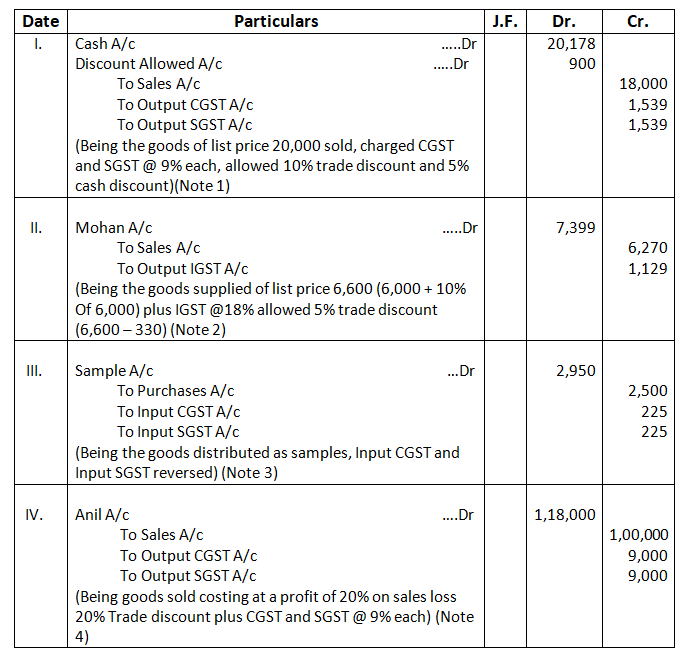

Q1. Journalise the following transactions in the books of Gurman of Delhi:

- Sold goods to Krishna of Delhi at the list price 20,000 less trade discount 10% add CGST and SGST @9% each., and allowed cash discount 5%. He paid the amount immediately.

- Supplied goods costing 6,000 to Mohan of Kolkata issued invoice at 10% above cost less 5% trade discount plus IGST @ 18%

- Goods valued at 2,500 distributed from stock as samples as part of an advertising campaign. These goods were purchased paying CGST and SGST @ 9% each.

- Sold goods costing 1, 00,000 to Anil of Delhi at a profit of 20% on sales less 20% Trade Discount plus CGST and SGST @ 9% each.

Solution – Journal Entries

Working Note:-

- Sold Goods to Krishna = 20,000

Less Trade Discount (10%) = 2,000

= 18,000

Less Cash Discount (5%) = 900

= 17,100

Add: CGST (9%) = 1,539

SGST (9%) = 1,539

= 20,178

II. Cost of Goods Sold = 6,000

Add: 10% (Issue Invoice) = 600

= 6,600

Less: Trade Discount (5%) = 330

= 6270

Add: IGST 18% = 1,129

= 7,399

III. Goods given as Sample = 2,500

+ CGST (9%) = 225

+ SGST (9%) = 225

= 2,950

IV. Cost of Goods sold = 1,00,000

Add: Profit on cost (20%) = 20,000

= 1, 20,000

Less: Trade Discount = 24,000

= 1,00,000

Add: CGST (9%) = 9,000

SGST (9%) = 9,000

= 1, 18,000

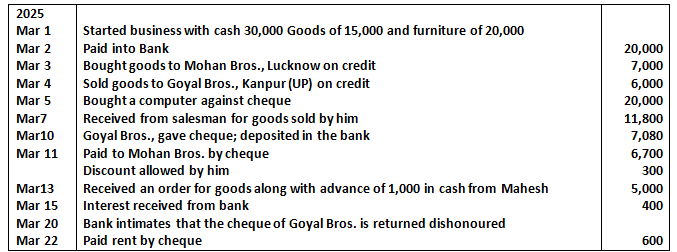

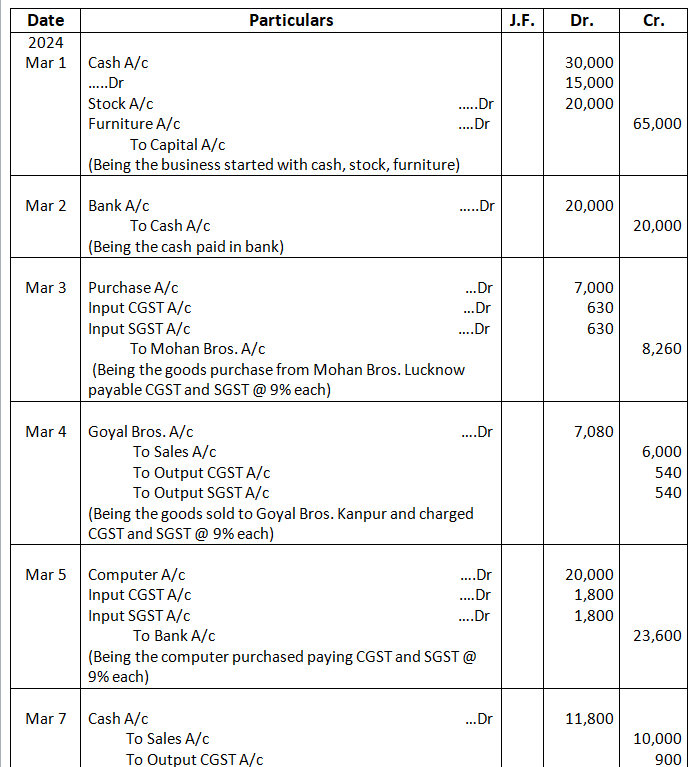

Q2. Journalise the following transactions in the books of Paresh Bros., Lucknow (UP):

Solution – Journal Entry

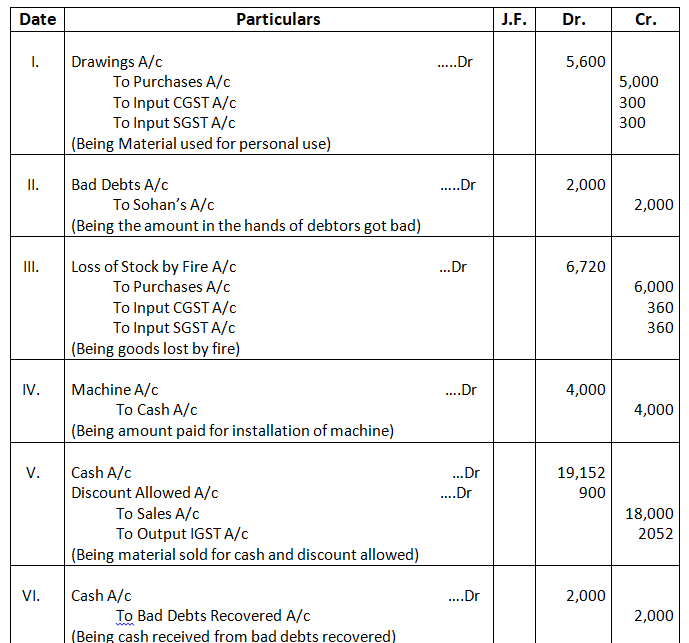

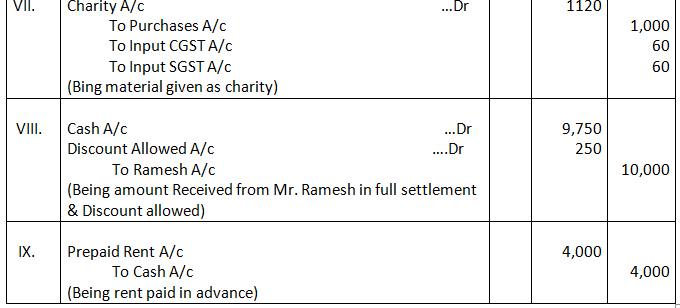

Q3. Journalise the following in the books of Amit Saini, Gurugram (Haryana):

- Goods of 5,000 out of goods purchased within the state were taken by him for personal use.

- 2,000 due from Sohan were bad debts.

- Goods of 6,000 were destroyed by fire and were not insured. These good were purchased from outside the state.

- Paid 4,000 in cash as wages on installation of machine. (GST is not to be Charged)

- Sold goods to Arjun of Delhi of list price 20,000. Trade discount @ 10% and cash discount of 5% was allowed. He paid the amount on the same day and availed the cash discount.

- Received 2,000 from Ramesh, whose account was written off as bad debts.

- Goods costing 1,000 given as charity. These goods were purchased from within the state.

- Received 9,750 from Ramesh in full settlement of his account of 10,000.

- Paid rent in advance 4,000.

CGST and SGST is to be levied on intra state sale @6% each and IGST @12% on interstate sale.

Solution – Journal Entries

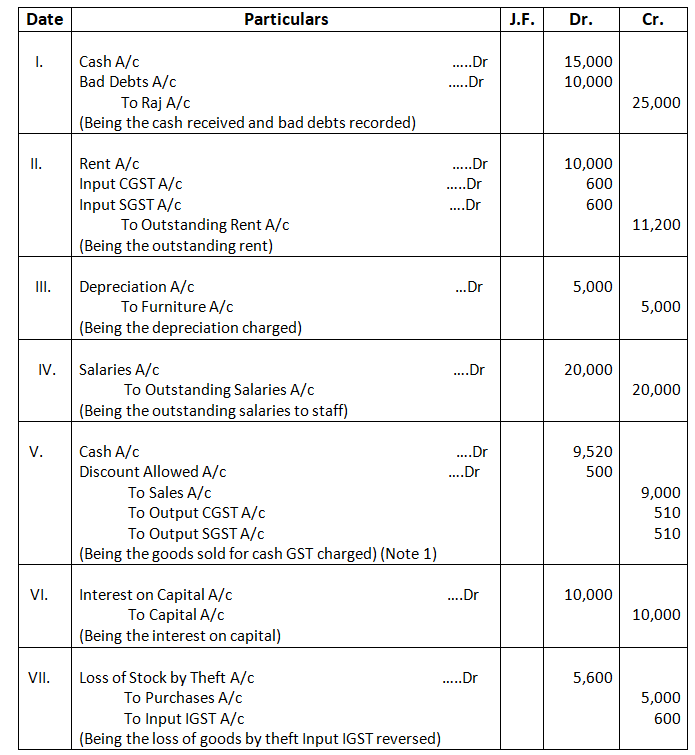

Q4. Journalise the following transactions in the books of Mohan, Delhi:

- Raj of Alwar, Rajasthan who owed Mohan 25,000 became insolvent and received 60 paise in a rupee as full and final settlement.

- Mohan owes to his landlord 10,000 as rent. GST payable @ 6% each.

- Charge depreciation of 10% on furniture costing 50,000.

- Salaries due to employee 20,000

- Sold to Sunil goods in cash of 10,000 less 10% trade discount plus CGST and SGST @ 6% each and received a net of 8,500 plus CGST and SGST.

- Provided interest on capital of 1, 00,000 @ 10% per annum.

- Goods lost in theft 5,000 which were purchased paying IGST @ 12% from Alwar, Rajasthan.

Solution – Journal Entries

Working Note –

Last Price = 10,000

Less: Trade Discount (10%) = 1,000

= 9,000

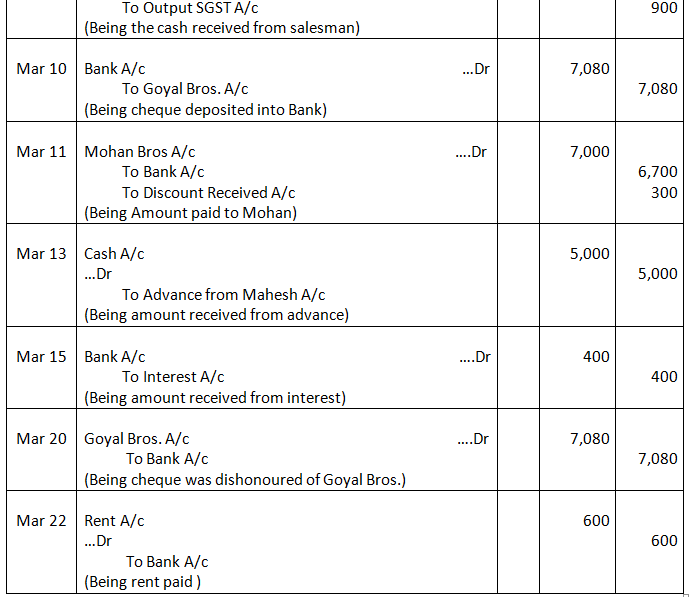

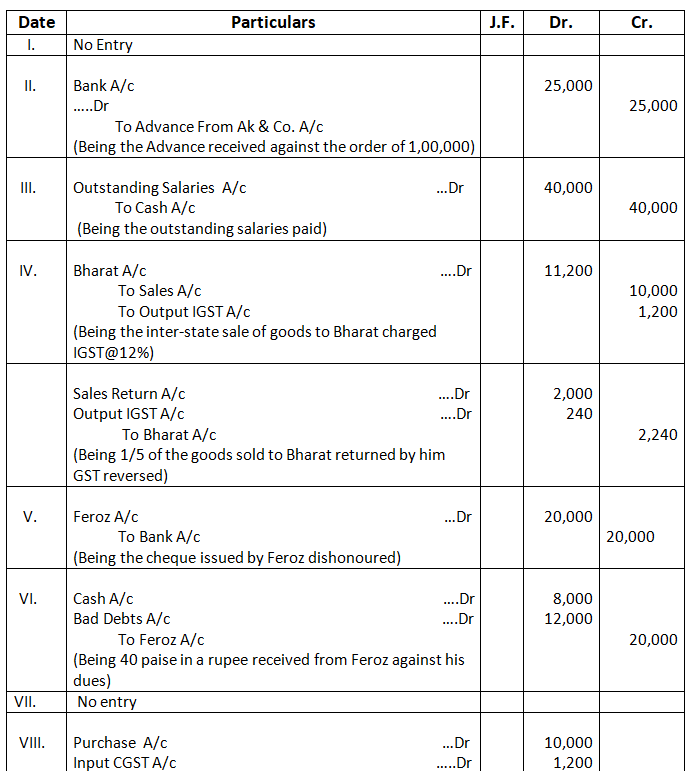

Q5. Pass Journal Entries in the books of Puneet, Delhi for the following:

- Received an order from Karan & Co. for supply of goods of 50,000.

- Received an order from AK & Co. for goods of 1, 00,000 along with a cheque for 25,000 an advance.

- Paid to staff 40,000 against outstanding salaries of 60,000.

- Sold goods to Bharat, Kaithal (Haryana) of 10,000 plus IGST @ 12% out of which 1/5th were returned by Bharat being defective.

- Cheque of 20,000 issued by Feroz was dishonoured.

- Received 40 paise in a rupee from Feroz against the above dues.

- Received a cheque of 25,000 from Mohan after banking hours.

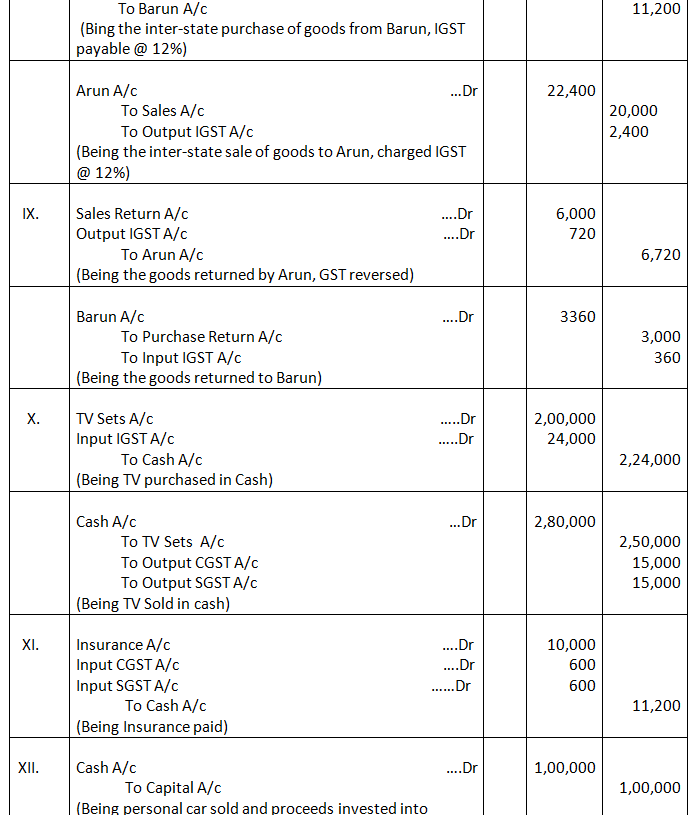

- Purchased goods from Barun of Chandigarh of 10,000 plus IGST @ 12% and sold them to Arun of Shimla (HP) at 22,400, including IGST @ 12%

- Arun returned goods of 6,720, including IGST which were returned to Barun.

- Puneet purchased 10TV sets @ 20,000 per set and paid IGST @ 12%. It sold all the sets @ 25,000 per set plus CGST and SGST @ 6% each

- Paid insurance of 11,200 including CGST and SGST @ 6% each for a period of one year.

- Sold personal car for 1, 00,000 and invested the amount in the firm.

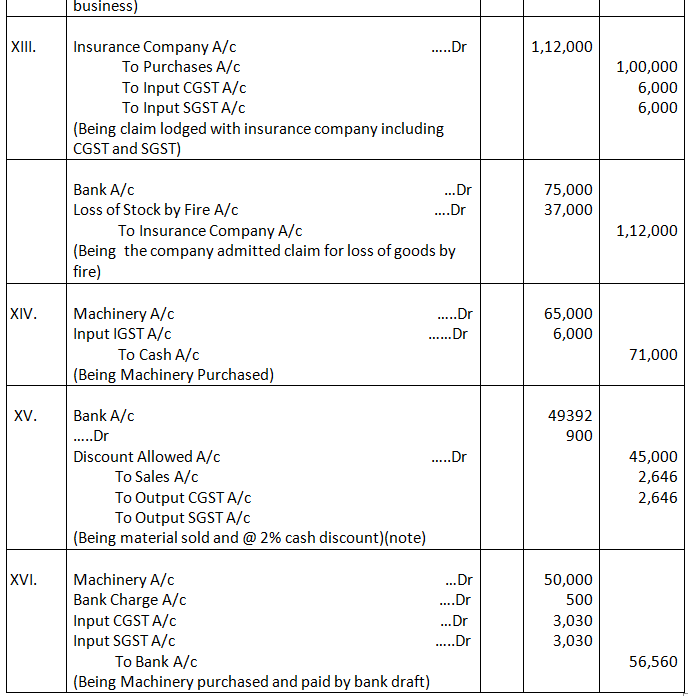

- Goods costing 1, 00,000 were destroyed in fire. Insurance company admitted the claim for 75,000. These goods were purchased within Delhi paying CGST and SGST @ 6% each.

- Purchased machinery for 56,000 including IGST of 6,000 and paid cartage thereon 5,000 and installation charges 10,000.

- Goods costing 40,000 sold to Kapil at a profit of 20% on sales less 10% Trade Discount plus CGST and SGST @ 6% each and received a cheque under 2% cash discount.

- Purchased machinery from New Machinery House for 50,000 and paid it by bank draft from bank. Paid bank charges 500. Bank charged CGST and SGST @ 6% each on Bank charges.

Solution – Journal Entries

Working Note – Cost of Goods Sold = 40,000

Add: Profit of sales (20%) = 10,000

List Price = 50,000

Less: Trade Discount (10%) = 5,000

= 45,000

Less: Cash discount (2%) = 900

44100

Add CGST (6%) = 2646

Add: SGST: (6%) = 2646

49392

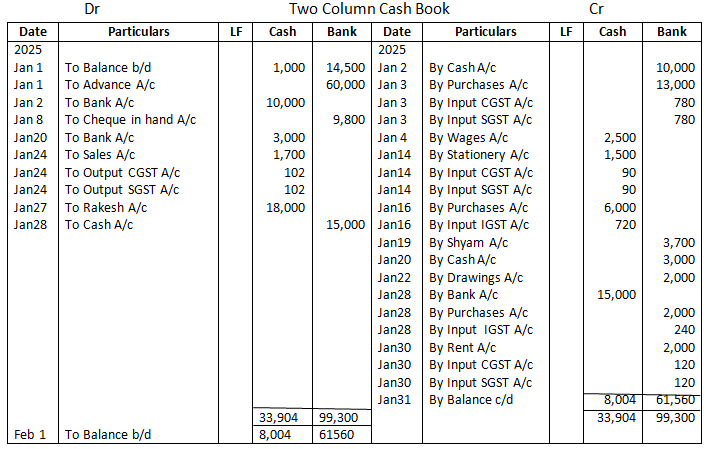

Cash Book

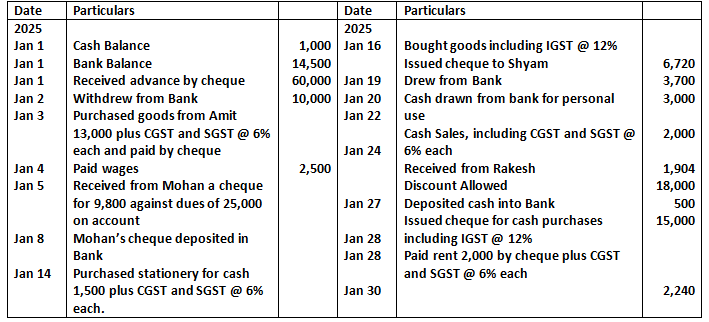

Q6. Record the following transactions of Sumant, Kochi in a Two-column Cash Book and balance the book on 31st January, 2025:

Solution – In the Books of Sumanto, Kochi

Purchase Book

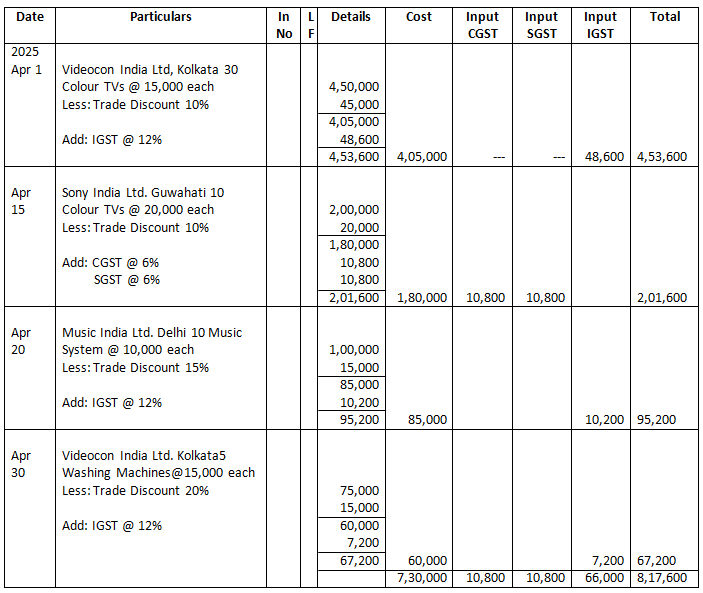

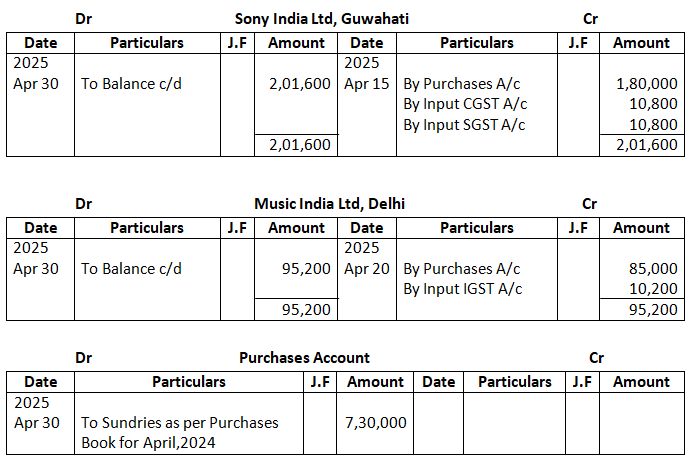

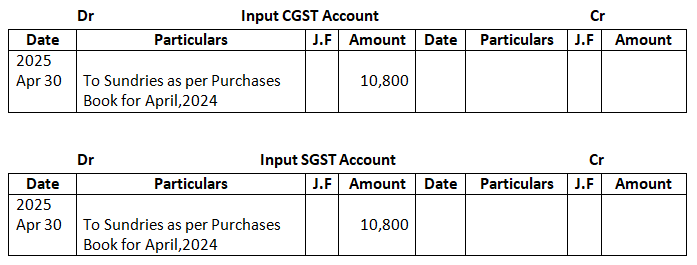

Q7. From the following transactions of Kamal, Guwahati, Prepare Purchases Book and post into Ledger:

Solution – In the Book of Kamal, Guwahati

Purchases Book

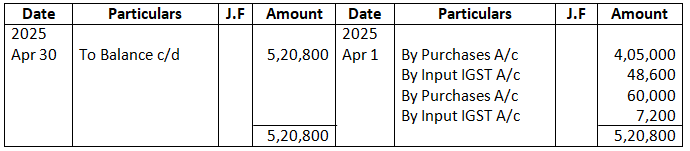

LEDGER:

Dr Videocon India Ltd, Kolkata Cr

Sales Book

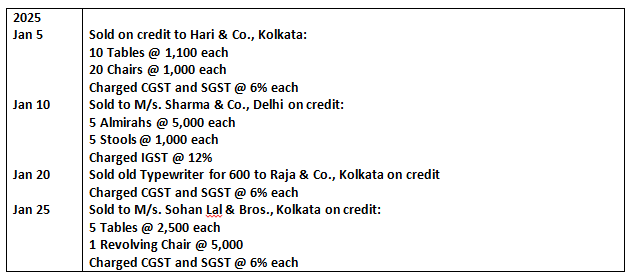

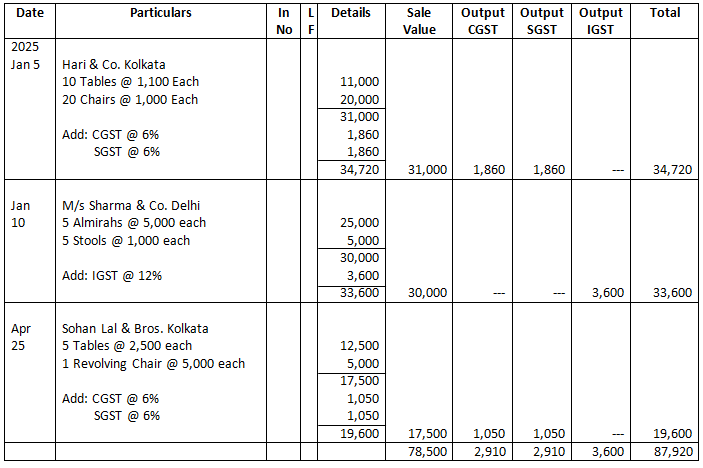

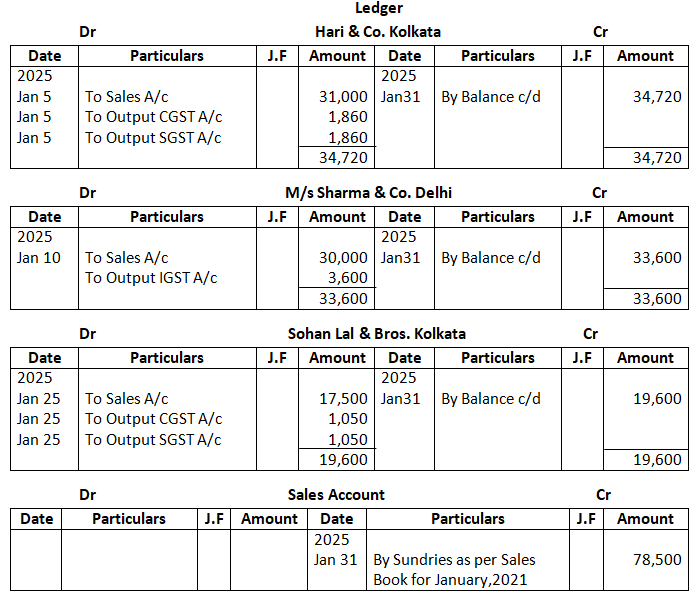

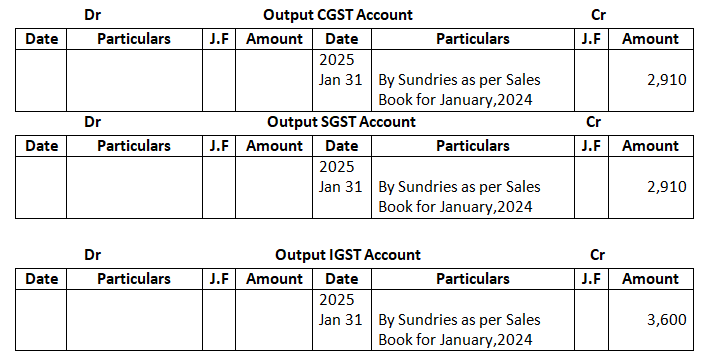

Q8. From the following particulars, prepare Sales Book of Gupta & Co., Kolkata who deals in furniture:

Show the Posting from Sales Book to Ledger Account.

Solution – In the Book of Gupta & Co Kolkata

Sales Book

Purchases Return Book

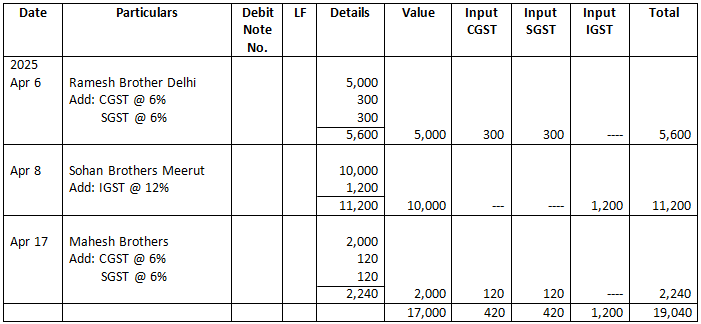

Q9. Record the following transactions in the Purchases Return Book of Kamla Stores, Delhi for April, 2025:

Solution –

Sales Return Book

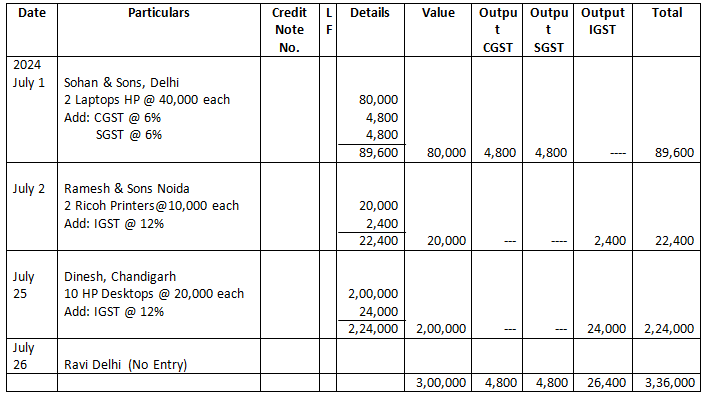

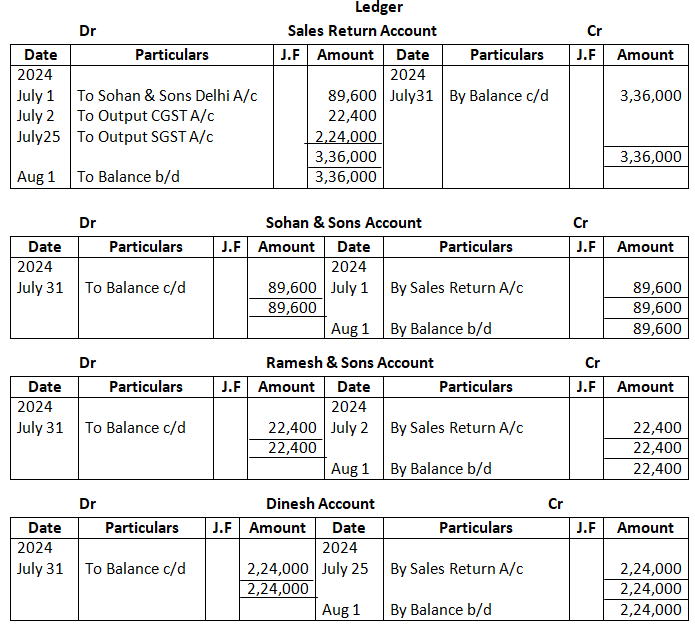

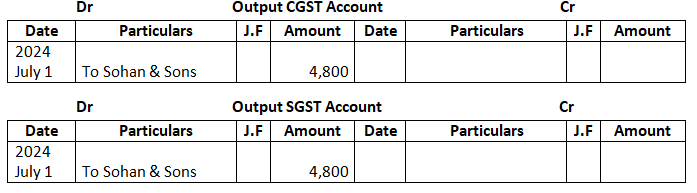

Q10. Enter the following transactions in the Sales Return Book of Raj Computers, Delhi:

Show its posting to Ledger Accounts

Solution –

GST Set Off

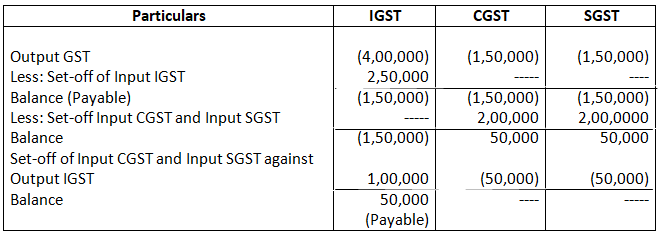

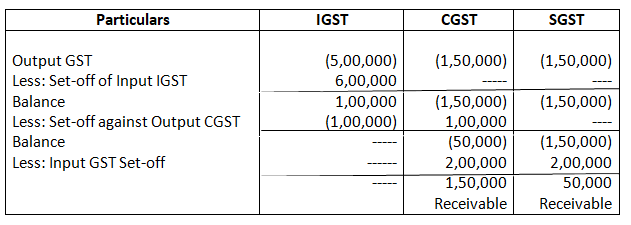

Q11. Gurman has following balances in his GST Accounts as on 31st March, 2025:

Pass the Journal entries for set-off of GST.

Solution –

Q12 Naman has following balance in his GST Account as on 31st March, 2025:

Pass the Journal entries for set-off of GST.

Solution: