- Cash Basis Of Accounting – Cash basis of accounting is a system in which transactions are recorded when cash is transacted, whether received or paid. It means, revenue is recognised on receipt of cash. Likewise, expenses are recorded as incurred when they have been paid. The difference between the total income and total expenses represents Profit or Loss of a business for the accounting period. Thus, when Cash Basis of Accounting is followed, outstanding and prepaid expenses and income received in advance or accrued incomes are not considered.

- Accrual Basis of Accounting – Under Accrual Basis of Accounting, unlike under Cash Basis of Accounting, income is recorded as income when it is earned or accrued. For example, credit sale is recognised as sale irrespective of the fact whether amount has been received or not. Similarly, if an expense has been incurred but payment has not been made, it will be recorded as an expense. For example, rent for the month of March, 2021 has not been paid. It will still be recorded as an expense because it had become due.

Difference between Accrual Basis of Accounting and Cash Basis of Accounting –

Accrual Basis of Accounting –

- Both Cash and credit transactions are recorded

- Prepaid and outstanding expenses are accounted in the profit and loss Account. Accrued income and income received in advance are also accounted and shown in the Balance sheet.

- The accrual Basis of Accounting requires technical knowledge as many adjustments like prepaid, outstanding, capital and revenue and required to be made.

- Correct profit or loss is ascertained because it records both cash and credit transactions.

Cash Basis of Accounting –

- Cash Transactions are recorded.

- Prepaid and outstanding expenses are not adjusted. Similarly, accrued income and income received in advance are not adjusted.

- It does not require much of technical knowledge as is required for Accrual Basis of Accounting.

- Correct profit or loss is not ascertained because it records only cash transactions.

PRACTICAL PROBLEMS

- During the year ended 31st March, 2025, Mohan, had cash sales of Rs.90,000 and credit sales of Rs.60,000. His expenses for the year were Rs.70,000 out which Rs.30,000 is yet to be paid. Find Mohan’s income for the year following the Cash Basis of Accounting.

Answer:

Cash sales = 90,000

Total Expenses = 70,000

Outstanding Expenses = 30,000

Cash Expenses = 70,000 – 30,000

= 40,000

Mohan’s income for 2025 = 90,000 – 40,000

= 50,000

2. Taking the value given in 1 above, determine the income according to the Accrual Basis of Accounting.

Answer:-

Mohan’s income for first year – Second year accrual basis of accounting

= total Sales – total expenses

= Cash sales + Credit Sales – total expenses

= Rs.90,000 + Rs.60,000 – Rs.70,000

= Rs.1,50,000 – 70,000

= Rs.80,000

3. In the financial year 2024-25, Shiva earned total revenue of Rs.3,45,000, out of which Rs.2,35,000 was received. Total expenses paid by him were Rs.2,20,000, out of which Rs.10,000 relate to 2025-26. Expenses of Rs.15,000 are still outstanding. Ascertain Shiva’s income for 2024-25 as per:

- Cash Basis of Accounting

- Accrual Basis of Accounting.

Answer:-

- Cash Basis of Accounting

Identify cash received: Revenue received = Rs.2,35,000.

Identify cash paid : Expenses paid = Rs.2,20,000

Calculate income: Cash received – Cash paid

= 2,35,000 – 2,20,000

= Rs.15.000

- Accrual basis accounting

Identify total expenses for the period = Expenses paid (Rs.2,20,000) – Expenses relating to 2025-26 (Rs.10,000) + Outstanding expenses (Rs.15,000)

= 345000-(2,20,000 – 10,000 + 15,000)

= 1,20,000

4. Naren gave following information about his income and expenses for the year ended 31st March, 2025:

Expenses paid 1,80,000

Exp. paid in advance (not included in above) 20,000

Exp. Not yet paid 10,000

Income received 2,40,000

Income received in advance (included in Income Received) 15,000

Income not yet received 12,000

Find the net income or profit of Naren if he adopts (i) Cash Basis of Accounting, and (ii) Accrual Basis of Accounting.

Answer:-

- Cash Basis

Income = Rs.2,40,000

Expenses = Rs.180,000

Profit = Rs.240,000 – Rs.180,000

= Rs.60,000

- Accrual Basis:

Total income = Rs.2,40,000 – Rs.15,000 (advance) + 12,000

= Rs.2,37,000

Total expenses = Rs.180,000 – Rs.20,000 (advance) + Rs.10,000

= Rs.170,000

Profit = Rs.237,000 – Rs.170,000

= 67,000

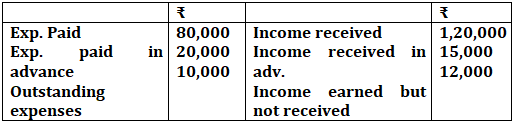

5. Pawan gives the following information about his income and expenses for the year ended 31st March, 2025”

Compute the net income of Pawan if he adopts (i) Cash Basis of Accounting, and (ii) Accrual Basis of Accounting.

Ans Cash Basis of Accounting

In cash basis, only actual cash transactions (received/paid) are considered.

Income: ₹1,20,000 (only received income is considered)

Expenses: ₹80,000 (only paid expenses are considered)

Profit (Cash Basis) = Income – Expenses

= ₹1,20,000 – ₹80,000

= ₹40,000

(b)Accrual basis accounting

Income Calculation:

Income received = ₹1,20,000

(-) Income received in advance = ₹15,000 (not yet earned)

(+) Income earned but not received = ₹12,000

Total Income (Accrual) = ₹1,20,000 – ₹15,000 + ₹12,000 = ₹1,17,000

Expense Calculation:

Expenses paid = ₹80,000

(-) Prepaid expenses = ₹20,000 (not related to current year)

(+) Outstanding expenses = ₹10,000

Total Expenses (Accrual) = ₹80,000 – ₹20,000 + ₹10,000 = ₹70,000

Profit (Accrual Basis) = ₹1,17,000 – ₹70,000 = ₹47,000