COMMERCIAL BANK

Commercial bank is an institution which performs the function of accepting deposits, granting loans and making investments, with the aim of earning profits. State Bank of India (SBI), Punjab National Bank (PNB), Bank of Baroda, Canara Bank are some example of Commercial Banks in India.

FUNCTIONS OF A COMMERCIAL BANK

The functions performed by commercial banks can be broadly categorized under two heads:

(i) Primary Function; (ii) Secondary Functions.

- Primary Functions

Commercial banks perform two primary functions:

- Accepting Deposits – It is the most important function of commercial banks. They accept deposits in several forms according to requirements of different sections of the society. The main kinds of deposits are:

(i) Current Account Deposits: These deposits refer to those deposits which are repayable by the banks on demand.

- Such deposits are generally maintained by businessmen with the intention of making transactions with such deposits.

- They can be drawn upon by a cheque without any restriction.

(ii) Fixed Deposits or Time Deposits or Term Deposits: Fixed deposits refer to those deposits, in which the amount is deposited with the bank for a fixed period of time.

- Such deposits do not enjoy chequable facility.

- These deposits carry a high rate of interest.

2. Advancing of Loans – The deposits received by banks are not allowed to remain idle. So, after keeping certain cash reserves, the balance is given to needy borrowers & interest is charged from them.

- Cash Credit: Cash credit refers to a loan given to the borrower against his current assets like shares, stocks, bonds, etc. A credit limit is sanctioned and the amount is credited in his account.

- Demand Loans: Demand loans refer to those loans which can be recalled on demand by the bank at any time. The entire sum of demand loan is credited to the account and interest is payable on the entire sum.

- Short-term Loans: They are given as personal loans against some collateral security. The money is credited to the account of borrower and the borrower can withdrew money from his account and interest is payable on the entire sum of loan granted.

II. Secondary Functions

In addition to primary functions, commercial banks also perform the following secondary functions:

(i) Overdraft facility – It refers to a facility in which a customer is allowed to overdraw his current account upto an agreed limit. This facility is generally given to respectable and reliable customers for a short period.

(ii) Discounting Bills of Exchange – It refers to a facility in which the holder of a bill of exchange can get the bill discounted with the bank before the maturity. After deducting the commission, bank pays the balance to the holder. On maturity, bank gets its payment from the party which had accepted the bill.

(iii) Agency functions – Commercial banks also perform certain agency functions for their customers. For these services, banks charge some commission from their clients. Some of the agency functions are:

- Transfer of Funds

- Collection and Payment of Various items

- Purchase and Sale of Foreign Exchange

- Purchase and Sale of Securities

- Income Tax Consultancy

- Trustee and Executor

- Letter of Reference

(iv) General Utility Functions

Commercial banks render some general utility services like

- Locker Facility

- Traveler’s Cheques

- Letter of credit

- Underwriting securities

- Collection of statistics

MONEY CREATION OR CREDIT CREATION

It is one of the most important activities of commercial banks. Through the process of money creation, commercial banks are able to create credit, which is far excess of the initial or Primary Deposits.

This process can be better understood by making two assumptions:

- The entire commercial banking system is one unit and is termed as ‘Banks’.

- All receipts and payments in the economy are routed through the Banks, i.e. all payments are made through cheques and all receipts are deposited in the banks.

Why only Fraction of deposits are kept as Cash Reserve?

Banks keep a fraction of deposits as Cash Reserve because a prudent banker, by his experience, knows two things:

- All the depositors do not approach the banks for withdrawal of money at the same time and also they do not withdrew the entire amount in one go.

- There is a constant flow of new deposits into the banks.

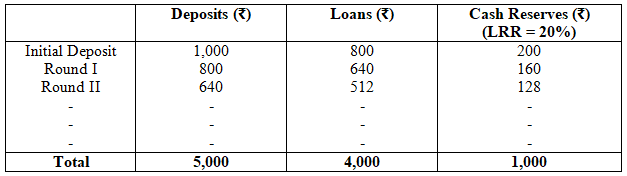

Refer the following table:

As seen in table, banks are able to create total deposits of Rs.5,000 with the initial deposit of just Rs.1,000. It means, total deposits become ‘five times’ of the initial deposit. Five times is nothing but the value of ‘Money Multiplier’.

Money Multiplier or Credit Multiplier or Deposit Multiplier

Money multiplier is the number by which total deposits can increase due to a given change in deposits. It is inversely related to legal reserve ratio. In other words, Money Multiplier is the process by which the commercial banks create credit, based upon the reserve ratio and initial deposits. It is calculated as:

Money Multiplier or Credit Multiplier or Deposit Multiplier = 1/LRR

In the given example, LRR I s20% or 0.2, So,

Money Multiplier = 1/0.2

= 5

It signifies that for every unit of money kept as reserves, banks are able to create 5 units of money. The value of money multiplier is determined by LRR. Higher the value of LRR, lower is the value of money multiplier and less money is created by the banking system.

CENTRAL BANK

Central Bank is an ‘Apex’ body that controls, operates, regulates and directs the entire banking and monetary structure of the country.

It is known as the apex (supreme) body as it occupies the top most position in the monetary and banking system of the country. All the financially developed countries have their own central bank. India’s Central Bank is the Reserve Bank of India (RBI). RBI was established in April 1, 1935 under Reserve Bank of India Act passed in 1934.

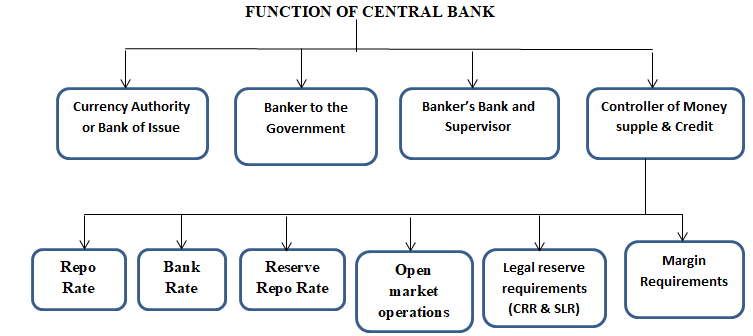

FUNCTIONS OF CENTRAL BANK

As the Central Bank of the country, The Reserve Bank of India performs the following functions:

- Currency Authority (or Bank of Issue) – Central Bank has the sole authority for issuing currency in the country. In India, Reserve Bank of India (RBI) has the sole right to issue paper currency notes (except one-rupee notes and coins, which are issued by the Ministry of Finance). The One Rupee note bears the signature of Finance Secretary, while other currency notes bear the signature of Governor of RBI.

Advantages to Sole Authority of Note issue with RBI

- It leads to uniformity in note circulation.

- It gives the central bank power to influence money supply because currency with public is a part of money supply.

- It enables the government to have supervision and control over the central bank with respect to issue of notes.

- It ensures public faith in the currency system.

- It helps in stabilization of internal and external value of currency.

2. Banker to the Government – The Reserve Bank of India acts as a banker, agent and a financial advisor to the Central Government and all the State Governments.

As a banker, it carries out all banking business of the government.

- It maintains a current account to keep their cash balances.

- It accepts receipts and makes payments for the government and carries out exchange, remittance and other banking operations.

- It also gives loans and advances to the government for temporary periods. The government borrows money by selling treasury bills to the Central Bank.

3. Banker’s Bank and Supervisor – There are a number of commercial banks in a country. There should be some agency to regulate and supervise their proper functioning. Being the apex bank, the central bank (RBI) acts as the banker to other banks.

- Custodian of Cash Reserves – Commercial banks are required to keep a certain proportion of their deposits (known as Cash Reserve Ratio or CRR) with the central bank.

- Lender of the Last Resort – When commercial banks fail to meet their financial requirements from other sources, i.e. in case of a financial emergency, they approach the central bank to give loans and advance as lender of the last resort.

- Clearing House – As central bank holds the cash reserves of all the commercial banks, it becomes easier and more convenient for it to act as their clearing house. All commercial bank have their accounts with the central bank.

4. Controller of Money Supply and Credit – The Reserve Bank of India (RBI) is empowered to regulate the money supply in the economy through its ‘Monetary Policy’. It is the policy adopted by the Central Bank of economy in the direction of credit control or money supply.

i. country (RBI in case of India) lends money to commercial banks to meet their short-term needs. The central bank advances loans against approved securities or eligible bills of exchange.

ii. Bank Rate (or Discount Rate) – Bank rate is the rate at which the central bank of a country (RBI in case of India) lends money to commercial banks to meet their long-term needs.

iii. Reserve Repo Rate (or Reverse Repurchase Rate) – This is the exact opposite of Repo Rate. Reserves Repo Rate is the rate of interest at which commercial banks can deposit their surplus funds with the Central Bank, for a relatively shorter period of time.

iv. Open Market Operations – Open market operations (OMO) refer to buying and selling of government securities by the Central Bank from/to the public and commercial banks.

v. Legal Reserve Requirements (Variable Reserve Ratio Method) – According to Legal reserve requirements, commercial banks are obliged to maintain reserves. It is a very quick and direct method for controlling the credit creating power of commercial banks. Commercial Banks are required to maintain reserves on two accounts:

- Cash reserve ratio (CRR) – It refers to the minimum percentage of net demand and time liabilities, to be kept by commercial banks with the central bank.

- Statutory Liquidity Ratio (SLR) – It refers to a minimum percentage of net demand and time liabilities which commercial banks are required to maintain with themselves.

vi. Margin Requirements – Margin is the difference between the amount of loan and market value of the security offered by the borrower against the loan. It the margin fixed by the Central Bank is 40%, then commercial banks are allowed to give a loan only up to 60% of the value of security.