Straight Line Method (SLM)

Q1. Tushar purchased a machine for Rs.90,000. Expenses incurred on its cartage and installation are Rs.10,000. The residual value at the end of its expected useful life of 10 years is estimated at Rs.20,000. Calculate the amount of depreciation by Straight Line Method for the first year ending 31st March, 2025, if the machine is purchased on:

- 1st April, 2024.

- 1st July, 2024.

- 1st October, 2024.

- 1st January, 2025.

Solution:-

Calculation the total cost of the machine:

Cost of machine = Rs.90,000

Cartae and installation = 10,000

Total cost = Rs.90,000 + 10,000

= 100,000

Calculation the annual depreciation using the straight line Method:

Residual value = 20,000

Useful life = 10 years

Annual depreciation = (cost – residual value) / Useful life

= (100,000 – 20,000 ) / 10

= 80,000 / 10 = 8,000 per year

Calculation depreciation for each cash based on the months the machine was used in the first year ending 31st March, 2025.

The financial year is from 1st April 2024 to 31st March 2025.

Calculation the total cost of the machine:

Cost of machine = Rs.90,000

Cartae and installation = 10,000

Total cost = Rs.90,000 + 10,000

= 100,000

Calculation the annual depreciation using the straight line Method:

Residual value = 20,000

Useful life = 10 years

Annual depreciation = (cost – residual value) / Useful life

= (100,000 – 20,000 ) / 10

= 80,000 / 10 = 8,000 per year

Calculation depreciation for each cash based on the months the machine was used in the first year ending 31st March, 2025.

The financial year is from 1st April 2024 to 31st March 2025.

Calculation the total cost of the machine:

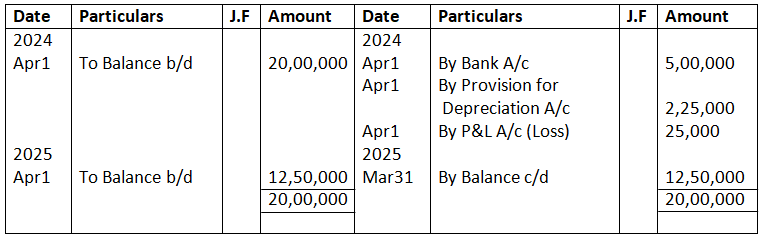

Cost of machine = Rs.90,000

Cartae and installation = 10,000

Total cost = Rs.90,000 + 10,000

= 100,000

Calculation the annual depreciation using the straight line Method:

Residual value = 20,000

Useful life = 10 years

Annual depreciation = (cost – residual value) / Useful life

= (100,000 – 20,000 ) / 10

= 80,000 / 10 = 8,000 per year

Calculation depreciation for each cash based on the months the machine was used in the first year ending 31st March, 2025.

The financial year is from 1st April 2024 to 31st March 2025.

- Purchase on 1st April, 2024:

Month used = 12 (full year)

Depreciation = 8,000 x (12/12)

= 8,000

b. Purchased on 1st July, 2024:

Month used = July to March = 9 months

Depreciation = 8,000 x (9/12) = 6,000

c. Purchased on 1st October, 2024:

Month used = October to March = 6 months

Depreciation = 8,000 x (6/12) = Rs.4,000

d. Purchased on 1st January, 2025:

Months used = Jan. to March = 3

Final Answer

- 8,000

- 6,000

- 4,000

- 2,000

Q-2 Calculated the Amount of annual Depreciation and Rate of Depreciation under Straight Line Method (SLM) from the following:

Purchased a second-hand machine for 96,000, spent 24,000 on its cartage, repairs and installation, estimated useful life of machine 4 years. Estimated residual value 72,000

Solution – Calculation of Rate of Depreciation by Straight Line Method:-

Amount of Depreciation = Cost of Asset – Estimated Scrap value/Number of year of life of Asset

Amount of Depreciation = 1, 20,000 – 72,000/4

= 48,000 / 4

= 12,000

= Rate of Depreciation = Amount of Depreciation / Cost of Asset x 100

= Rate of Depreciation = 12,000/120000 x 100

= 10% P.a.

Q-3. On 1st July 2024, Raja ltd. Purchased a second hand machine for 5,00,000 and spend 1,00,000 on its cartage , repair and installation.

Calculate the amount of depreciation of 10% p.a. according to the straight line method for the year ended on 31st March 2025.

Ans- cost of machinery= 500,000+100,000=600,000

600,000 X 10% X9/12

45000

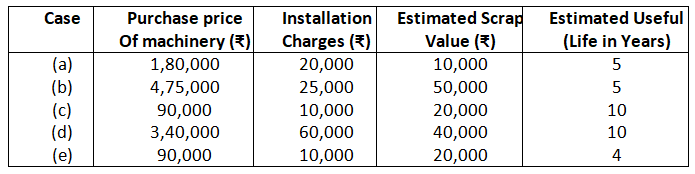

Q-4 Calculate annual depreciation and rate of depreciation under Straight Line Method in each of the alternative cases:

Ans. a) 180,000+20,000=200,000-10,000 / 5

38000 X 100 / 2,00,000

=19

b) 4,75,000+25000= 500,000-50,000 / 5

=90,000 X 100 / 5,00,000

= 18

c) 90,000+10,000 = 100,000-20,000 / 10

= 80,000 X 100 / 1,00,000

=8

d) 340,000+60,000 = 400,000-40,000 / 10

= 36000 X 100 / 4,00,000

=9

e) 90,000 +10,000 =100,000-20,000 / 4

=20,000 X100/ 1,00,000

=20

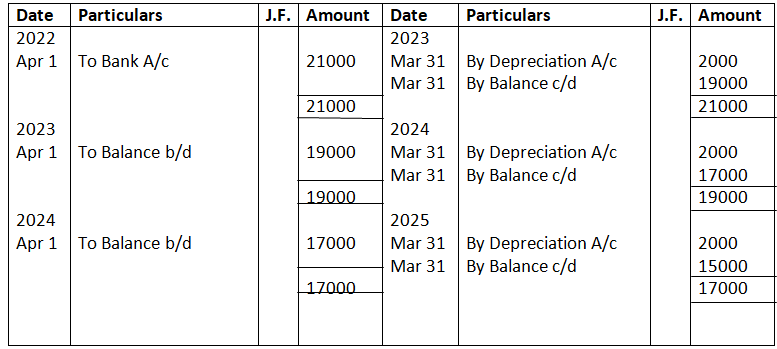

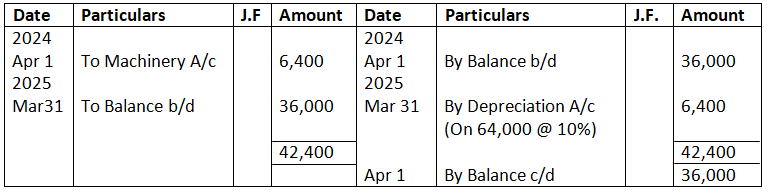

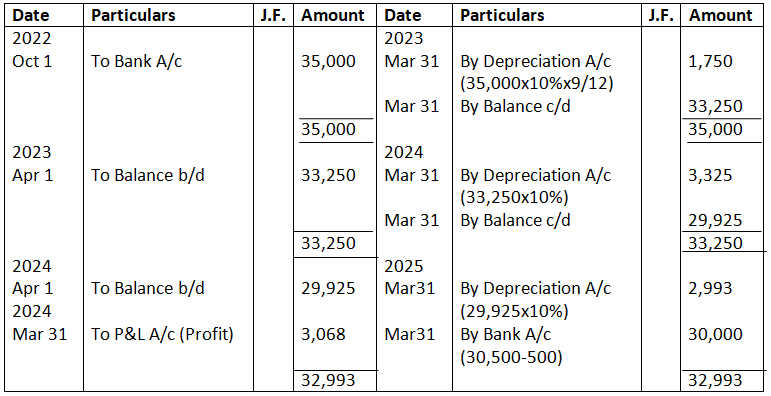

Q-5Mohan & Co. purchased machinery for₹21,000 on 1st April, 2022. The estimated useful life of the machinery is 10 years, after which its realisable value will be₹ 1,000. Determine the amount of annual depreciation according to the Straight Line Method and prepare Machinery Account for the first three years. The books of account are closed on 31st March every year.

Solution – Mohan & co.

Dr Machinery Account Cr

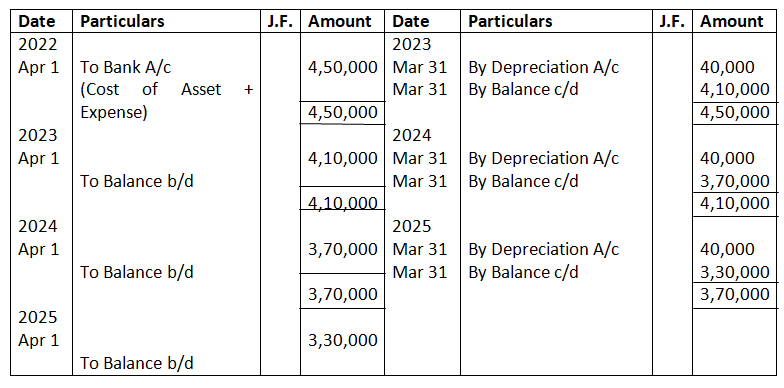

Q-6. On 1st April, 2022, Starex Purchased a machine costing 4, 00,000 and spent 50,000 on its installation. The estimated life of the machinery is 10 years, after which its residual value will be 50,000 only. Find the amount of annual depreciation according to the Fixed Instalment Method and prepare Machinery Account for the first three years. The books are closed on 31st March every year.

Solution – Book of X Ltd

Dr Machinery Account Cr

Working Note 1:–

Cost of Assets = Purchases Price of Machine + Repairs and Installation Charge

= (4, 00,000 + 50,000)

= 4, 50,000

Working Note 2:- Calculation of Depreciation:-

Amount of Depreciation = Cost of Asset + Installation Charge – Scrap Value/ Number of the Year of the Life of Asset

Amount of Depreciation = (4, 00,000 + 50,000 – 50,000)/ 10

= 40,000 P.A.

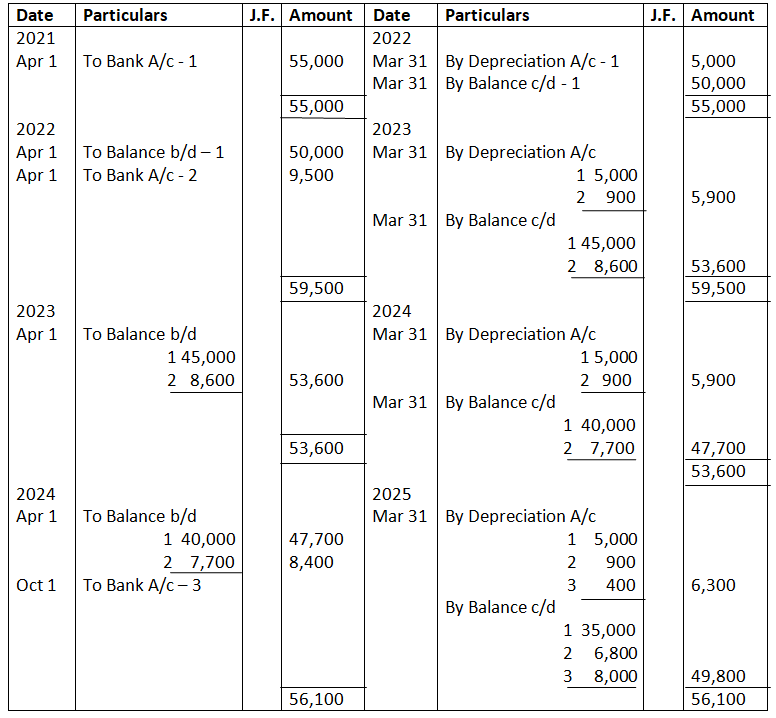

Q-7. On 1st April, 2021, furniture costing 55,000 was purchased. It is estimated that its life is 10 years at the end of which it will be sold for 5,000. Additions are made on 1st April, 2022and 1st October, 2024 to the value of 9,500 and 8,400 (Residual values 500 and 400 respectively). Show the Furniture Account for the first four years, if Depreciation is written off according to the Straight Line Method.

Solution – In the Books of……

Dr Furniture Account Cr

Working Note – Calculation of Depreciation

Amount of Depreciation = Cost of Asset – Scrap Value/ Number of year of Life of Asset

For Furniture 1

Amount of Depreciation = 55,000 – 5,000 / 10 = 5,000 P.A.

For Furniture 2

Amount of Depreciation = 9,500 – 500/10 = 900 P.A

For Furniture 3

Amount of Depreciation = 8,400 – 400 / 10 = 800 P.A.

Depreciation for Furniture 3 (for Six Months) = 800 x 6/12 = 400

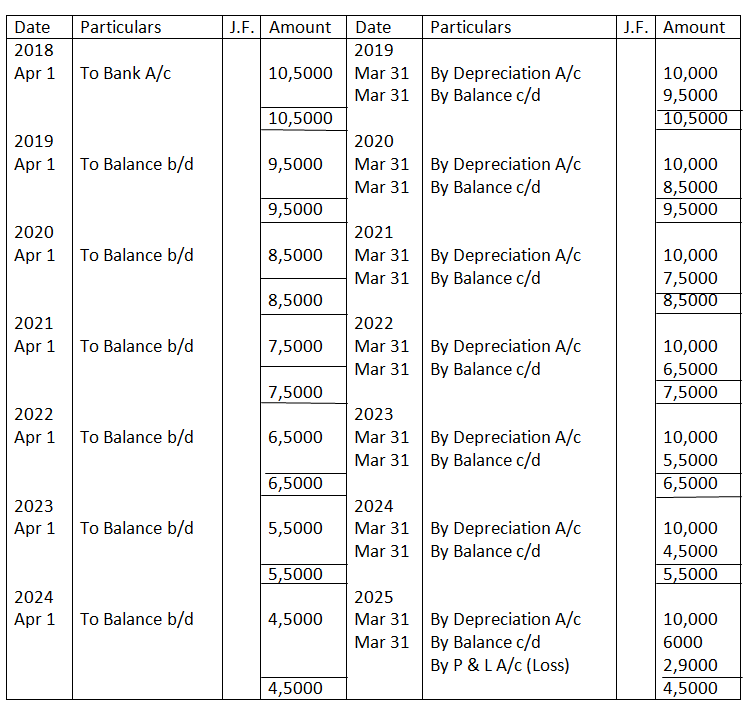

Q-8. On 1st April, 2018, a company purchased a machinery for₹ 1,05,000. The scrap value was estimated to be ₹ 5,000 at the end of asset’s 10 years’ life. Straight Line Method of depreciation was used. The accounting year ends on 31st March every year. The machine was sold for ₹ 6,000 on 31st March, 2025. Calculate the following

- The Depreciation expense for the year ended 31st March, 2019.

- The net book value of the asset on 31st March, 2023.

- The gain or loss on sale of the machine on 31st March, 2025.

Solution –

Dr Asset Account Cr

Working Note –

- Depreciation Expense for the year ended 31st March, 2018

Amount of Depreciation = Cost of Asset – Scrap Value / Nu. of year of life of Asset

Amount of Depreciation = 10,5000 – 5000 / 10

= 10,000 P.A.

II. The net book value of the assets on 31st March, 2022

Net Book Value = Cost Price – Depreciation till date

= 10,5000 – 10,000 x 5

= 5,5000

III. Calculation of Profit or Loss on the Sale of Asset

=Value of Assets on 1 April, 2017 – Total Depreciation

= 10,5000 – 70,000

Net Book Value of Asset = 3,5000

Loss on sale of Machinery = Net Book value of Asset – Sales Price

= 3,5000 – 6000

= 2,9000

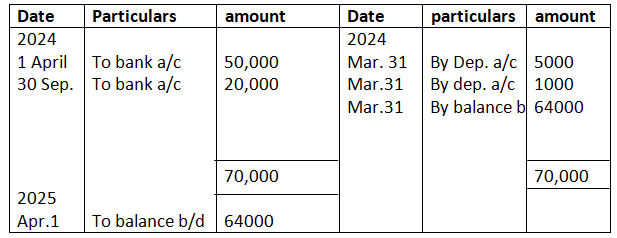

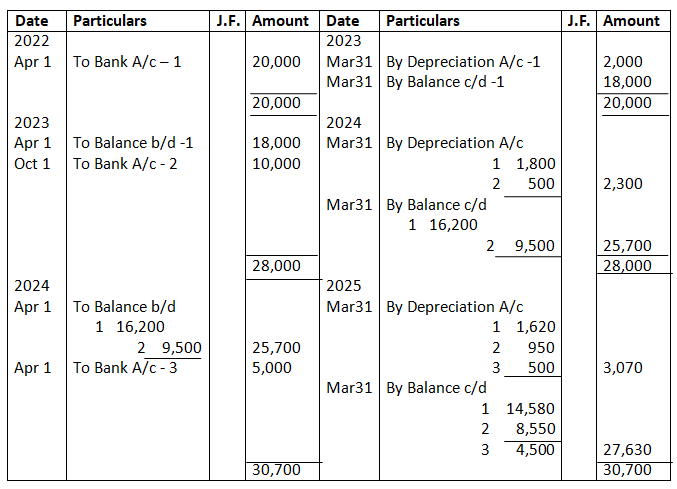

Q-9. From the following transactions of a concern, prepare the Machinery Account for the year ended 31st March, 2024:

1st April, 2024: Purchased a second-hand machinery for 40,000

1st April, 2024: Spent 10,000 on repairs for making it serviceable

30th Sep, 2024: Purchased additional new machinery for 20,000

31st December, 2024: Repairs and renewal of machinery 3,000

31st March, 2025: Depreciate the machinery at 10% p.a.

Solution:-

Q-10. On 1st April, 2021, Harish Traders Purchased 5 machines for 60,000 each. On 1st April, 2023, one of the machines was sold at a loss of 8,000. On 1st July, 2024, second machine was sold at a loss of 12,500. A new machine was purchased for 1, 00,000 on 1st October, 2024.

Prepare Machinery Account for 4 years, assuming accounts are closed on 31st March, 2025. Depreciation is provided @ 10% per annum as per Straight Line Method.

Solution –

Dr Cr

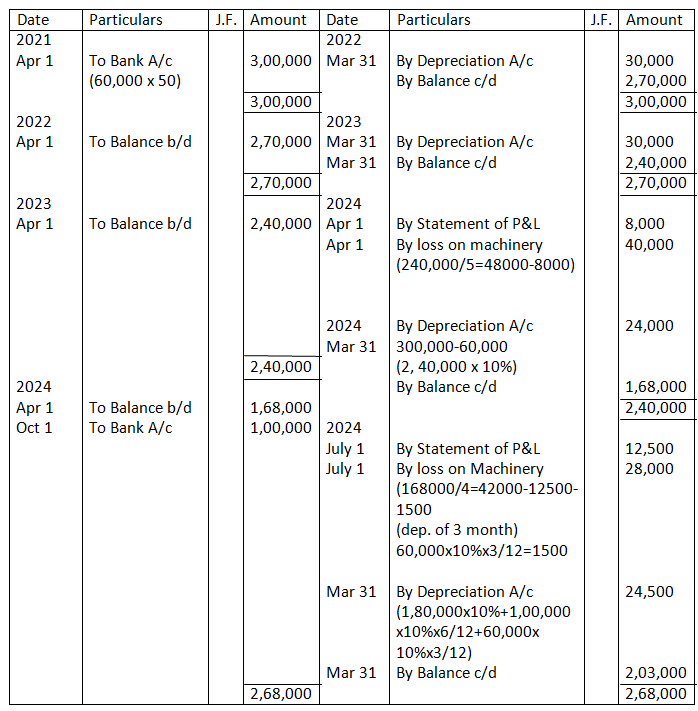

Q-11. On 1st April, 2021, Madhukar Ltd. Purchased a machine for 2, 40,000 and spent 10,000 on its erection. On 1st October, 2021, an additional machinery costing 1,00,000 was purchased on 1st October, 2023, the machine purchased on 1st April, 2021 was sold for 1,43,000 and on the same date, a new machine was purchased at a cost of 2,00,000. Show the Machinery Account for the first four financial years after charging Depreciation at 5% p.a. by the Straight Line Method.

Solution –

Dr Machinery Account Cr

Working Note 1:-

Cost of Assets = Purchases Price of Machine + Repairs and Installation charge

Cost of Assets = 2, 40,000 + 10,000

Cost of Assets = 2, 50,000

Working Note 2:-

Calculation of Depreciation

Amount of Depreciation = Cost of Asset x Rate of Depreciation

For Machine 1

Amount of Depreciation = 2, 50,000 x 5/100 = 12,500 P.a.

For Machine 2

Amount of Depreciation = 1, 00,000 x 5/100 = 5,000 P.a.

For Machine 2 (Six Months)

Amount of Depreciation = 1, 00,000 x 5/100 x 6/12 = 2,500 P.a.

For Machine 3

Amount of Depreciation = 2, 00,000 x 5/100 = 10,000 P.a.

Working Note 3:-

- Calculation of Profit or Loss on the Sale of Machine 1

=Value of Assets on 1 April, 2017 – Total Depreciation on machine 1

= 2, 25,000 – 6,250 (250,000×5%x6/12)= 2, 18,750

Loss on sale of Machinery = Net Book value of Asset – Sales Price

= 2, 18,750 – 1, 43,000 = 75,750

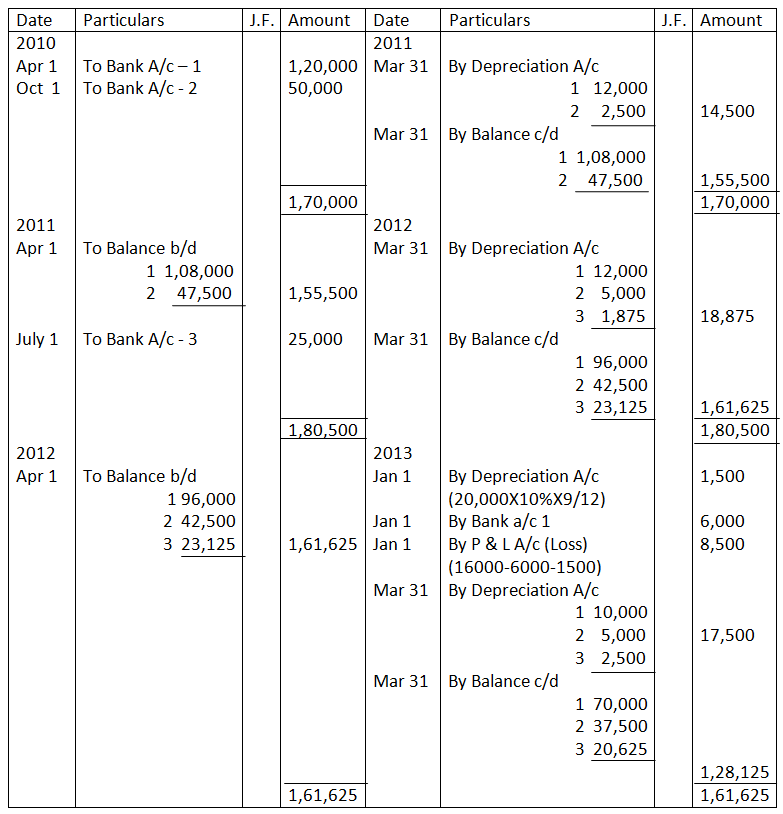

Q12. On 1st April, 2010, Plant and Machinery was purchased for 1,20,000. New machinery was purchased on 1st October, 2010 for 50,000 and on 1st July, 2011, for 25,000. On 1st January, 2013, a machinery of the original value of 20,000 which was included in the machinery purchased on 1st April, 2010, was sold for 6,000. Prepare Plant and Machinery A/c for three years after providing depreciation at 10% p.a. on Straight Line Method.

Solution –

Dr Machinery Account Cr

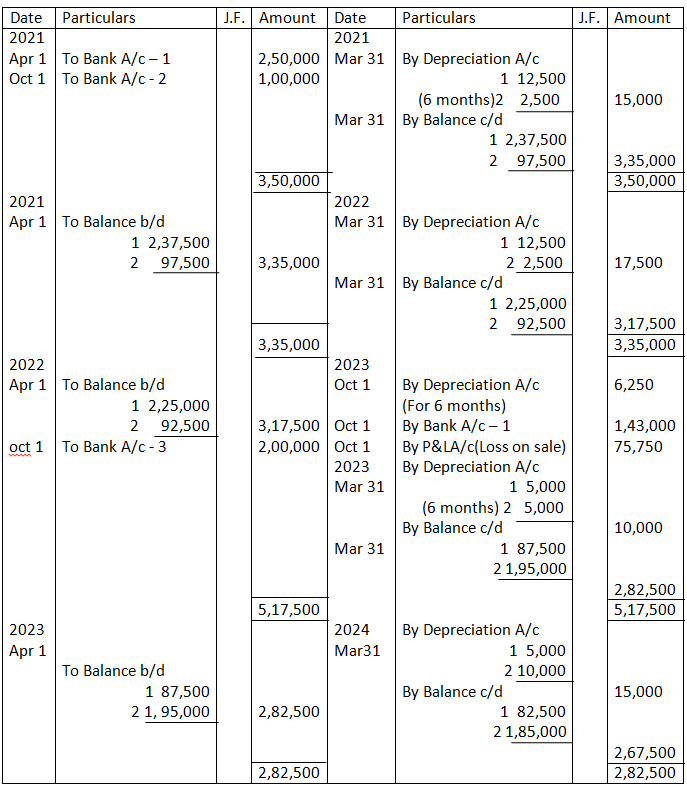

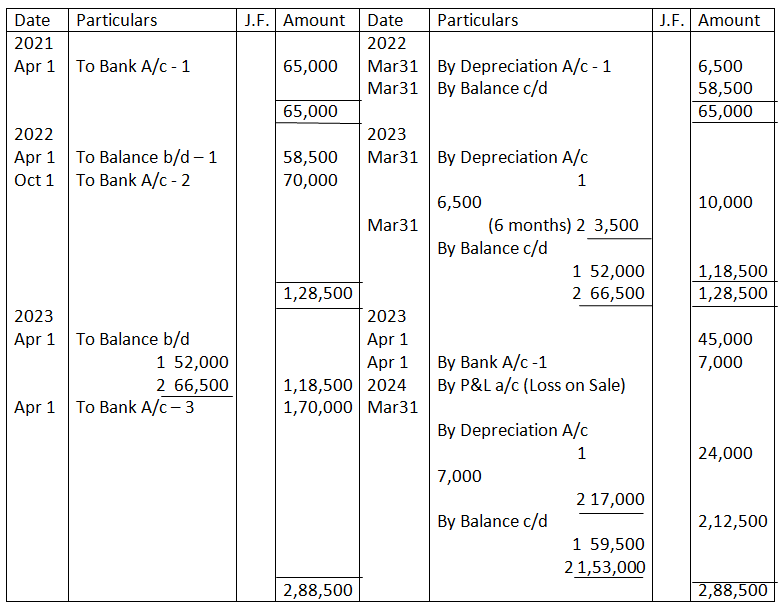

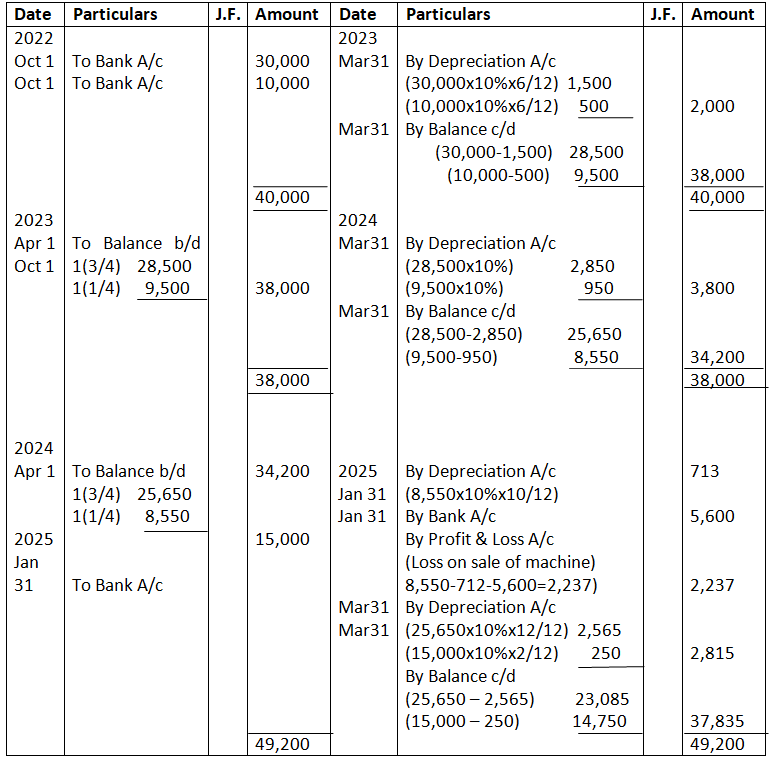

Q13. A Van was purchased on 1st April, 2021 for 60,000 and 5,000 was spent on its repairs and registration. On 1st October, 2022 another van was purchased for 70,000. On 1st April, 2023, the first van purchased on 1st April, 2021 was sold for 45,000 and a new van costing 1, 70,000 were purchased on the same sate. Show the Van Account from 2021-22 to 2023-24 on the basis of Straight Line Method, if the rate of Depreciation charged is 10% p.a. Assume that books are closed on 31st March every year.

Solution –

Dr Van Account Cr

Working Note 1:-

Calculation of Depreciation

Amount of Depreciation = Cost of Asset x Rate of Depreciation

For Van 1

Amount of Depreciation = 65,000 x 10/100 = 6,500 P.a.

For Van 2

Amount of Depreciation = 70,000 x 10/100 = 7,000 P.a.

For Van 2 (Six Months)

Amount of Depreciation = 70,000 x 10/100 x 6/12 = 3,500 P.a.

For Van 3

Amount of Depreciation = 1, 70,000 x 10/100 = 17,000 P.a.

Working Note 3:-

- Calculation of Profit or Loss on the Sale of Van 1

=Value of Machinery on 1 April, 2021 – Total Depreciation on Van 1

= 65,000 – 13,000 = 52,000

Loss on sale of Machinery = Net Book value of Van – Sales Price

= 52,000 – 45,000 = 7,000

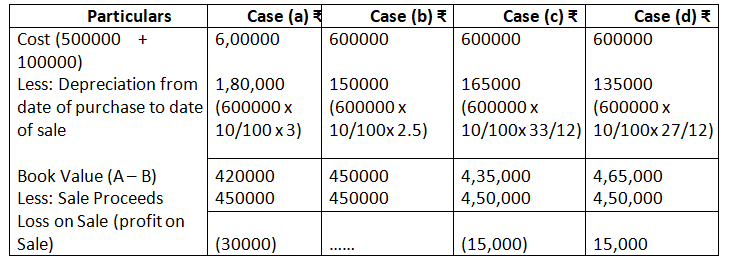

Q14. Mahima Traders purchased a second-hand machine for Rs.5,00,000 and spent Rs.1,00,000 on its repairs. Depreciation is to be provided @ 10% p.a. as per Straight Line Method. This machine is sold for Rs.4,50,000. Accounting year is financial year. Calculate profit or loss on sale of machine in each of the following alternative cases:

Ans.-

Calculation of Profit/Loss on Sale of Machine:

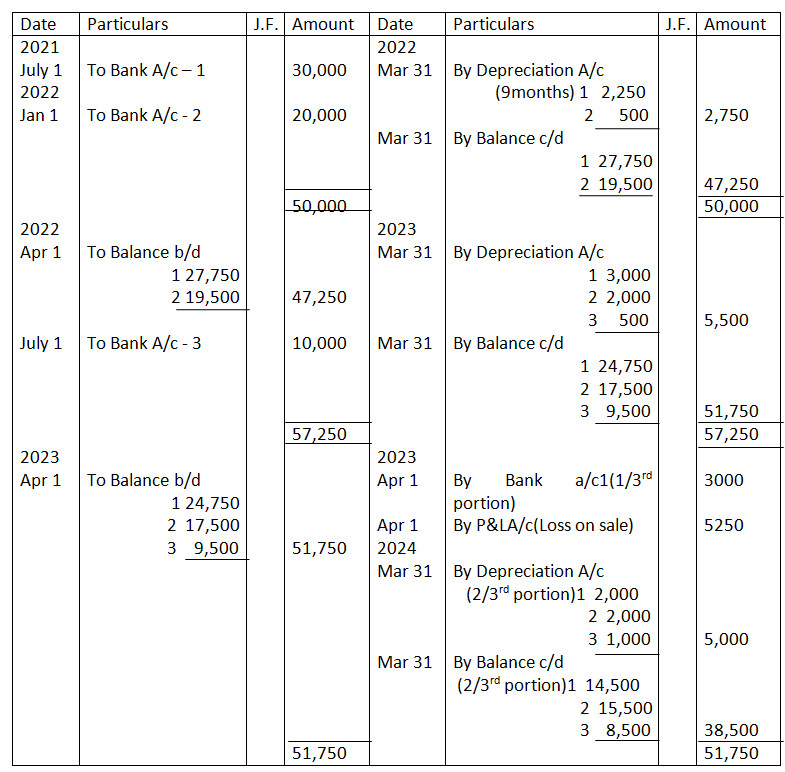

Q15. A company whose accounting year is a financial year, purchased on 1st July, 2022 machinery costing 30,000.

It purchased further machinery on 1st January, 2023 costing 20,000 and on 1st October, 2023 costing 10,000

On 1st April, 2024, one-third of the machinery installed on 1st July, 2022 become obsolete and was sold for 3,000

Show how Machinery Account would appear in the books of the company. It being given that machinery was depreciated by Fixed Instalment Method at 10% p.a. What would be the value of Machinery Account on 1st April, 2025?

Solution –

Dr Machinery Account Cr

Working Note 1:-

Calculation of Depreciation

Amount of Depreciation = Cost of Asset x Rate of Depreciation

For Machinery 1

Amount of Depreciation = 30,000 x 10/100 = 3,000 P.a.

For Machinery 1 (For 9 Months)

Amount of Depreciation = 30,000 x 10/100 x 9/12 = 2,250 P.a.

For Machinery 2

Amount of Depreciation = 20,000 x 10/100 = 2,000 P.a.

For Machinery 3

Amount of Depreciation = 10,000 x 10/100 = 1,000 P.a.

Working Note 2:-

- Calculation of Profit or Loss on the Sale of 1/3rd Part of Machine-1

=Value of Machinery on 1 July 2022 – Total Depreciation on Machinery 1

= 30,000 – 5,250 = 24,750

Loss on sale of Machinery = Value of 1/3rd Part of Machinery – Sales Price

= 8,250 – 3,000 = 5,250

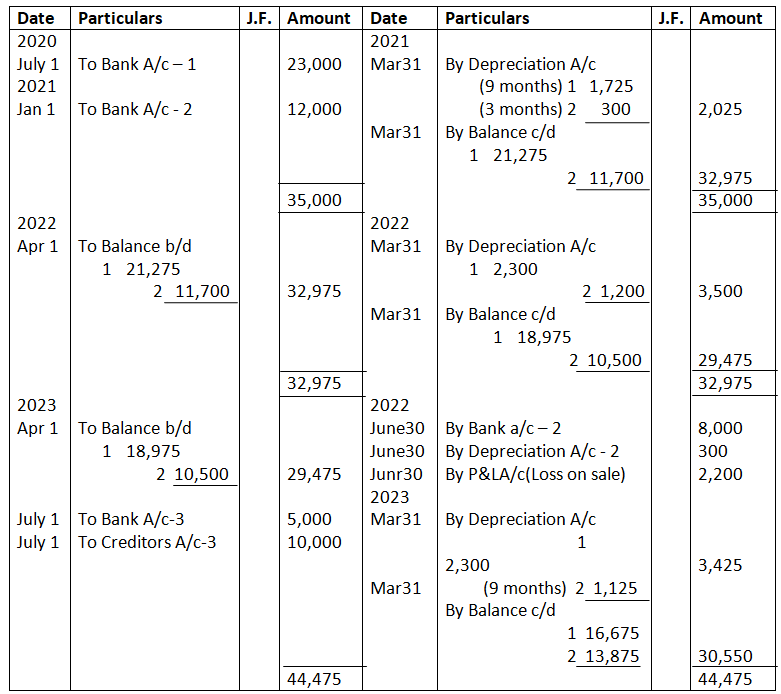

Q16. On 1st July, 2021, Alpha Ltd. purchases second-hand machinery for 20,000 and spends 3,000 on reconditioning and installing it. On 1st January, 2022, the firm purchases new machinery worth 12,000. On 30th June, 2023, the machinery purchased on 1st January, 2022, was sold for 8,000 and on 1st July, 2023, a fresh plant was installed. A payment for this plant was to be made as follows:

1st July, 2023 5,000

30th June, 2024 6,000

30th June, 2025 5,500

Payment in 2024 and 2025 include interest 1000 and 500

The company write off 10% p.a. on original cost. The account are closed every year on 31st March. Show the machinery account for the year ended 31st March 2024.

Solution – Book of A. Co. Ltd

Dr Machinery Account Cr

Working Note 1:-

Calculation of Depreciation

Amount of Depreciation = Cost of Asset x Rate of Depreciation

For Machinery 1

Amount of Depreciation = 23,000 x 10/100 = 2,300 P.a.

For Machinery 1 (For 9 Months)

Amount of Depreciation = 23,000 x 10/100 x 9/12 = 1,725 P.a.

For Machinery 2

Amount of Depreciation = 12,000 x 10/100 = 1,200 P.a.

For Machinery 2 (For 3 Months)

Amount of Depreciation = 12,000 x 10/100 x3/12= 300 P.a.

For Machinery 3

Amount of Depreciation = 15,000 x 10/100 = 1,500 P.a.

For Machinery 3 (For 9 Months)

Amount of Depreciation = 15,000 x 10/100 x 9/12 = 1,125 P.a.

Working Note 2:-

- Calculation of Profit or Loss on the Sale of Machine-2

=Value of Machinery on 1 July, 2022 – Total Depreciation on Machinery 2

= 12,000 – 1,800 = 10,200

Loss on sale of Machinery = Value of Machinery on 1 July, 2019– Sales Price

= 10,200 – 8,000 = 2,200

Recording of depreciation by creating provision for depreciation

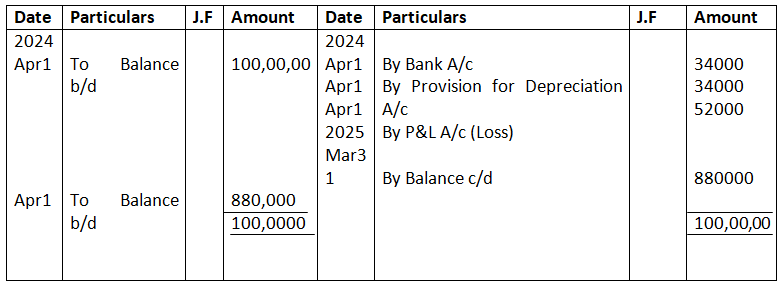

Q17. The following balances appeared in the books of Priyank Ltd. as on 1st April, 2024:

Machinery A/c 10,00,000

Provision for Depreciation A/c 4,50,000

Depreciation is provided at 10% per annum on the original cost on 31st March every year.

On 1st October, 2024, a machine which was purchased on 1st December, 2021 for ₹1,20,000 was sold for ₹34,000.

Prepare Machinery Account and Provision for Depreciation Account for the year 2024-25.

[Ans.: Loss on Sale of Machinery-₹ 52,000; Balance of Machinery Alc₹ 8,80,000;Balance of Provision for Depreciation Alc- ₹5,10,000.]

Solution:-

In the Books of Hari Bros

Dr Machinery Account Cr

Dr. Provision for Depreciation Account Cr.

Depreciation

1 dec 2020 to 31 march 2021 120,000X4/12×10%=4000

1 April 2021 to 31 march 2022 120,000×10%= 12000

1 April 2022 to 31 march 2023 120,000×10% 12000

1 April 2023 to 1 oct 2024 120,000x 6/12×10% 6000

34000

Loss on machinery 120,000-34000-34000=52000

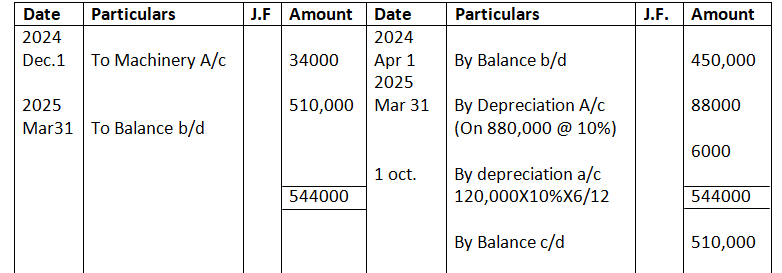

Q18. Following balances appear in the books of Hari Bros:

1st April, 2024 Machinery A/c 80,000

Provision for Depreciation A/c 36,000

On 1st April, 2024, they decided to sell a machine for 8,700. This machine was purchased for 16,000 in April, 2020.

Prepare the Provision for Depreciation Account and Machinery Account on 31st March, 2025, assuming the firm has been charging Depreciation at 10% p.a. on Straight Line Method.

Solution – In the Books of Hari Bros

Dr Machinery Account Cr

Dr. Provision for Depreciation Account Cr.

Working Note 1:-

- Calculation of Value of Machine on 1 April 2018 & Loss on sale of Machine

=Value of Machinery on 1 April, 2022 – Total Depreciation on Machinery

= 16,000 – 6,400 = 9,600

Profit on Sale of Machine = Value of Machinery on 1 April, 2022 – Sales Price

= 9,600 – 8,700 = 900

Amount of Depreciation = 16,000 x 10/100 = 1,600 p.a.

Total Depreciation = 1,600 x 4 = 6,400

Q19. Following balances appear in the books of Priyank Bros:

1st April, 2024 Machinery A/c 20, 00,000

Provision for Depreciation A/c 8, 00,000

On 1st April, 2024, they decide to sell a machine for 5, 00,000. This machine was purchased for 7, 50,000 on 1st April, 2021.

Prepare the Machinery Account and Provision for Depreciation Account for the Year ended 31st March, 2025 assuming that the firm has been charging Depreciation @ 10% p.a. on the Straight Line Method.

Solution – Books of Priyank Brothers

Dr Machinery Account Cr

Dr. Provision for Depreciation Account Cr.

Working Note 1:-

- Calculation of Value of Machine on 1 April 2020 & Loss on sale of Machine

=Value of Machinery on 1 April, 2024 – Total Depreciation on Machinery

= 7, 50,000 – 2, 25,000 = 5, 25,000

Profit on Sale of Machine = Value of Machinery on 1 April, 2024 – Sales Price

= 5, 25,000 – 5, 00,000 = 25,000

Amount of Depreciation = 7, 50,000 x 10/100 = 75,000 p.a.

Total Depreciation = 75,000 x 3 = 2, 25,000

Written down value method

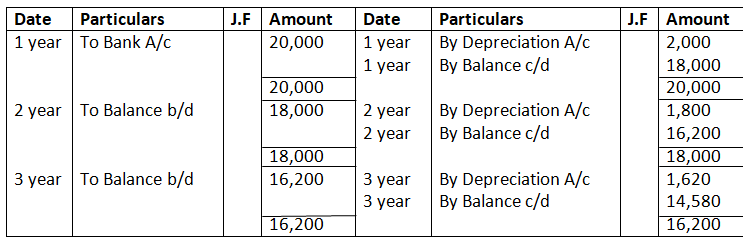

Q21. A boiler was purchased from abroad for 10,000. Shipping and forwarding charges 2,000, Import duty 7,000 and expenses of installation amounted to 1,000.

Calculate the Depreciation for the first three years (separately for each year) @ 10% p.a. on Diminishing Balance Method.

Solution –

Dr Boiler Account Cr

Working Note 1:-

Cost of Boiler = cost of Boiler + Shipping and forward charges + Import Duty + Installation Charges

= 10,000 + 2,000 + 7,000 + 1,000

= 20,000

Working Note 2:-

Calculation of Depreciation

Amount of Depreciation = Opening Balance x Rate of Depreciation

For 1 year

Amount of Depreciation = 20,000 x 10/100 = 2,000 P.a.

For 2 year

Amount of Depreciation = 18,000 x 10/100 = 1,800 P.a.

For 3 year

Amount of Depreciation = 16,200 x 10/100 = 1,620 P.a.

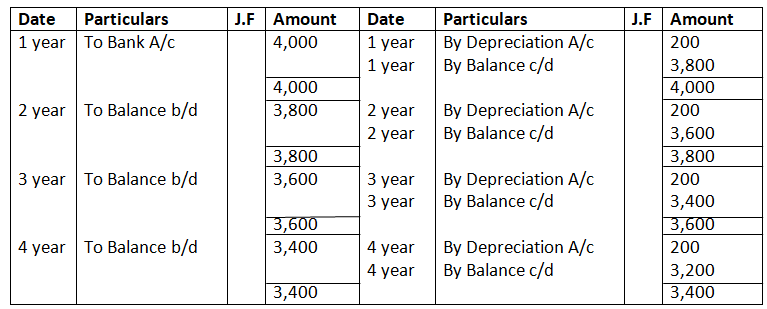

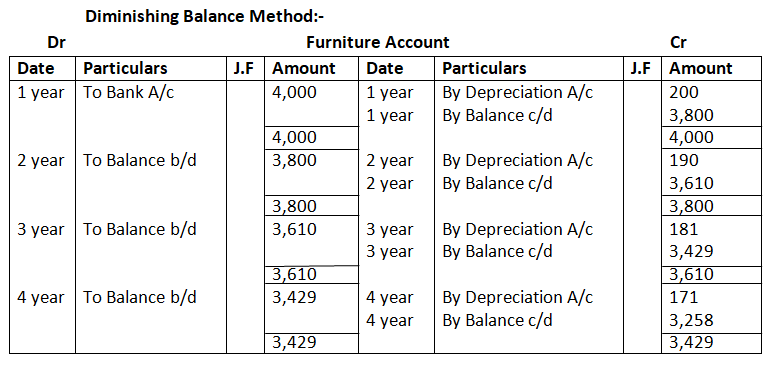

Q22. The original cost of furniture amounted to 4,000 and it is decided to write off 5% on the original cost as Depreciation at the end of each year. Show the Ledger Account as it will appear during the first four years. Show also how the same account will appear if it was decided to write off 5% p.a. on the diminishing balance of the asset each year.

Solution – Original Cost Basis:-

Dr Furniture Account Cr

Working Note 1:- Original Cost Basis

Calculation of Depreciation

Amount of Depreciation = Opening Balance x Rate of Depreciation

Amount of Depreciation = 4,000 x 5/100 = 200 p.a.

Working Note 2:- Diminishing Balance Method

Calculation of Depreciation

Amount of Depreciation = Opening Balance x Rate of Depreciation

For 1 year

Amount of Depreciation = 4,000 x 5/100 = 200 P.a.

For 2 year

Amount of Depreciation = 3,800 x 5/100 = 190 P.a.

For 3 year

Amount of Depreciation = 3,610 x 5/100 = 181 P.a.

For 3 year

Amount of Depreciation = 3,429 x 5/100 = 171 P.a.

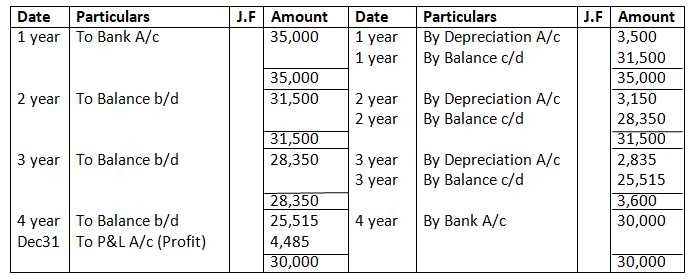

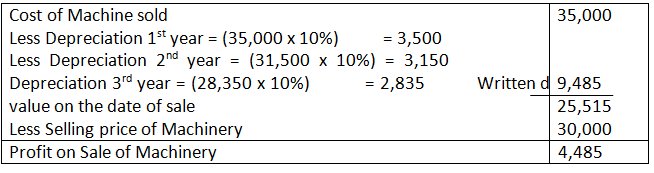

Q23. Kabir bought a machine for ₹25,000 on which he spent₹ 5,000 for carriage and freight, 1,000 for brokerage of the middleman, ₹3,500 for installation and ₹ 500 for an iron pad. The machine is depreciated @ 10% p.a. on Written Down Value basis. After three years, the machine was sold to Yash for₹ 30,500 and₹500 was paid as commission to the broker through whom the sale was affected. Find out the profit and loss on sale of machine.

Solution – Books of X

Dr Machinery Account Cr

Working Note 1:-

- Book Value of Machinery = Cost of Machine + Freight + Brokerage + Installation

= 25,000 + 5,000 + 1,000 + 3,500 + 500

= 35,000

b. Selling price of machinery = 30,500 – 500

= 30,000

Working Note 2:-

Calculation of Profit/Loss on Sale of Machine

Working Note 3:-

Calculation of Depreciation

Amount of Depreciation = Opening Balance x Rate of Depreciation x Number of Month

For 1year (12 months)

Amount of Depreciation = 35,000 x 10/100 x 12/12 = 3,500 P.a.

For 2year (12 months)

Amount of Depreciation = 31,500 x 10/100 x 12/12 = 3,150 P.a.

For 3 year (12 months)

Amount of Depreciation = 28,350 x 10/100 x 12/12= 2,835 P.a.

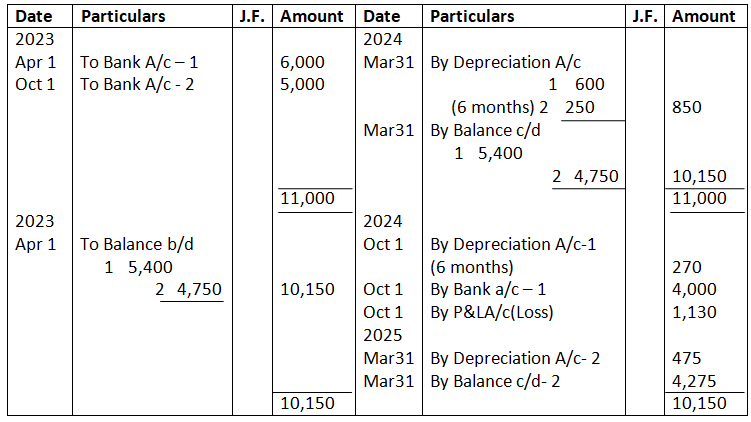

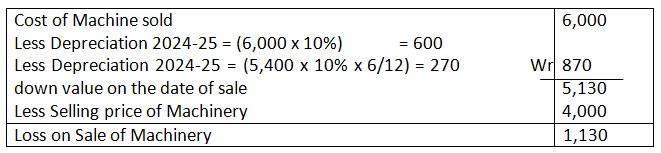

Q24. Rajesh purchased on 1st April, 2023, a machine for 6,000. On 1st October, 2023, he also purchased another machine for 5,000. On 1st October, 2024, he sold the machine purchased on 1st April, 2023 for 4,000.

It was decided that Depreciation @ 10% p.a. was to be written off every year under Diminishing Balance Method.

Assuming the accounts were closed on 31st March every year, show the Machinery Account for the years ended 31st March, 2024 and 2025.

Solution – Book of Babu

Dr Machinery Account Cr

Working Note 1:-

Calculation of Profit/Loss on Sale of Machine

Working Note 2:-

Calculation of Depreciation

Amount of Depreciation = Opening Balance x Rate of Depreciation x Number of Month

For Machinery 1 (1year 12 months)

Amount of Depreciation = 6,000 x 10/100 x 12/12 = 600 P.a.

For Machinery 1 (2year 6 months)

Amount of Depreciation = 5,400 x 10/100 x 6/12 = 270 P.a.

For Machinery 2 (1 year 6 months)

Amount of Depreciation = 5,000 x 10/100 x 6/12= 250 P.a.

For Machinery 2 (2year 12 months)

Amount of Depreciation = 4,750 x 10/100 x 12/12 = 475 P.a.

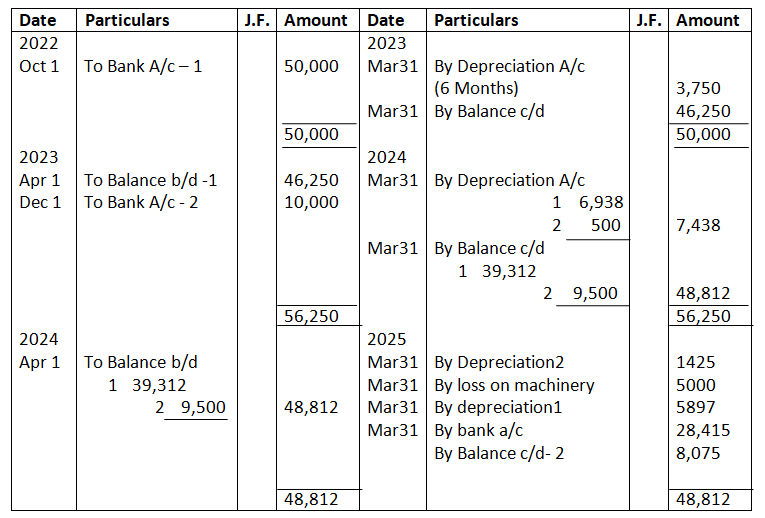

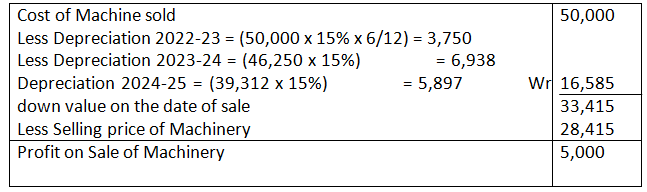

Q25. A company purchased a machine for 50,000 on 1st October, 2022. Another machine costing 10,000 was purchased on 1st December, 2023. On 31st March, 2025, the machine purchased in 2022 was sold at a loss of 5,000. The company charges depreciation @ 15% p.a. on Diminishing Balance Method. Accounts are closed on 31st March every year. Prepare the Machinery Account for 3 years.

Solution –

Dr Machinery Account Cr

Working Note 1:-

Calculation of Profit/Loss on Sale of Machine

Q26. On 1st October, 2022, Rahul Traders purchased a machine for Rs.25,000 and spent Rs.5,000 for carriage and freight; Rs.1,000 for brokerage of the middle-man, Rs.4,000 for installation. The machine is depreciated @ 10% p.a. on written down value basis. On 31st March, 2025, the machine was sold to Deepa for Rs.30,500 and Rs.500 was paid as commission to broker through whom the sale was affected. Find out the profit or loss on sale of machine if account are closed on 31st March, every year.

Solution:-

Dr Machinery Account Cr

Working Note 1:-

- Book Value of Machinery = Cost of Machine + Freight + Installation

= 25,000 + 5,000 + 1,000 + 4,000

= 35,000

b. Selling Price of Machinery = 30,500 – 500

= 30,000

Working Note 2:-

Calculation of Profit/Loss on Sale of Machine

Q27. On 1st April, 2022, a machinery was purchased for ₹20,000. On 1st October, 2023, another machine was purchased for 10,000 and on 1st April, 2024, one more machine was purchased for ₹5,000. The firm depreciates its machinery @ 10% p.a. on the Diminishing Balance Method.

What is the amount of Depreciation for the years ended 31st March, 2023, 2024 and 2025?

What will be the balance in Machinery Account as on 31st March, 2025?

Dr Machinery Account Cr

Q28. Gurman & Co. purchased machinery for₹ 40,000 on 1st October, 2022. Depreciation is provided @ 10% p.a. on the Diminishing Balance. On 31st January, 2025, one-fourth of the machinery was found unsuitable and disposed off for₹5,600. On the same date, new machinery at a cost of 15,000 was purchased. Write up the Machinery Account for the years ended 31st March, 2023, 2024 and 2025. Accounts are closed on 31st March each year.

Solution –

Dr Machinery Account Cr

Working Note 1:-

Calculation of Profit/Loss on Sale of Machine

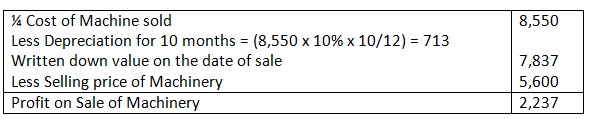

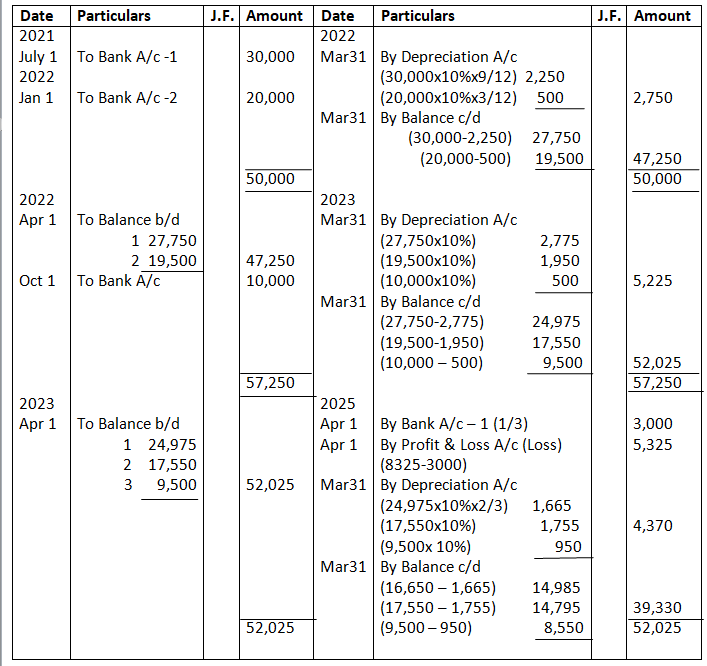

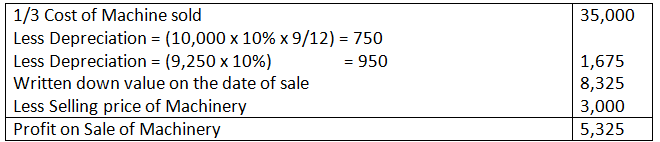

Q29. Bharat stores purchased on 1st July, 2021 machinery costing 30,000. It further purchased machinery on 1st January, 2022 costing 20,000 and on 1st October, 2022 costing 10,000. On 1st April, 2023, one-third of the machinery installed on 1st July, 2021 became obsolete and was sold for 3,000. The company follows financial year as accounting year.

Show how the Machinery Account would appear in the books of company if depreciation is charged @ 10% p.a. on Written down Value Method

Solution-

Dr Machinery Account Cr

Working Note 1:-

Calculation of Profit/Loss on Sale of Machine

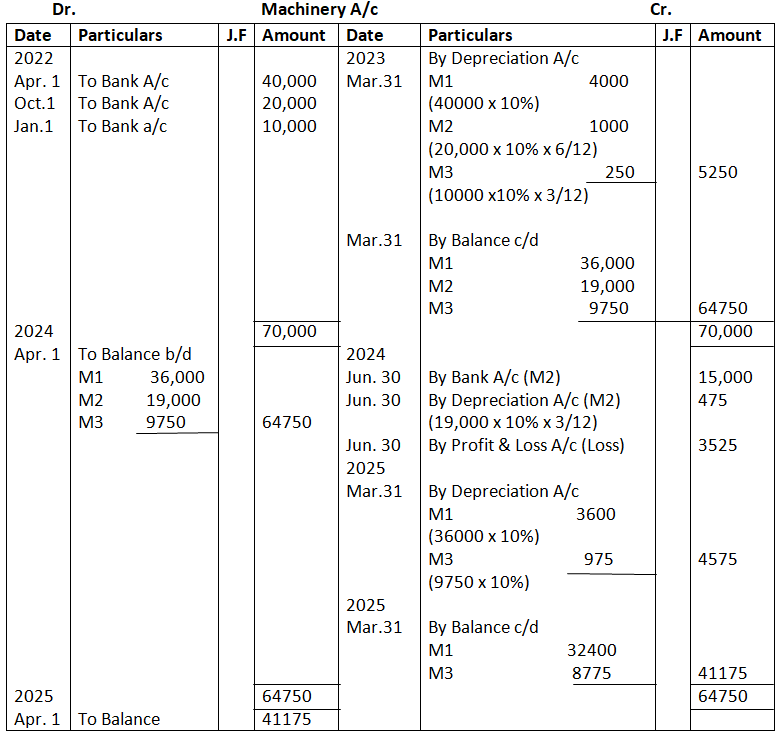

Q30. Sagar purchased the following machines:

On 1st April, 2022 Rs.40,000

On 1st October, 2022 Rs.20,000

On 1st January, 2023 Rs.10,000

Depreciation was provided @ 10% p.a. under Written Down Value Method (Diminishing Balance Method). The Machine purchased on 1st October, 2022 was sold on 30th June. 2023 at Rs.15,000.

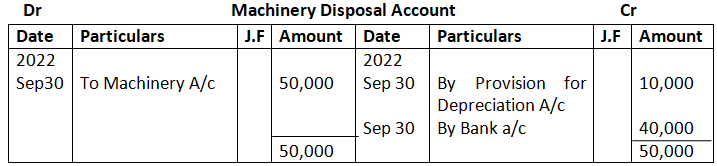

Show necessary ledger accounts in the books of Sager Ltd. If accounts are closed on 31st March every year.

Solution:-

Machinery disposal account

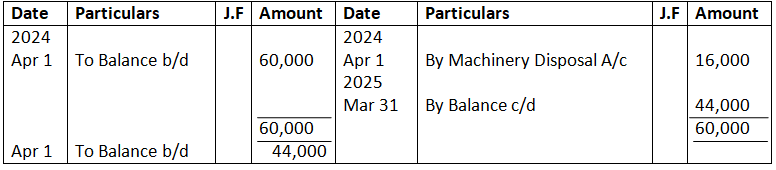

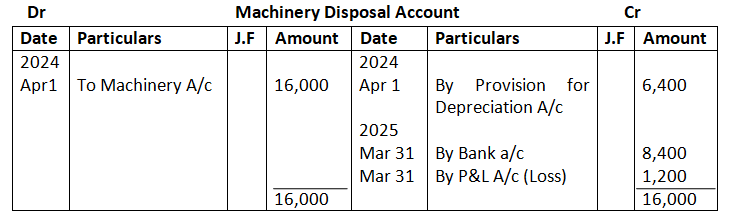

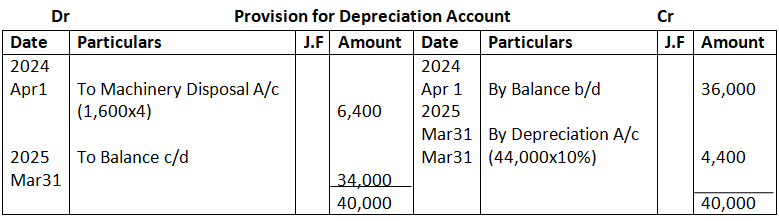

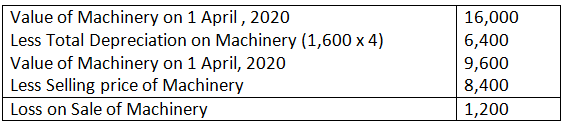

Q31. Following balances appear in the books of M/s Amrit as on 1st April, 2024:

2024

1st April Machinery A/c 60,000

Provision for Depreciation A/c 36,000

On 1st April, 2024, they decided to dispose off machinery for 8,400 which was purchased on 1st April, 2020 for 16,000.

You are required to prepare the Machinery Account, Provision for Depreciation Account and Machinery Disposal Account for the year ended 31st March, 2025. Depreciation was charged at 10% p.a. on cost following Straight Line Method.

Solution – In the Books of M/s. Amrit

Dr Machinery Account Cr

Working Note 1:-

Calculation of Profit/Loss on Sale of Machine

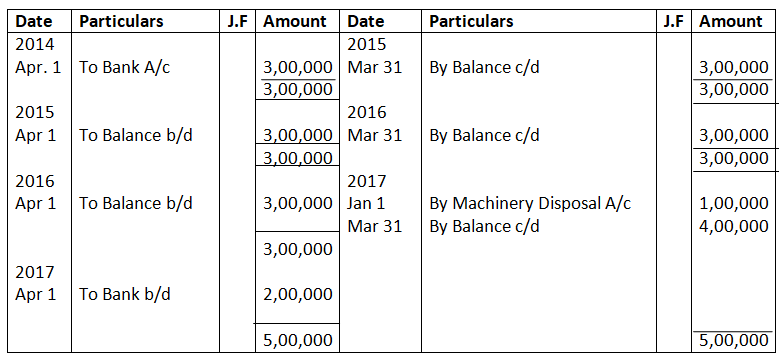

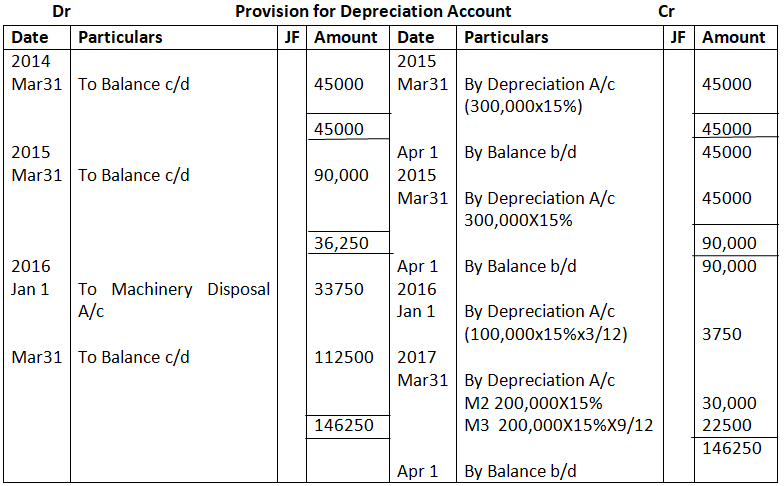

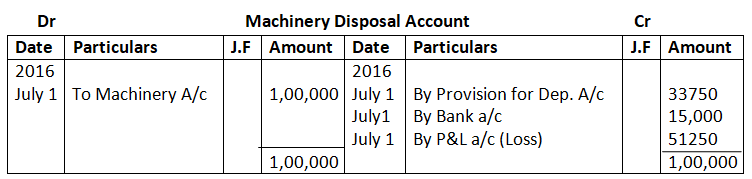

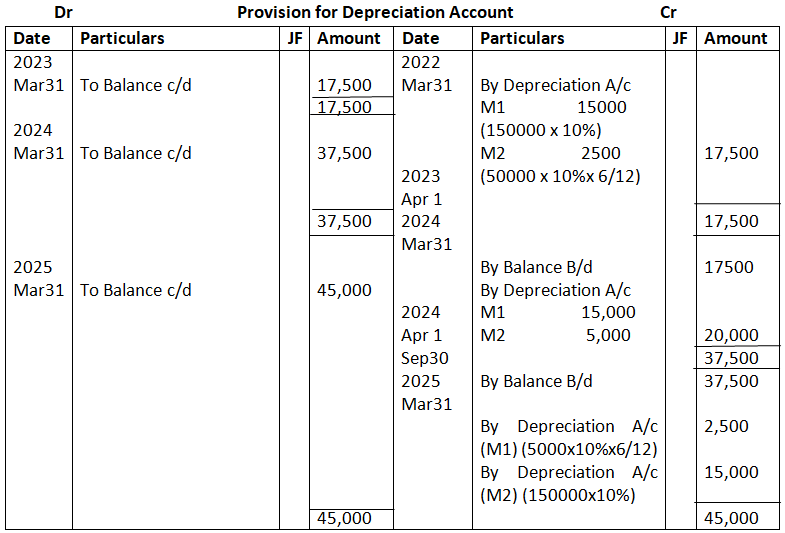

Q32. On 1st April, 2014, Veeru Ltd. Purchased a machinery for 2, 50,000 and spent 50,000 on its installation. On 1st July, 2016, 1/3rd of machinery purchased on 1st April, 2014 was sold for 15,000 and a new machinery at the cost of 2, 00,000 was purchased on the same date. The company has adopted the method of providing depreciation @ 15% p.a. on Straight Line Method. Show the Machinery Account, Provision for Depreciation Account and machinery Disposal Account for Three years ended on 31st March, 2015 to 31st March, 2017.

Solution –

Dr Machinery Account Cr

Working Note 1:-

Calculation of Accumulated Depreciation on Machinery sold

For (2014 – 15) , 1,00,000 x 15% – Rs.15,000

For (2015 – 16) , 1,00,000 x 15% – Rs.15,000

For (2016 – 17) , 1,00,000 x 15% x 3/12 – Rs.3,750

Total Depreciation provided on machinery sold 33,760

Calculate of Depreication provided for 2016 – 17

Depreciation on Remaining Machinery – 30,000

(3,00,000 – 1,00,000 ) x 15%

Depreciation on Machinery Purchased on 1st July 2016

(2,00,000 x 15% x 9/12) – 22,500

Depreciation on Machinery sold – 3,750

(1,00,000 x 15% x 3/12)

Calculation of Profit or loss on Machinery sold

Book Value – 1,00,000

Accumulated Depreciation – Rs.33,750

Rs.66,250

Less: Sale Proceeds Rs.15,000

Loss on Sale of Machinery Rs.51,250

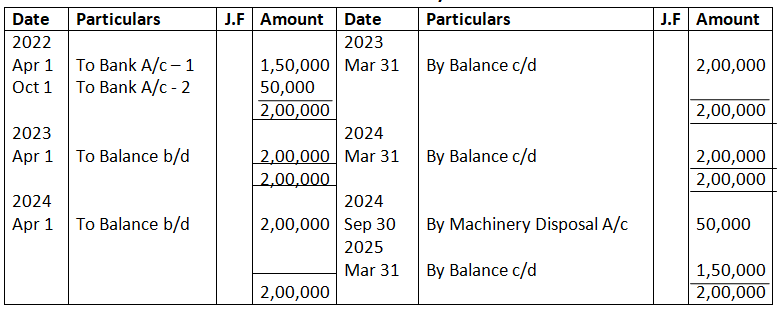

Q33. Ashoka & Co. Whose Books are closed on 31st March, purchased a machinery for 1, 50,000 on 1st April, 2022. Additional machinery was acquired for 50,000 on 1st October, 2022. Certain machinery which was purchased for 50,000 on 1st October, 2022 was sold for 40,000 on 30th September, 2024.

Prepare the Machinery Account and Accumulated Depreciation Account for all the years up to the Year ended 31st March, 2025. Depreciation is charged @ 10% p.a. on Straight Line Method. Also show the Machinery Disposal Account.

Solution – Books of Sharma & Co

Dr Machinery Account Cr

Working Note:-

Depreciation provid on machinery sold till 1st October 2024:

For (2022 – 23), 50,000 x 10% x 6/12 – 2500

For (2023 – 24), 50,000 x 10% – 5,000

For (2024 – 25), 50,000 x 10% x 6/12 – 2500

Total Depreciation provided on machinery sold 10,000

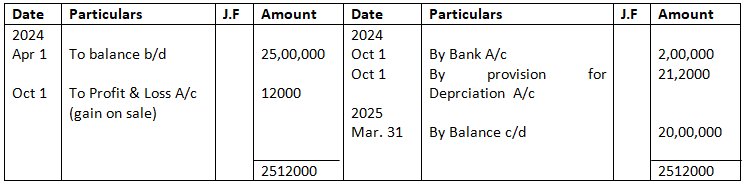

Q34. From the books of Harish Traders following information as on 1st April, 2024 is extracted:

Plant and Machinery Account ₹25,00,000

Provision for Depreciation Account 5,80,000

Depreciation is charged on the plant at 20% p.a. by the Diminishing Balance Method. A piece of machinery purchased on 1st April, 2022 for₹5,00,000 was sold on 1st October, 2024 for ₹3,00,000. Prepare the Plant and Machinery Account and Provision for Depreciation Account for the year ended 31st March, 2025. Also, prepare Machinery Disposal Account.

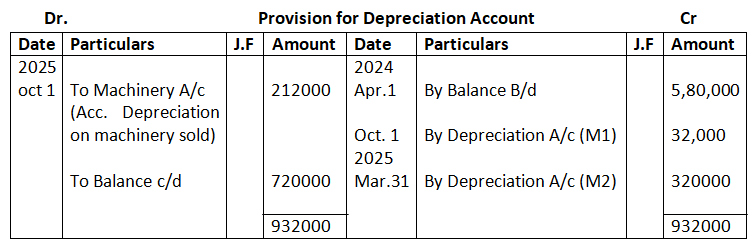

Solution:-

Dr Machinery Account Cr

Working Note:

Depreciation provided on Machinery sold till 1st October, 2024

For (2022 – 23) 50,000 x 20% – 1,00,000

For (2023 – 24) (50,000 – 1,00,000) x 20% – 80,000

For (2024 – 25) (50,000 – 1,00,000 – 80,000) x 20% x 6/12 – 32000

Total Depreciation provided on Machinery sold 212000

Calculation of Depreciation provided for 2024 – 25 on remaining machinery

Balance of provision for Depreciation on 1st April 2024-25 5,80,000

Add: Depreciation provided on machinery sold 32,000

6,12,000

Less: Accumulated Depreciation on Machinery sold 2,12,000

Accumulated Depreciation on the remaining machinery 4,00,000

Cost of Remaining Machinery (25,00,000 – 5,00,000) = 20,00,000

Less: Accumulated Depreciation on remaining machinery 4,00,000

Book value of remaining machinery 16,00,000

Depreciation on remaining machinery (16,00,000 x 20%) 3,20,000

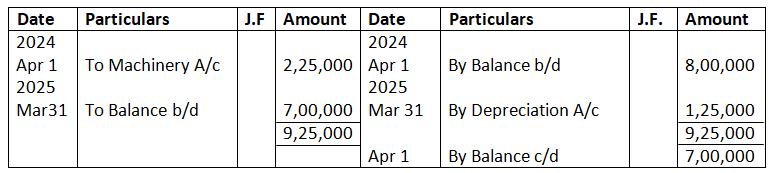

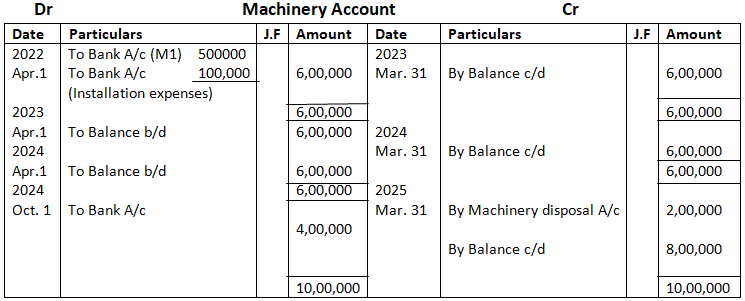

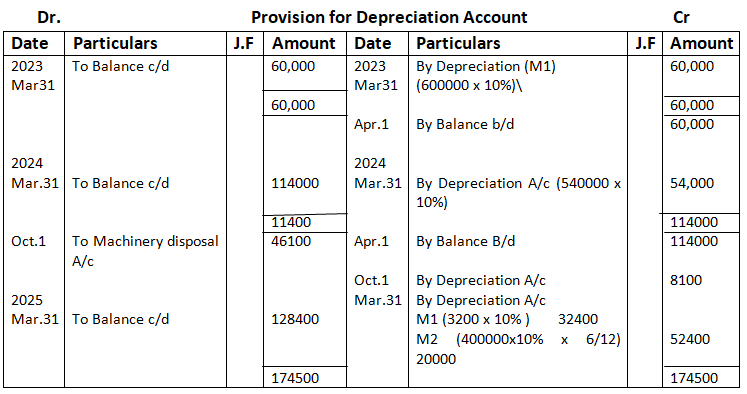

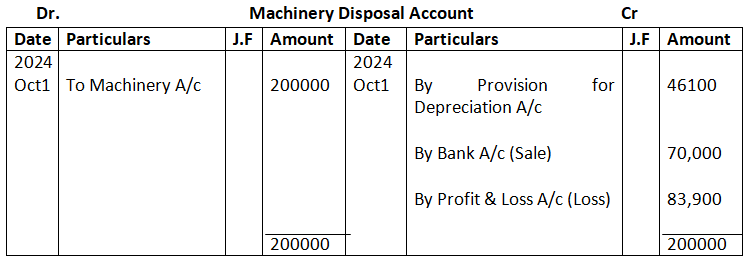

Q35. On 1st April, 2022, Jai purchased machinery for Rs.5,00,000 and spent Rs.1,00,000 on its installation. On 1st October, 2024, 1/3rd of machinery purchased on 1st April, 2022 was sold for Rs.70,000 and a new machinery at the cost of Rs.4,00,000 was purchased on the same date. The company has adopted the written down value method of providing depreciation @ 10% p.a. on the machinery.

You are required to show: (i) Machinery Account; (ii) Machinery disposal Account and (iii) Provision for Depreciation Account for the period of three accounting years ended 31st March, 2025.

Solution:-

Working Note:

Depreciation Provided on Machinery sold till 1st October 2024

For (2022-23), 6,00,000 x 1/3 x 10% – 20,000

For (2023-24) (2,00,000 – 20,000) x 10% – 18,000

For (2024-25) (180,000 – 18,000) x 10% x 6/12 – 81,000

Total Depreciation Provided on Machinery sold – 46,100

Calculat of Depreciation Provided for 2024 – 25

Balance of Provision for Depreciation on 1st April 2024-25 – 114000

Add: Depreciation provided on machinery sold – 8100

122100

Less: Accumulated Depreciation on machinery sold (w.N.1) 46100

Accumulated Depreciation on the remaining machinery 76,000

Cost of Remaining Machinery (6,00,000 – 2,00,000) – 4,00,000

Less: Accumulated Depreciation on remaining machinery (as above) 76,000

Book Value of Machinery 324000

Depreciation on remaining Machinery for 2024 – 25 (324000 x 10%) 32400