What is Economy?

You must have observed many activities happening around you in your daily life. For instance, you may have seen factories, mines, shops, offices, flyovers, railways, etc. All these institution and organizations may collectively be called an economy. Such units enable people to earn and income and, at the same time, help to produce goods and services that people require for use. An economy is a system which provides people, the means to work and earn a living. It is an organization that provides living to the people. This task makes use of the available resources to produce the goods and services that people want. For example, Indian economy consists of all sources of production in agriculture, industry, transport and communication, banking, etc.

Vital Processes of an Economy

Economy is a system which provides living to the people. For this objective to be fulfilled, it is necessary that every economy should undertake three economic activities:

- Production

- Consumption

- Investment or Capital Formation.

These economic activities are known as the essentials or the vital processes of an economy.

SCARCITY

Scarcity refers to the limitation of supply in relation to demand for a commodity. It refers to situation, when wanted exceed the available resources. As a result, goods are not readily available and society does not any enough resource to satisfy all wants of its people. Scarcity is universal, i.e. every individual, organization and economy faces scarcity of resources. Scarcity of resources calls for economizing of resources. Economizing of resources refers to making optimum use of the available resources.

ECONOMIC PROBLEM

Economic Problem is a problem of choice involving the satisfaction of unlimited wants out of limited resources having alternative uses.

Reasons for Economic Problem

- Scarcity of Resources – Resources (i.e. land, labor, capital, etc.) are limited in relation to their demand and the economy cannot produce all the people want. It is the basic reasons for the existence of economic problems in all economies.

- Unlimited Human Wants – Human wants are never-ending, i.e. they can never be fully satisfied. As soon as one want is satisfied, another new want emerges. The wants of the people are unlimited and keep on multiplying & cannot be satisfied due to limited resources. Human wants also differ in priorities, i.e. all wants are not of equal intensity.

- Alternate Uses – Resources are not only scarce, but they can also be put to various uses. It makes choice among resources more important. For example, petrol is used not only in vehicles, but also for running machines, generators, etc. As a result, economy has to make choice between the alternative uses of the given resources.

Meaning of Economics – Economics is a social science which studies the way a society choose to use its limited resources which have alternate uses, to produce goods and serives and to distribute them among different group of people.

Positive Economics and Normative Economics

Positive Economics (or Science) – Positive economics studies the facts of life, i.e., it deals with ‘things as they are’. Positive Economics deals with what are the economic problems and how are they actually solved. For example, India is an overpopulated country or prices are constantly rising.

Positive Economics is neutral between ends – Positive economics remain strictly neutral with respect to ultimate ends. It avoids economic value judgments. For example a positive economic theory might describe that manufacturing and sale of cigarettes is injurious to health, but it does not provide any instruction or judgment on what policy output to be followed to avoid cigarettes in an economy.

“According to Robbins, economics is not concerned with moral or ethical questions and economists should analyse things as they are and have no right to give judgment.”

Do not confuse statement of Positive Economics as statement of truth – Positive economics statements should not be confused with statement of truth. They may be true of false. For example, If Para’s says that India is large than China in terms of land area, while Utkarsh says that China is larger than India in terms of land area, then India in terms of land area, then both are positive statement. However, Paras is wrong and Utkarsh is righ.

- Normative Economics (or Science) – Normative economics tell us ‘what ought to be’. Normative Economics deals with what ought to be or how the economic problems should be solved. For example, India should not be an overpopulated country or prices should not rise. Normative economic discusses what are desirable tings and should be realized and what are undesirable things and should be avoided. It gives decisions regarding value judgments.

Microeconomic and Macroeconomics

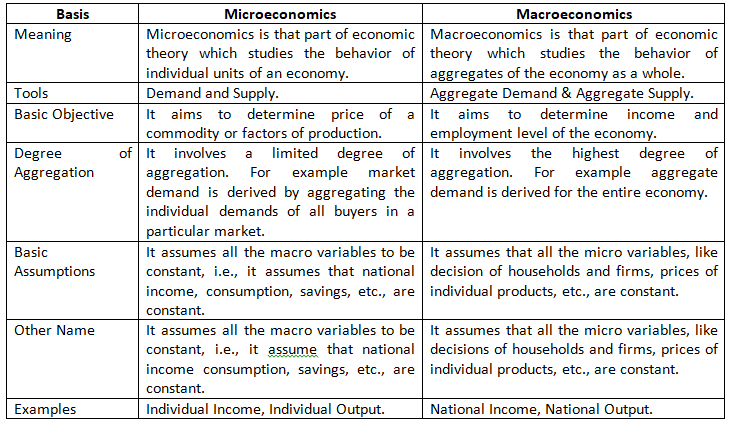

- Microeconomics – Adam Smith is considered to be the founder of the field of microeconomics. The term ‘micro’ has been derived from Greek word ‘mikros’ which means ‘small’.Microeconomics deals with analysis of behavior and economic actions of small and individual units of the economy, like a particular consumer, a firm or a small group of individual units. The concept of microeconomics is very important as it supplies the foundation for most of our understanding of the functioning of an economy. For example – Individual income, individual output, price of commodity, etc. its main tools are Demand and Supply.

- Macroeconomics – The term ‘macro’ has been derived from the Greek work ‘macros’ which means ‘large’. So, macroeconomics deals with the overall performance of the economy. It is concerned with the study of problems of the economy like inflation, unemployment, poverty, etc. Macroeconomics is that part of economics theory which studies that behavior of aggregates of the economy as a whole. For example – National income, aggregate output, aggregate consumption, etc. Its main tools are Aggregate Demand and Aggregate Supply.

Difference between Microeconomics and Macroeconomics

Central Problems of an Economy

Production, distribution and disposition of goods and services are the basic economic activities of life. In the course of these activities, every society has to face a scarcity of resources. Because of this scarcity, every society has to decide how to allocate scare resources. It leads to following central problems, that are faced by every economy:

- What to produce

- How to produce

- For whom to produce

These problems are called central problem because these are the most basic problems of an economy and all other problems revolve around them.

- What to produce – This problem involves section of goods and services to be produced and the quantity to be produced of each selected commodity. Every economy has limited resources and thus, cannot produce all the goods. More of one good or service usually means less of others. For Example – Production of more sugar is possible only by reducing the production of other goods. Production of more war goods is possible only by reducing the production of civil goods. So, on the basis of the importance of various goods, an economy has to decide which goods should be produced and in what quantities. This is a problem of allocation of resources among different goods.

The problem of ‘What to produce’ has two aspects:

- What possible commodities to produce – An economy has to decide, which consumer goods (rice, wheat, clothes, etc.) and which of the capital goods (machinery, equipment’s, etc.) are to be produced. In the same way, economy has to make a choice between civil goods (bread, butter, etc.) and war goods (guns, tanks, etc.).

- How much to produce – After deciding the goods to be produced, economy has to decide the quantity of each commodity, that is selected. It means, it involves a decision regarding the quantity to be produced, of consumer and capital goods, civil and war good and so on.

2. How to Produce – This problem refers to the selection of techniques to be used for the production of goods and services. A good can be produced using different techniques of production. By ‘technique’, we mean which particular combination of inputs to be used. Generally, techniques are classified as: labor intensive techniques (LIT) and Capital intensive techniques (CIT).

- In Labour intensive technique, more labour and less capital (in the form of machines, etc.) is used.

- In capital intensive technique, there is more capital and less labour utilization.

3. For Whom to Produce – This problem relates to the distribution of produced goods and services among the individuals within the economy, i.e. selection of the category of people who will ultimately consume the goods, i.e. whether to produce goods for more poor and less rich or more rich and less poor.

The problem can be categorized under two main heads:

- Personal Distribution – It means how the national income of an economy is distributed among different groups of people.

- Functional Distribution – It involves deciding the share of different factors of production in the total national product of the country.

Opportunity cost – As resources are scare, society is always forced to make choices. To produce more of one good, a certain amount of other goods has to be sacrificed. The true cost of using economic resources in any given project is the loss of the alternative output which they might have produced. Hence, Opportunity Cost is the cost of next best alternative foregone. For example – suppose you are working in a bank at a salary of Rs.70,000 per month. Further suppose, you receive two more job offers:

- To work as an executive at Rs.60,000 per month; or

- To become a journalist at Rs.65,000 per month.

In the given case, the opportunity cost of working in the bank is the cost of next best alternative foregone, i.e. Rs.65,000. The amount of other goods and services, that must be sacrificed to obtain more of any one good, is called the opportunity cost of that good.

Production Possibility Frontier (PPF)

Production Possibility Frontier (PPF) refers to the graphical representation of possible combinations of two goods that can be produced with given resource and technology. Alternately, PPF is the locus of various possible combinations of two goods that can be produced with given resources and technology.

Synonyms of PPF

PPF is also known by the following names:

- Production possibility Curve (PPC)

- Production possibility Boundary

- Transformation Curve

- Transformation Boundary

- Transformation Frontier

Assumptions for PPF

Production possibility frontier is based on the following assumption:

- The amount of resources in an economy is fixed, but these resources can be transferred from one use to another;

- With the help of given resources, only two goods can be produced;

- The resources are fully and efficiently utilized;

- Resources are not equally efficient in production of all products. So, when resources are transferred from production of one good to another, the productivity decreases;

- The level of technology is assumed to be constant.

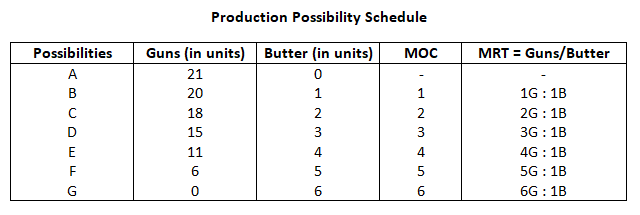

The concept of PPF can be better understood with the help of following imaginary (hypothetical schedule and diagram:

Marginal Opportunity Cost (MOC) – MOC refer to the number of a commodity sacrificed to gain one additional unit of another commodity. In case of PPF, MOC is always increasing, i.e. more and more unites of a commodity have to be sacrificed to gain an additional unit of another commodity.

Marginal Rate of Transformation (MRT) – MRT is the ratio of number of units of a commodity sacrificed to gain an additional unit to another commodity.

MRT = Δ Units Sacrificed/ Δ Units Gained .

In the given example of guns and butter, MRT = Δ Guns / Δ Butter

MRT measures the slope of Production Possibility Frontier.

Characteristics or Properties of PPF

The two basic characteristics or features or properties of PPF are:

- PPF slopes Downwards – PPF shows all the maximum possible combinations of two goods, which can be produced with the available resource and technology. In such a case, more of one good can be produced only by taking resources away from the production of another good.

- PPF is Concave Shaped – PPF is concave shaped because of the increasing marginal rate of transformation (MRT), i.e. more and more units of one commodity are sacrificed to gain an additional unit of another commodity.

Whether Economy will always operate on PPF?

In must be remembered that PPF does not show the point at which the economy will actually operate. It only shows the maximum available possibilities, which an economy can produce.

The exact point of operation depends on how well the resources of the economy are used.

- Economy will operate on PPF only when resources are fully and efficiently utilized.

- Economy will operate at any point inside PPF if resources are not fully and efficiently utilized.

- Economy cannot operate at any point outside PPF as it is unattainable with the available productive capacity.

It means:

- Economy can either operate on PPF or inside PPF, known as ‘Attainable Combinations’.

- However, economy cannot operate outside PPF, known as ‘Unattainable Combinations’.

Attainable and Unattainable Combinations

Attainable Combinations – It refers to those combination at which economy can operate. There can be two attainable options:

- Optimum utilization of resources – If the resources are used in the best possible manner, then economy will operate at any point (like, A, B, C or D) on PPF.

2. Inefficient utilization of resources – However, the actual production can fall short of its capabilities. It there is wastage or inefficient utilization of resources, then economy will operate at any point inside the PPF (like E).

Unattainable Combinations: With the given amount of available resources, it is impossible for the economy to produce any combination more than the given possible combination, i.e. an economy can never operate at any point outside the PPF.

PPF and MRT – We can measure MRT on the PPF. For example, MRT between the possibilities D and E is equal to DH/HE and between E and F, it is equal to EI/IF and so on. We know, PPF is concave shaped curve. The slope of PPF is a measure of the MRT. Since the slope of a concave curve increase as we move downwards along the curve, the MRT also rises as we move downwards along the curve.

Can PPF be a straight line? – PPF can be a straight line if we assume that MRT is constant, i.e. the same amount of a commodity is sacrificed to gain an additional unit of another commodity. It is possible only when we assume that all the resources are equally efficient in the production of all goods.

Can PPF be Convex to the Origin? – PPF can be convex to the origin if MRT is decreasing, i.e. less and less units of a commodity are sacrificed to gain an additional unit of another commodity.

PPF and Opportunity Cost – The opportunity cost of a product is the alternative that must be given up to produce that product. PPF illustrates the concept of opportunity cost. The opportunity cost of producing more butter is fewer guns. As we mover from ‘E’ to ‘F’ the production of butter rises from 4 units to 5 units, but the number of guns decreases from 11 units to 6 units, i.e. opportunity cost of the 5th unit of butter is sacrifice of 5 units of guns.

PPF as Transformation Curve – Slope of PPF indicates the ease or difficulty in transforming one good into another.

Change in PPF – PPF is based on the assumption, that resources of an economy are fixed. However, in this changing world, the productive capacity of an economy is constantly changings due to increase or decrease in resources. Such changes in resource lead to change in PPF.

- Shift in PPF – The PPF can shift either towards right or towards left, when there is a change in resources or technology with respect to both the goods.

- Rightward Shift in PPF – when there is “Advancement or Upgradation of Technology” or/and “Growth of Resources” in respect to both the goods, then PPF will shift to the right. For example, if there is an increase in resource for the production of butter and guns, we can produce more of both the goods. In such case, existing PPF (PP) will shift to the right, represented by P1P1.

- Leftward Shift in PPF – PPF will shift towards left, when there is a technological degradation and /or decrease in resources with respect to both the goods. For example, destruction of resources in an earthquake will reduce the productive capacity and as a result, PPF will shift to the left from PP to P1P1.

2. Rotation of PPF – It happens when there is a change in productive capacity (resources or technology) with respect to only one good. The rotation can be either for the commodity on the X-axis or for commodity on the Y-axis.

- Rotation for Commodity on the X-axis – When there is a technological improvement or an increase in resources for the production of the commodity on the X-axis (say, butter), then PPF will rotate from AB to AC.

- Rotation for commodity on the Y-axis – A technological improvement or an increase in resources for production of commodity on Y-axis (say, guns), will rotate the PPF from AB to CB. However, in case of degradation in technology or a decrease in resources for production of guns, PPF will rotate to the left from AB to DB.