintenance of business accounts, which would be otherwise impossible.

2. Secondary Functions – These refer to those functions of money are supplementary to the primary functions. These functions are derived from primary functions and , therefore, they are also known as’ Derivative functions.

The major secondary functions are:

(i) Standard of Deferred Payments – Money as a standard of deferred payments means that money acts as a ‘standard’ for payments, which are to be made in future. Every day, millions of transactions take place in which payments are not made immediately.

This function of money is significant because:

- Money as a standard of deferred payments has simplified the borrowing and lending operations.

- It has led to the creation of financial institutions.

(ii) Store of Value (Asset Function of Money) – Money as a store of value means that money can be used to transfer purchasing power from present to future. Money is a way to store wealth. Although wealth can be stored in other forms also, but money is the most economical and convenient way.

Money as store of value has the following advantages:

- Money is available in fractional denomination, ranging from Rs.1 to Rs.500.

- Money is easily portable. So, it is easy and economical to store money as its storage does not require much space.

Money has overcome the drawbacks of Barter System

- Medium of Exchange – As a medium of exchange, money has removed the major difficulty of lack of double coincidence of wants in barter system. A buyer can buy goods through money and a seller can sell goods for money.

- Measure of value – Money is the measuring and rod which expresses the value of other commodities. It becomes easier to compare the relative values of any two commodities.

- Store of value – Under Barter system, it is very difficult to store goods for future use. Most of the goods are perishable and their storage requires huge space and transportation cost. But, money can be easily stored for future use.

- Standard of deferred payments – Barter system lacks suitable standard of deferred payments which creates difficulty in credit transactions. Borrower may not be able to arrange goods of exactly the same quality at the time of repayment.

DEFINITION OF MONEY

Money is anything which is generally accepted as a medium of exchange, measure of value, store of value and means for standard of deferred payment.

- The term ‘money’ is used to cover all such things like coins, currency notes, cheques, etc., which are used to conduct business transactions and settlement of business claims.

Legal Definition of Money – Money is what the low says is money. So, anything which the government declares as money is money. On the basis of legal recognition, money is of two kinds:

(i) Legal Tender Money – Money which can be legally used to make payment of debts or other obligations is termed as legal tender money. A creditor is obliged by law to receive such money in payment of debt du rot him. Legal tender money is of two kinds:

- Limited Legal Tendar – It refers to that from of legal tender money, which can be paid in discharge of a debt up to a certain limit. In India, coins are limited legal tender. For example – as per Coinage Act, 2011, coins shall be a legal tender in case of coin of any denomination not lower than one rupee, for any sum not exceeding Rs.1,000.

- Unlimited legal Tender – It refers to that from of legal tender money, which can be paid in discharge of a debt of any amount. Legal action can be taken against a person who refuses to accept this money. In India, paper notes are unlimited legal tender.

(ii) Non-Legal Tender Money or Optional Money – It refers to that form of money, which is generally accepted, but legally, one is not bound to accept it. For example – cheques, bank drafts, bills of exchange, etc. do not have legal backing and their acceptance is totally optional.

“Cryptocurrency, crypto-currency or crypto is a digital or virtual currency which uses cryptography to secure transactions. It works as a medium of exchange through a computer network and does not rely on any central authority, such as government or bank, to verify transactions. In India, it has not been accorded the status of legal tender.”

Bank Money – Bank Money refers to demand deposits created by the commercial banks. These deposits are repayable by the banks on demand. It must be notes that bank money is a Non-Legal Tender Money or Optional Money.

MONEY SUPPLY

Money Supply refers to total valume of money held by public at a particular point of time in an economy.

Feature of Money Supply

- It includes ‘Money held by Public only’. The term ‘public’ signifies the money-using sector, i.e. individuals and business firms. It does not include Money-Creating Sector (or Producers/Suppliers of Money), i.e. Government and Banking System as cash balances held by them do not come into actual circulation in the country.

- It is a Stock Concept, i.e. it is concerned with a particular point of time.

Components of Money Supply

The two main components of money supply are:

- Currency with Public – It consists of paper notes and coins held by the public. It is the most liquid of all assets and includes coins of denominations of Rs.20, Rs.10, Rs.5, Rs.2, Rs.1 etc. and paper notes of denominations like Rs.500, RS.200, Rs.100 etc.

- Currency Money is also termed as ‘Fiat Money’. Fiat Money is defined as the money which is under the fiat or order from the government to act as money, i.e. under law, it must be accepted for all debts.

- It is also termed as ‘Legal Tender Money’ as it can be legally used to make payment of debts or other obligations.

2. Demand Deposits with Banks – It refers to demand deposits (or Bank Money) of the public with the commercial banks. Demand deposits are the deposits, which can be enchased by issuing cheques at any time by the account holders.

- Only Net Demand Deposits are included – It must be noted that demand deposits are taken on net basis, i.e., Inter-bank deposits are excluded. Inter-bank deposits are the deposits held by banks on behalf of other banks.

- Term Deposits are not included – While calculating M1 Measurement of money supply, only demand deposits are considered as a part of money supply and not the Term Deposits. (Demand Deposits = Saving Accountj Deposits + Current Account Deposits)

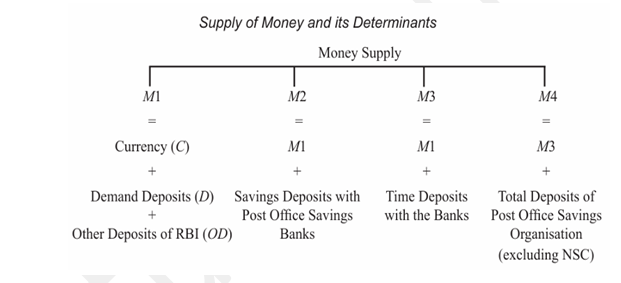

Measures of Money Supply

Till 1967-68, Reserve Bank of India (RBI) used only the narrow measure of money supply. But, since 1977, four alternative measures of money supply (M1, M2, M3 and M4) have been evolved:

- M1 – It is the first and basic measure of money supply. M1 is the most liquid measure of money supply as all its components are easily used as a medium of exchange.

M1 = Currency & coins with public + Demand Deposits of Commercial Banks + Other Deposits with RBI

- M2 – It is broader concept of money supply as compared to M1. In addition to M1, it also includes savings deposits with post office saving bank.

M2 = M1 + Savings Deposits with Post Office Saving Bank

- M3 – This concept is broader as compared to M1. In addition to M1, It also includes net time deposits.

M3 = M1 + Net Time Deposits with Banks

- M4 – This measure includes total deposits with post office saving bank in addition to M3.

M4 = M3 + Total Deposits with Post Office Saving Bank (Excluding NSC)

Importance Facts about Money Supply

- The four measures of money supply represent different degrees of liquidity, with M1 being the most liquid and M4 being the least liquid.

- M3 is widely used as a measure of money supply and it is also known as ‘aggregate monetary resources of the society’.

- M1 and M2 are generally known as narrow money supply concepts, whereas, M3 and M4 are known as brad money supply concepts.

- Reserve Bank of India (RBI) releases data on money supply in India.

What is High Powered Money (H)?

High Powered Money is money produced by the RBI and the government. It consists of two things: (i) currency held by the public; and (ii) Cash reserves with the banks.

‘Money (M)’ Vs ‘High Powered Money (H)’

- Money consists of currency and demand deposits, while ‘High Powered Money’ consists of currency and cash reserves with banks. It means, ‘Currency held by the public’ is common in both of them. The only difference is that ‘Money ‘ includes demand deposits of banks, while ‘High Powered Money’ includes cash reserves with the banks.

- ‘H’ is high-powered as compared to ‘M’ because cash reserves (part of H) serve as the actual base for the generation of demand deposits.

Short Answer Type Questions

- State the limitations of Barter Exchange.

Answer: The main limitations of Barter Exchange are:

- Lack of double coincidence of wants.

- Lack of a common measure of value.

- Difficulty in storing wealth or value.

- Lack of standard for deferred payments.

- Difficulty in indivisibility of certain goods.

2. Explain “difficulty in storing wealth” problem faced in the barter system of exchange.

Answer: Under the barter system, wealth was stored in the form of physical goods like grain, cattle, or cloth. These goods were perishable and could decay over time. Moreover, storing such goods required huge space and involved high maintenance costs. It was difficult to carry this wealth from one place to another compared to modern money.

3. Briefly explain any two functions of money.

Answer:

1. Medium of Exchange: Money acts as an intermediary for all transactions, allowing people to buy and sell goods without the need for a double coincidence of wants.

2. Measure of Value: Money serves as a common unit in which the values of all goods and services are expressed, making it easy to compare prices.

4. Explain “store of value” function of money.

Or – Give the meaning of money. Explain the ‘store of value’ function of money.

Or – Explain the significance of ‘Store of Value’ function of money.

Answer: Store of value means that money can be held and used in the future to purchase goods and services. Money is a convenient way to store wealth because it is easily portable, has high liquidity, and is generally stable in value compared to perishable goods.

5. State the four functions of money. Explain any one of them.

Answer: The four functions are Medium of Exchange, Measure of Value, Standard of Deferred Payments, and Store of Value. Explanation of Medium of Exchange: It is the primary function of money. It means money is used as a means to pay for goods and services. It removes the major hurdle of the barter system, which was the requirement of finding someone who has exactly what you want and wants exactly what you have.

6. What is ‘barter’? Explain ‘standard of deferred payment’ function of money.

Or – Explain the ‘standard of deferred payment’ function of money.

Or – Explain the significance of the ‘Standard of Deferred Payment’ function of money.

Answer: Barter is a system of exchange where goods are directly exchanged for other goods without the use of money. Standard of Deferred Payment: This means money acts as a unit in which future payments like loans and interest are settled. It is difficult to make future payments in terms of goods because their quality or value might change over time, but money remains a reliable unit for long-term contracts.

7. Discuss the meaning of: (i) Currency and coins with Public, (ii) Demand deposits held by commercial banks.

Answer:

(i) Currency and coins with Public: It includes all the paper notes and coins held by the people of a country at a particular point in time for day-to-day transactions.

(ii) Demand deposits: These are the deposits in commercial banks that can be withdrawn by the depositor at any time by writing a check. These are treated as money because they are easily used for payments.

8. Give the meaning of: (i) Barter Exchange; (ii) Money; (iii) Money Supply.

Answer:

(i) Barter Exchange: A system where goods are traded for goods.

(ii) Money: Anything that is generally accepted as a medium of exchange, measure of value, store of value, and standard of deferred payments.

(iii) Money Supply: The total stock of money held by the public at a particular point in time.

9. How does money solve the problem of double coincidence of wants?

Answer: In a barter system, exchange is only possible if two people want exactly what the other possesses. Money acts as an intermediary. A person can sell their goods for money and then use that money to buy whatever they need from anyone else. This separates the acts of sale and purchase.

10. Explain the ‘unit of account’ function of money.

Answer: Unit of account means that money acts as a common denominator. Just as we measure length in meters, we measure the value of all goods and services in money terms. This allows for the maintenance of proper accounting records and easy comparison of values.

11. Explain the ‘medium of exchange’ function of money.

Answer: Money as a medium of exchange means it is used to make payments for all transactions of goods and services. It removes the need for double coincidence of wants and makes the exchange process smooth and efficient.

12. Explain the ‘store of value’ function of money. How has it solved the related problem created by barter?

Answer: Store of value means people can save their wealth in the form of money for future use. In barter, storing wealth in goods was difficult due to perishability and high storage costs. Money is durable and takes less space, solving these problems.

13. Explain the ‘medium of exchange’ function of money. How has it solved the related problem created by barter?

Answer: Money solves the lack of double coincidence of wants by acting as a common medium. In barter, you had to find a specific person to trade with. With money, you can sell to anyone and buy from anyone.

14. Explain the ‘unit of account’ function of money. How has it solved the related problem created by barter?

Answer: In barter, there was no common unit to measure value. Money provides a single unit (like Rupees) to express the price of all goods, making calculation and accounting easy.

15. Explain the ‘standard of deferred payment’ function of money. How has it is solved the related problem created by barter?

Answer: This function allows for future payments. In barter, it was hard to return a loan in goods because the quality could differ. Money is a stable unit, making borrowing and lending simple.

16. Explain the concept of money supply.

Answer: Money supply is a stock concept. It refers to the total amount of money circulating in an economy among the public at a specific point in time.

17. Define money supply and explain its components.

Answer: Money supply is the total stock of money held by the public. Its components under

M1 are:

- Currency and Coins with the public.

- Demand Deposits with commercial banks.

- Other deposits with the Central Bank.

Long Answer Type Questions

- Discuss the limitations of Barter Exchange.

Answer: Barter system refers to the direct exchange of goods for goods. Its limitations are:

- Lack of Double Coincidence of Wants: It requires that both parties must have exactly what the other person needs. Finding such a match is very difficult.

- Lack of Common Measure of Value: There is no common unit to express the value of different goods. It is hard to decide exchange ratios.

- Lack of Standard for Deferred Payments: Making future payments in terms of goods is difficult because the quality or value of goods may change.

- Difficulty in Storing Wealth: Many goods are perishable and require a lot of space to store. This makes it hard to save.

- Problem of Indivisibility: Certain goods cannot be divided into smaller parts without losing their value, like a live animal.

2. Explain any two functions of money.

Answer:

- Medium of Exchange: Money acts as an intermediary in transactions. It allows people to sell their products for money and buy whatever they want. This removes the problem of double coincidence of wants.

- Store of Value: Money can be kept for future use without the fear of it getting spoiled. It is a convenient way to store wealth because it is liquid and has low storage costs.

3. Describe the following functions of money: (a) Medium of exchange; (b) Standard to deferred payment.

Answer:

(a) Medium of Exchange: Money is used as a means of payment for all transactions. It provides a common platform for exchange, separating the acts of buying and selling.

(b) Standard of Deferred Payment: Money acts as a unit in which loans and future settlements are made. It is a stable unit for long-term contracts compared to goods.

4. Explain (a) store of value & (b) measure of deferred payments function of money.

Answer:

(a) Store of Value: Money serves as an asset that can be used to transfer purchasing power from the present to the future. It allows individuals to save current income for future needs.

(b) Standard of Deferred Payments: This function makes credit transactions possible. It provides a reliable way to settle debts. Since money value is relatively stable, it is universally accepted for future payments.

5. How does money overcome the drawbacks of barter exchange?

Answer: Money overcomes barter drawbacks by:

- Providing a Medium of Exchange to eliminate double coincidence of wants.

- Acting as a Measure of Value to provide a common unit for prices.

- Serving as a Store of Value to make saving wealth easier.

- Acting as a Standard of Deferred Payment to facilitate credit and future settlements.

6. What is meant by ‘money supply’? Discuss, in brief, the various constituents of money supply.

Answer: Money supply is the total stock of money held by the public at a specific point in time. According to the M1 measure, its constituents are:

1. Currency and Coins with the Public: Paper notes and coins held by households and businesses.

2. Demand Deposits with Commercial Banks: Deposits in savings and current accounts that can be withdrawn at any time using checks.

3. Other Deposits with RBI: Deposits of international organizations like IMF and foreign central banks held with the RBI.

7. Explain the concepts of: (i) Currency and coins with Public; (ii) Demand deposits held by commercial banks.

Answer:

(i) Currency and coins with Public: This is the most liquid part of money supply. It consists of the legal tender issued by the government or central bank that is in circulation among the people.

(ii) Demand deposits held by commercial banks: These are deposits that people keep in bank accounts and can be withdrawn on demand without any prior notice. They are widely accepted for making payments through check facilities.