Numerical Questions

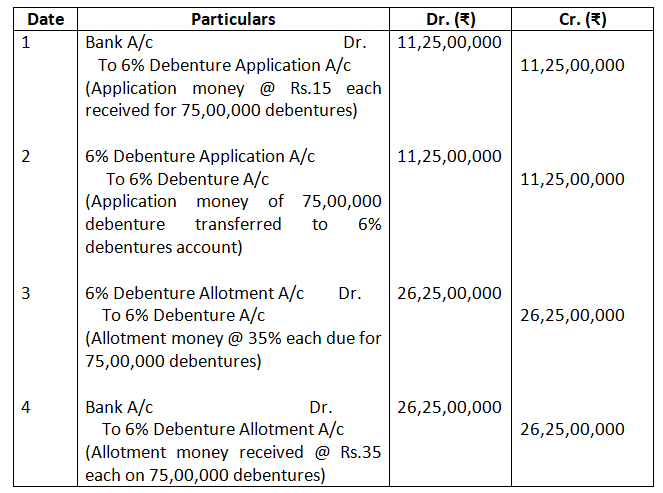

- G. Ltd. Issued 75,00,000, 6% Debenture of Rs.50 each at par payable Rs.15 on application and Rs.35 on allotment, redeemable at par after 7 years from the date of issue of debenture. Record necessary entries in the books of company.

Solution:-

Books of G. Ltd.

Journal

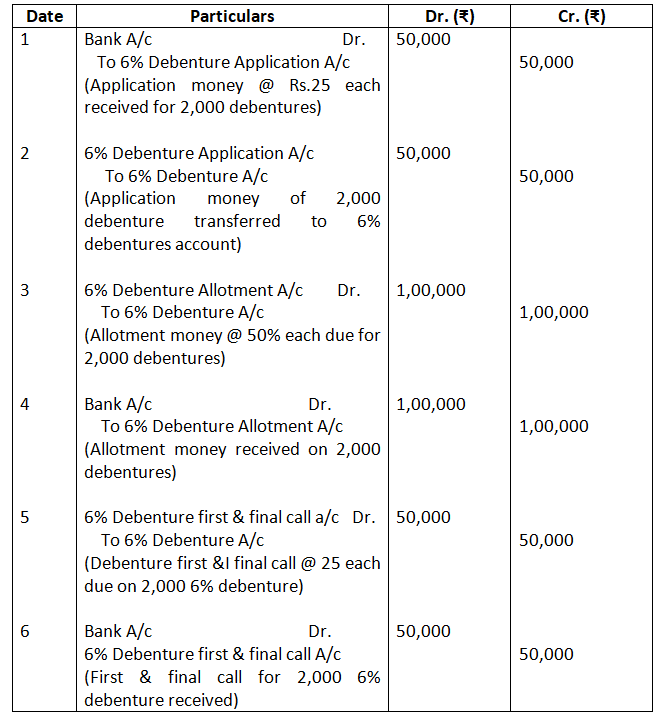

2. Y. Ltd., issued 2,000, 6% Debenture on Rs.100 each payable as follows: RS.25 on application; Rs.50 on allotment and Rs.25 on first and final call.

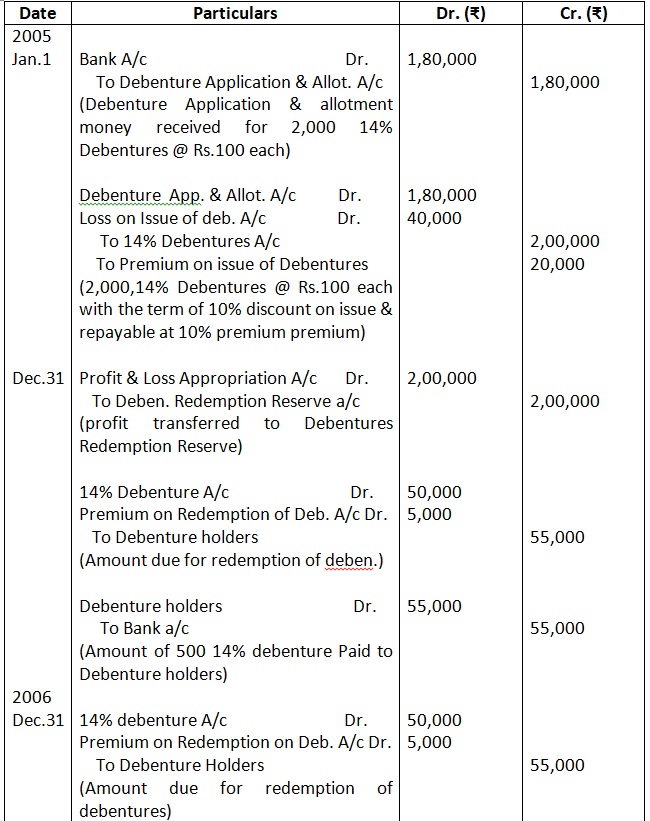

Solution:-

Books of Y. Ltd.

Journal

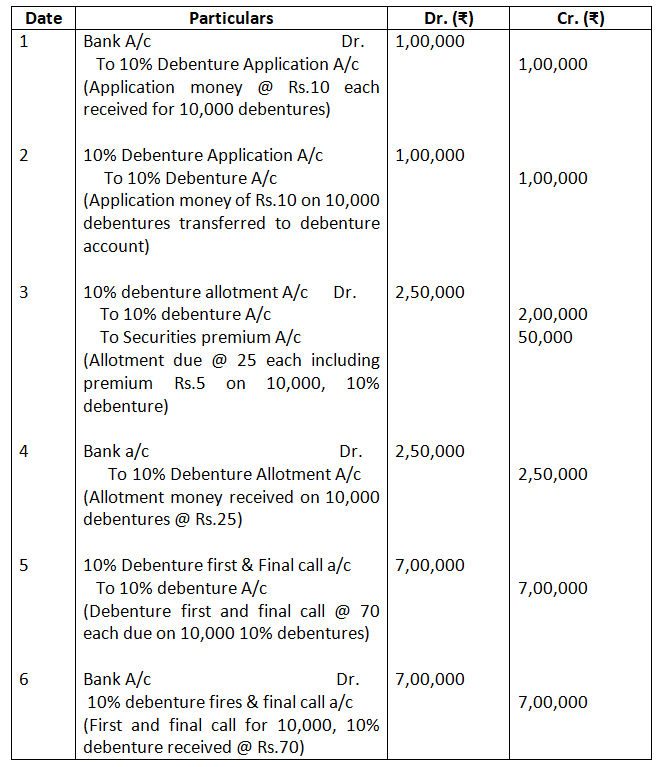

3. A. Ltd., issued 10,000, 10% Debenture of Rs.100 each at a premium of 5% payable as follows:

Rs.10 on Application;

Rs.20 along with premium on allotment and balance on First and final call. Record necessary Journal Entries.

Solution:-

Books of A. Ltd.

Journal

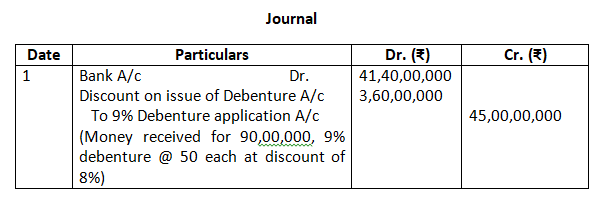

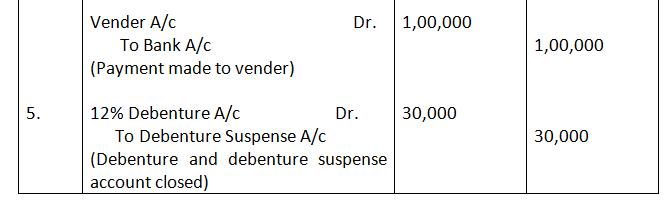

4. A. Ltd., issued 90,00,000, 9% Debenture of Rs.50 each at a discount of 8%, redeemable at par any time after 9 years. Record necessary entries in the books of A. Ltd.

Solution:-

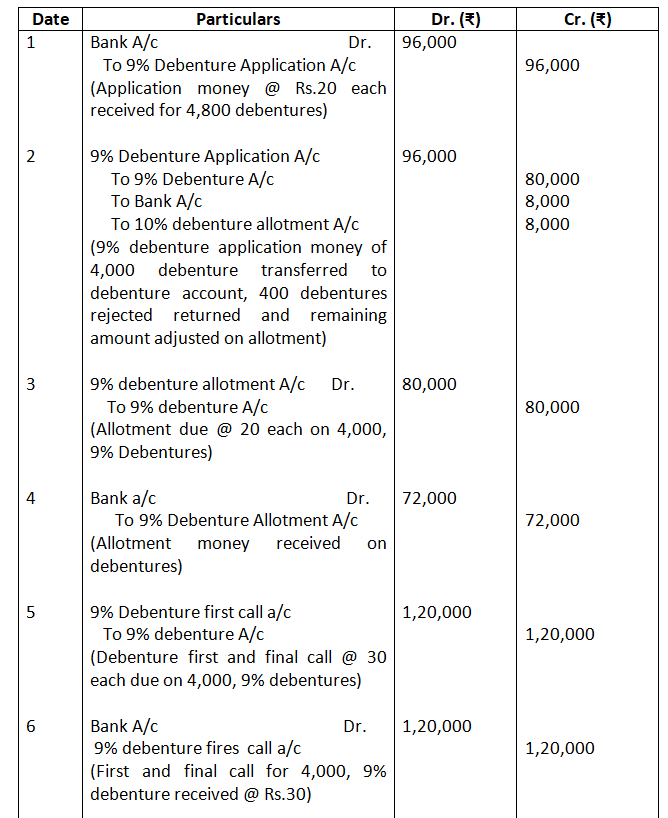

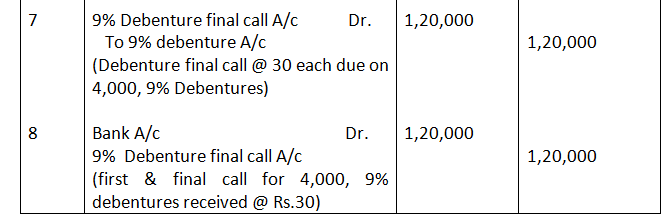

5. A. Ltd., issued 4,000, 9% Debenture of Rs.100 each on the following terms:

Rs.20 on Application;

Rs.20 on Allotment;

Rs.30 on First call; and

Rs.30 on Final call.

The public applied for 4,800 Debentures. Applications for 3,600 Debentures were accepted in full. Application for 800 Debentures were allotted 400 Debentures and applications for 400 Debentures were rejected.

Solution:-

Books of A. Ltd.

Journal

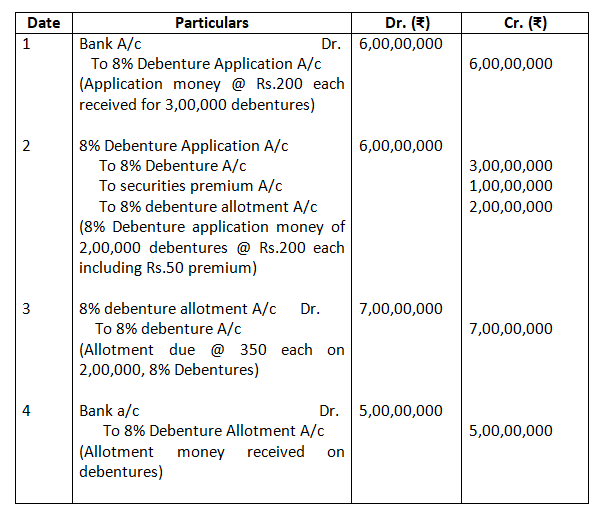

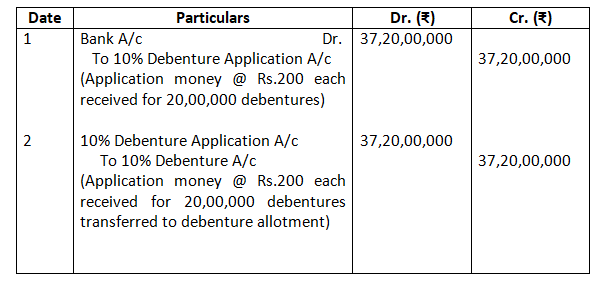

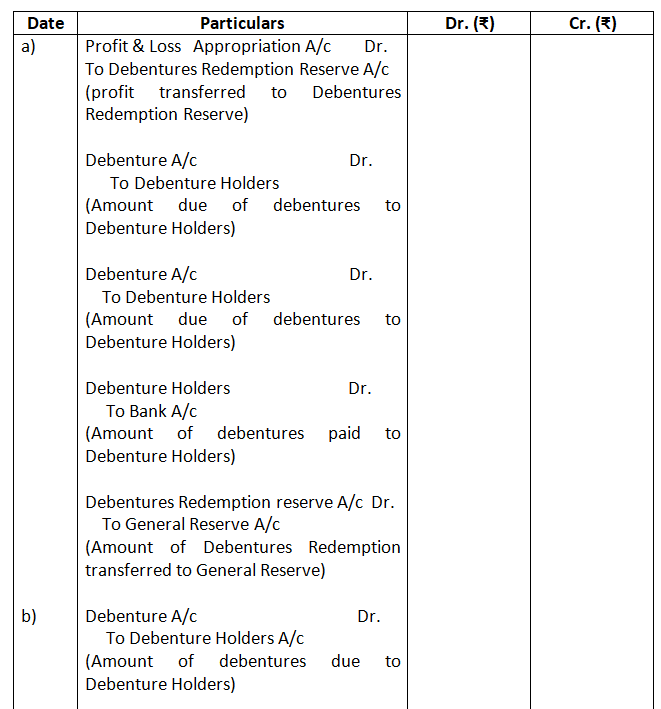

6. T. Ltd., offered 2,00,000, 8% Debenture of Rs.500 each on June 30, 2002 at a premium of 10% payable as Rs.200 on application (including premium) and balance on allotment, redeemable at par after 8 years. But application are received for 3,00,000 debenture and the allotment is made on pro-rata basis. All the money due on application and allotment is received. Record necessary entires regarding issue of debenture.

Solution:-

Books of T. Ltd.

Journal

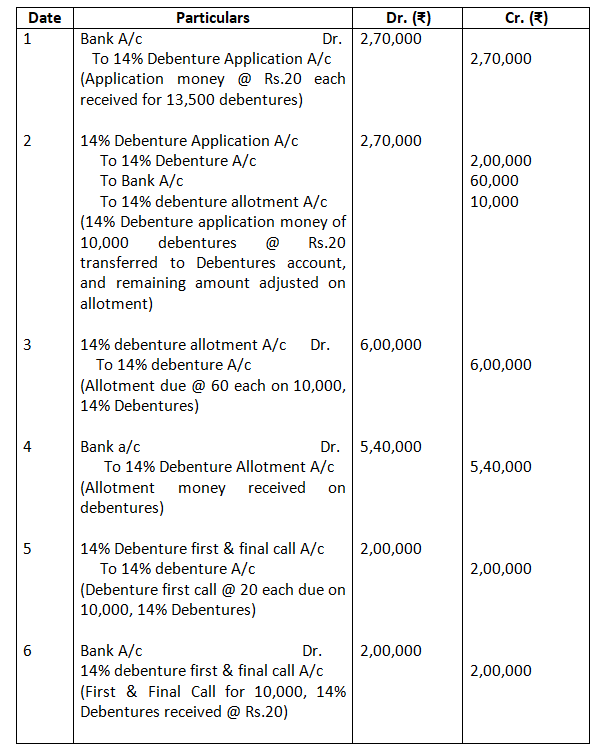

7. X. Ltd., invites application for the issue of 10,000, 14% debentures of Rs.100 each payable as to Rs.20 on application, Rs.60 on allotment and the balance on call. The company receives application for 13,500 debentures, out of which applications for 8,000 debentures are allotted in full, 5,000 only 40% and the remaining rejected. The surplus money on partially allotted applications is utilized towards allotment. All the sums due are duly received.

Solution:-

Books of X. Ltd.

Journal

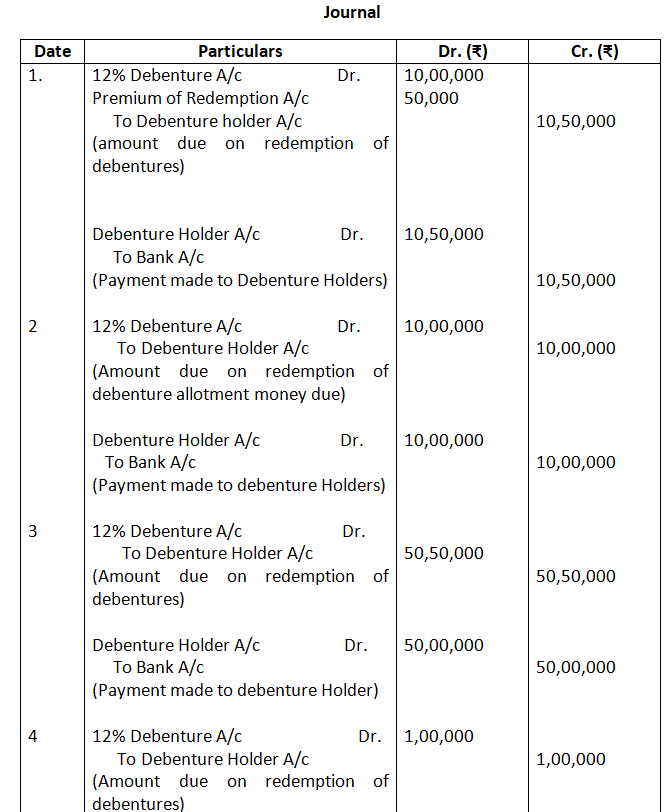

8. R. Ltd., offered 20,00,000, 10% Debenture of Rs.200 each at a discount of 7% redeemable at premium of 8% after 9 years. Record necessary entries in the books of R. Ltd.

Solution:-

Books of R. Ltd.

Journal

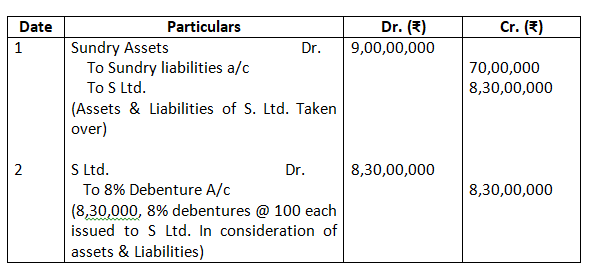

9. M. Ltd., took over assets of Rs.9,00,000 and liabilities of Rs.70,00,000 of S. Ltd. And issued 8% Debenture of Rs.100 each. Record necessary entries in the books of M. Ltd.

Solution:-

Books of M. Ltd.

Journal

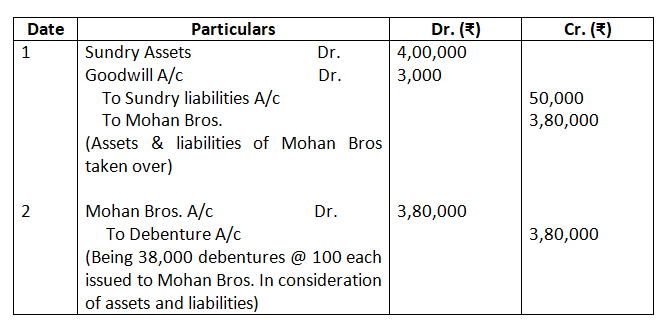

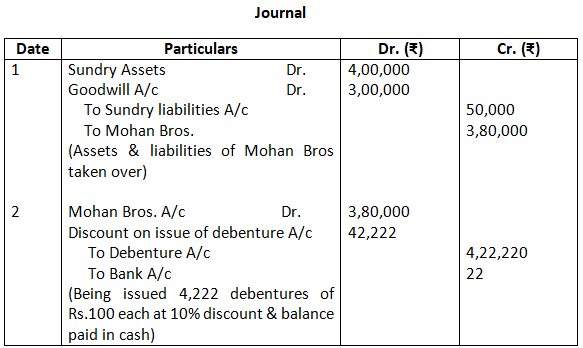

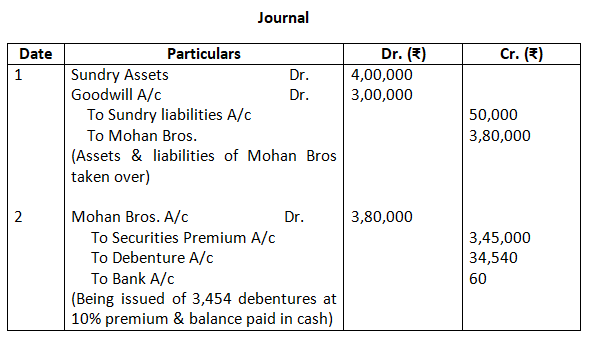

10. B. Ltd., purchased assets of the book value of Rs.4,00,000 and took over the liability of Rs.50,000 from Mohan Bros. It was agreed that the purchase consideration, settled at Rs.3,80,000, be paid by issuing debentures of Rs.100 each.

What journal entires will be made in the following three cases, if debentures are issued: a) at par; b) at discount; c) at premium of 10%? It was agreed that any fraction of debentures be paid in cash.

Solution:-

Case (a)

Journal

Case (b)

Case (c)

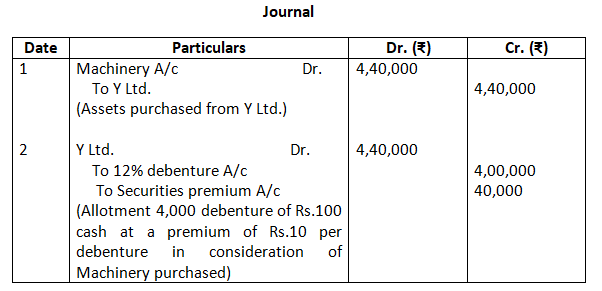

11. X. Ltd., purchased a Machinery from Y for an agreed purchase consideration of Rs.4,40,000 to be satisfied by the issue of 12% debentures of Rs.100 each at a premium of Rs.10 per debenture. Journalise the transactions.

Solution:-

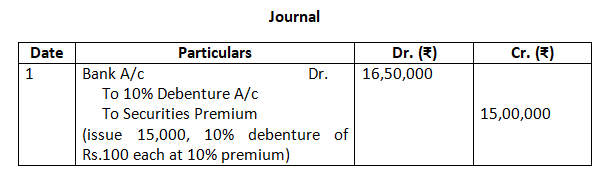

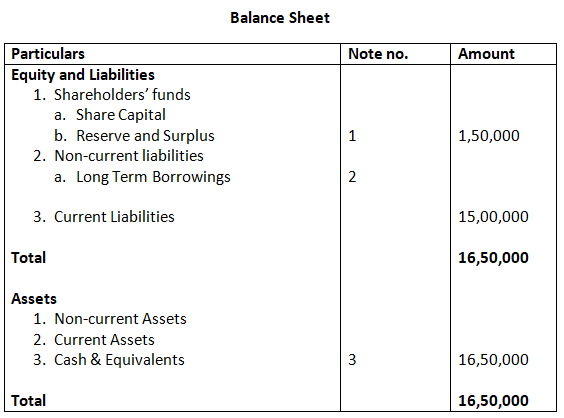

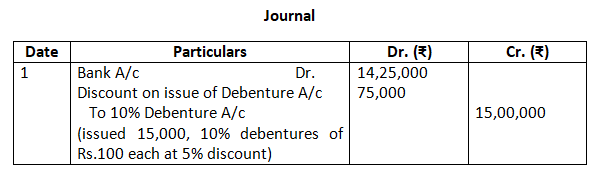

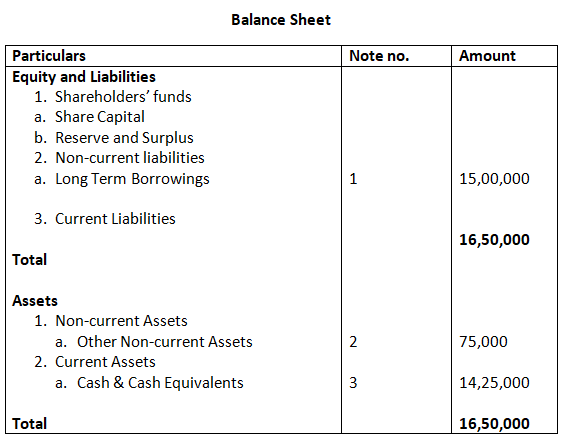

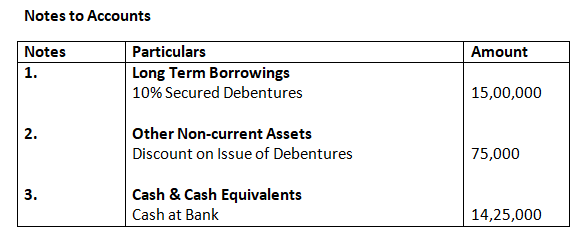

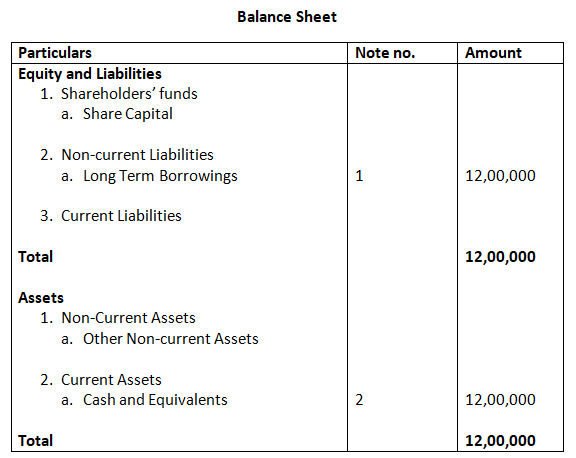

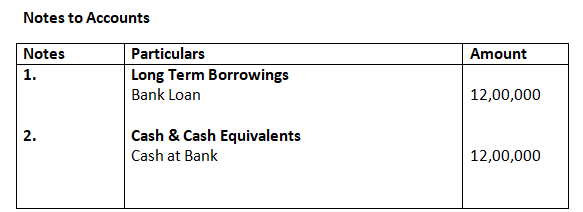

12. X. Ltd., issued 15,000, 10% debentures of Rs.100 each. Give journal entires and the balance sheet in each of the following cases:

- The debentures are issue at a premium of 10%;

- The debentures are issued at a discount of 5%;

- The debentures are issued as a collateral security to bank against a loan of Rs.12,00,000; and

- The debenture are issued to a supplier of machinery costing Rs.13,50,000.

Solution:-

Case (i)

Case (ii)

Cash (iii) No Journal entries

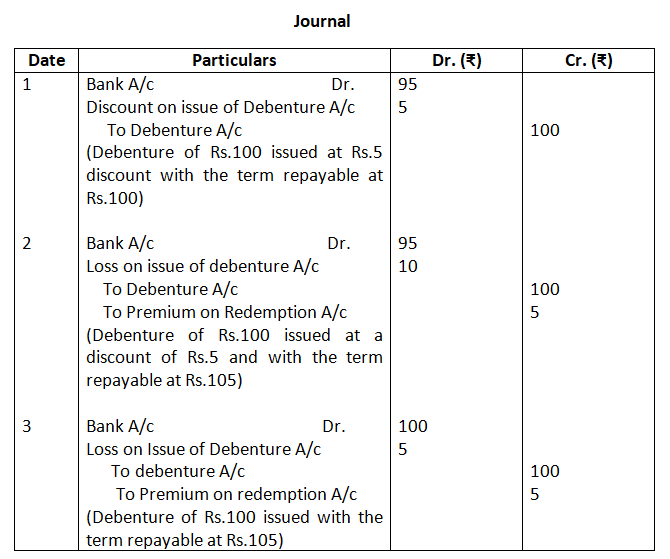

13. Journalise the following :

- A debenture issued at Rs.95, repayable at Rs.100;

- A debenture issued at Rs.95, repayable at Rs.105; and

- A debenture issued at Rs.100, repayable at Rs.105;

The face value of debenture in each of the above cases is Rs.100.

Solution:-

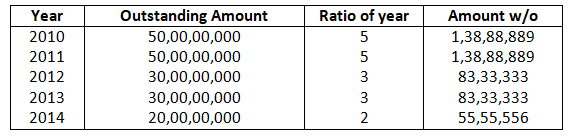

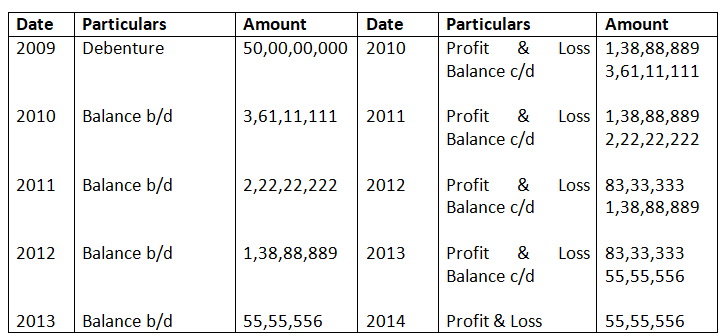

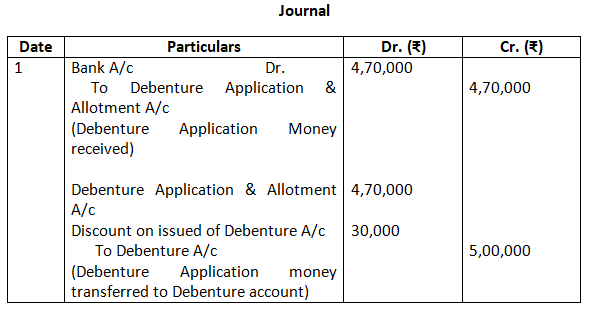

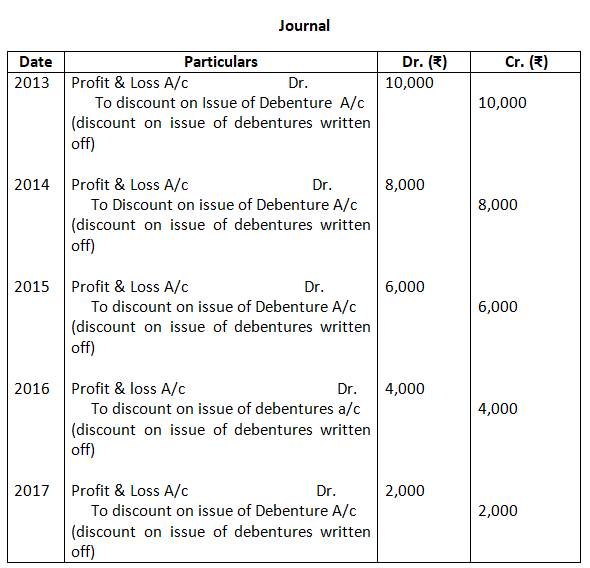

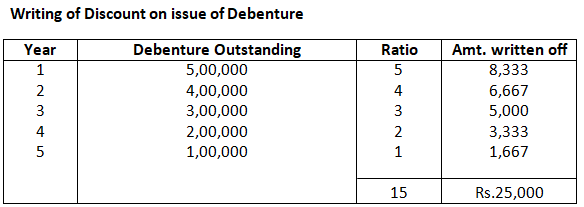

14. A. Ltd. Issued 50,00,000, 8% Debenture of Rs.100 at a discount of 6% on April 01, 2000 redeemable at premium of 4% by draw of lots as under;

20,00,000 debenture on March, 2002

10,00,000 Debenture on March, 2004

20,00,000 Debenture on March, 2005

Compute the amount of discount to be written-off in each year till debentures are paid. Also prepare discount/loss on issue of debenture account.

Solution:-

Loss on issue of debenture = 6% discount on issue + 4% redemption premium = 10% = 5000,000 x 100 x 10/100 = 5,00,00,000

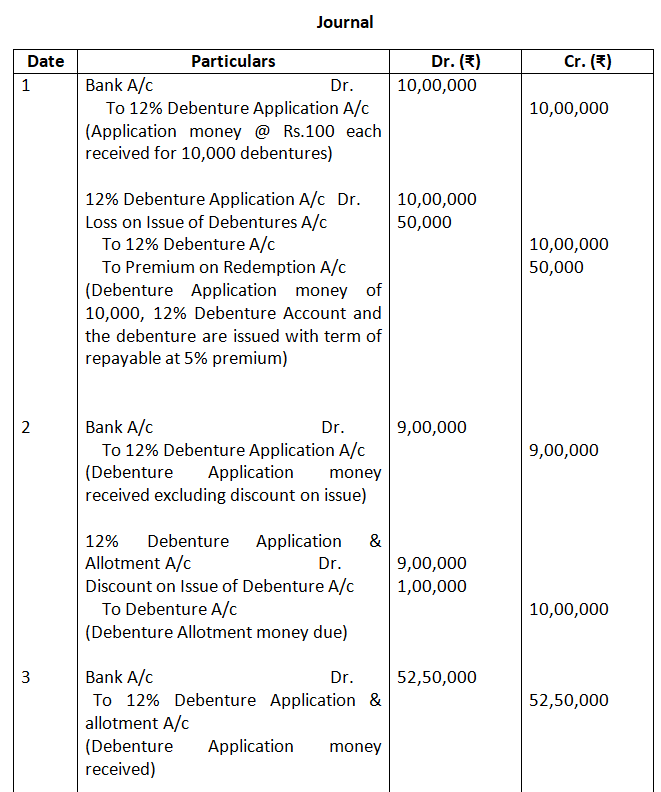

15. A company issues the following debentures:

- 10,000, 12% debenture of Rs.100 each at par but redeemable at premium of 5% after 5 years:

- 10,000, 12% debentures of Rs.100 each at a discount of 10% but redeemable at par after 5 years;

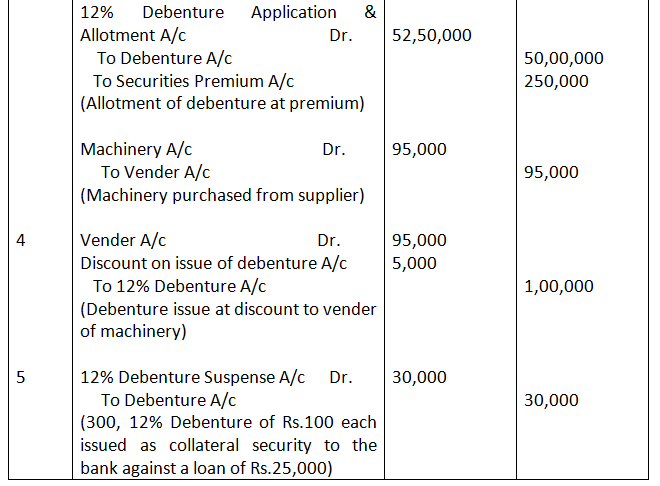

- 5,000, 12% debentures of Rs.1,000 each at a premium of 5% but redeemable at par after 5 years;

- 1,000, 12% debentures of Rs.100 each issued to a supplier of machinery costing Rs.95,000. The debentures are repayable after 5 years; and

- 300, 12& debentures of RS.100 each as a collateral security to a bank which has advanced a loan of Rs.25,000 to the company for a period of 5 years.

Pass the journal entries to record the: a) issue of debentures; and b) repayment of debentures after the given period.

Solution:-

- Issue of Debentures

b) Repayment of Debentures

16. A company issued debentures of the face value of Rs.5,00,000 at a discount of 6% on January 01, 2001. These debentures are redeemable by annual drawings of Rs.1,00,000 made on December 31 each year. The decided to write off discount based on the debentures outstanding each year. Calculate the amount of discount to be written-off each year. Give journal entries also.

Solution:-

Amount of Discount on issue of debenture = 5,00,000 x 6/100 = 30,000

(Written off in 5 years)

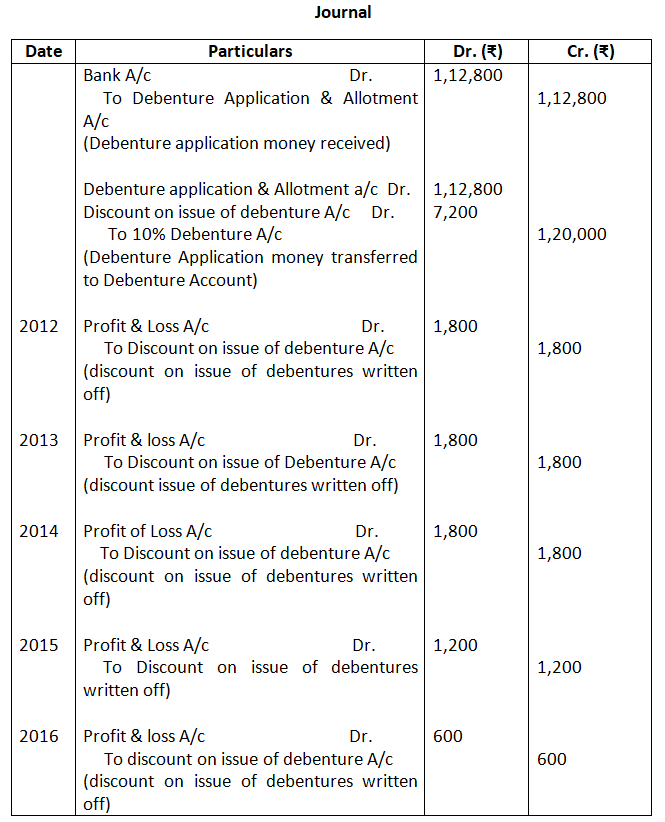

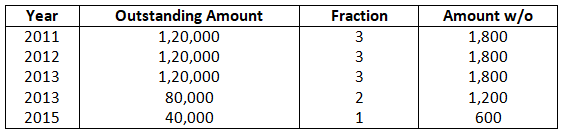

17. A company issued 10% Debentures of the face value of Rs.1,20,000 at a discount of 6% on January 01, 2001. The debentures are payable by annual drawings of Rs.40,000 commencing from the end of third year. How will you deal with discount on debentures? Show the discount on debentures account in the company ledger for the period of duration of debentures. Assume accounts are closed on December 31.

Solution:-

Amount of Discount Issue of Debentures = 1,20,000 x 6/100 = 7,200 (Written off in 5 years)

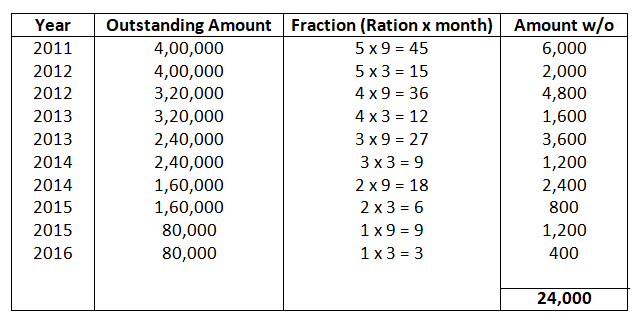

18. B. Ltd., issued debentures at 94% for Rs.4,00,000 on April 01, 2000 repayable by five equal drawings of Rs.80,000 each. The company prepares its final accounts on December 31 every year.

Indicate the amount of discount to be written-off every accounting year assuming that the company decides to write off the debentures discount during the life of debentures. (Amount to be written-off: 2000 Rs.6,000; 2001 Rs.6,800; 2002 Rs.5,200; 2003 Rs.3,600; 2004 Rs.2,000; 2005 RS.400).

Solution:-

Debenture issued = 4,00,000 @ 94%

Discount on issue = 6%

Amount of Discount on Issue = 4,00,000 x 6/100 = 24,000

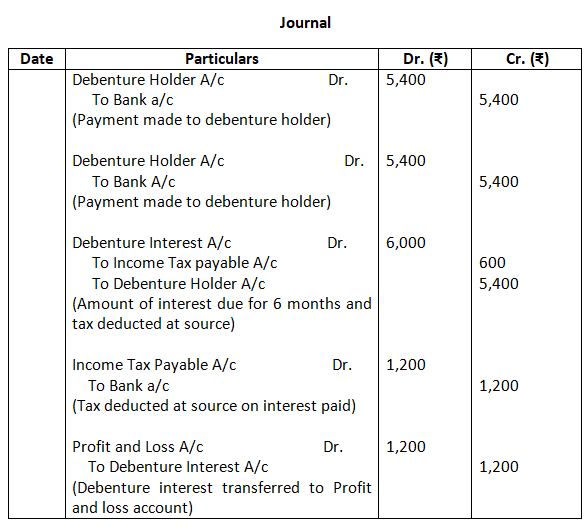

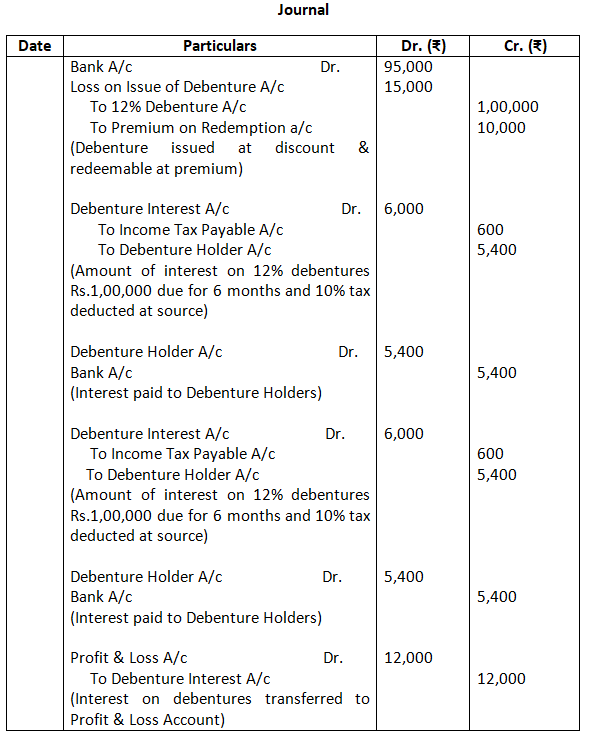

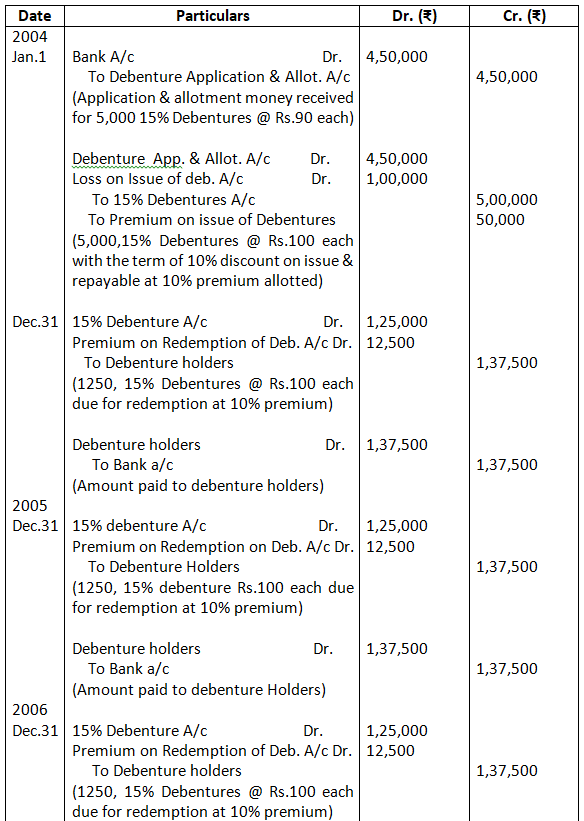

19. B. Ltd., issued 1,000, 12% debentures of Rs.100 each on January 01, 2005 at a discount of 5% redeemable at a premium of 10%. Give journal entires relating to the issue of debentures and debentures interest for the period ending December 31, 2005 assuming that interest is paid half yearly on June 30 and December 31 and tax deducted at source is 10%. B. Ltd., follows calendar year as its accounting year.

Solution:-

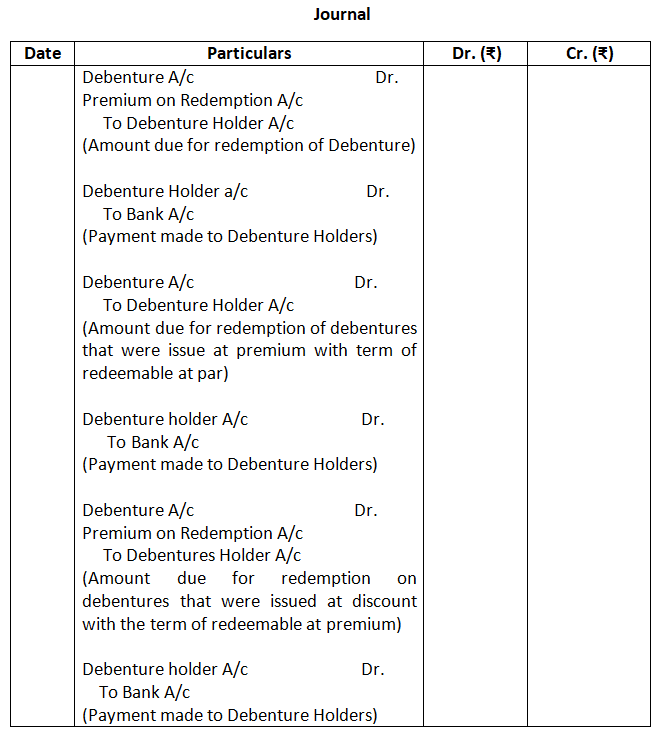

20. What journal entries will be made in the following cases when company redeems debentures at the expiry of period by serving the notice; a) when debentures were issued at par with a condition to redeem them at premium; b) when debentures were issued at premium with a condition to redeem that at par; and c) when debenture were issued at discount with a condition to redeem them at premium?

Solution:-

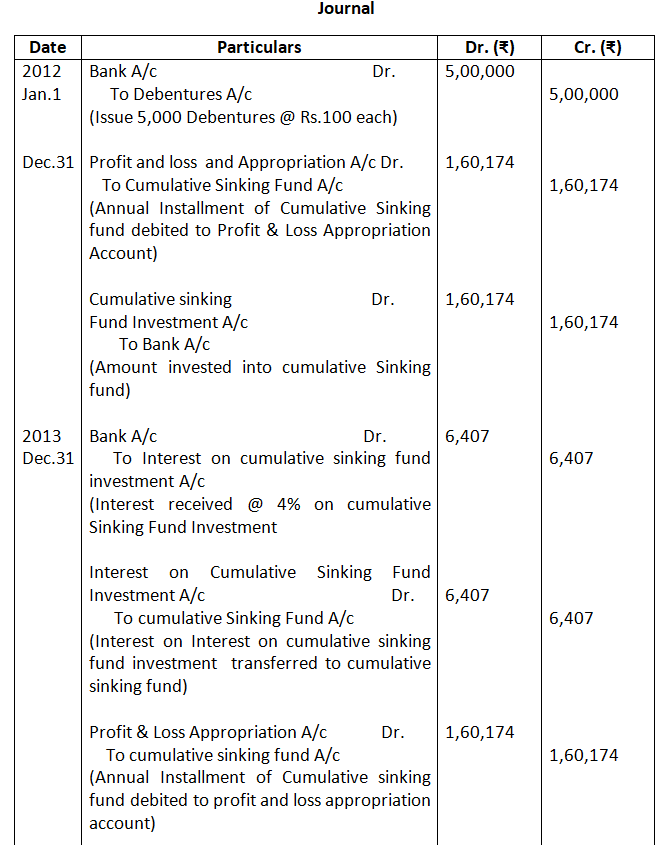

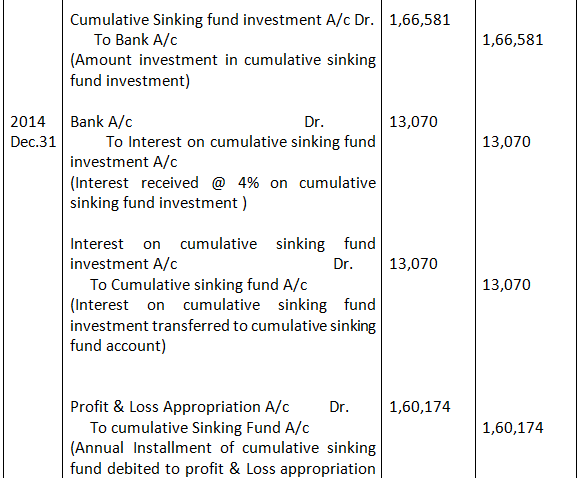

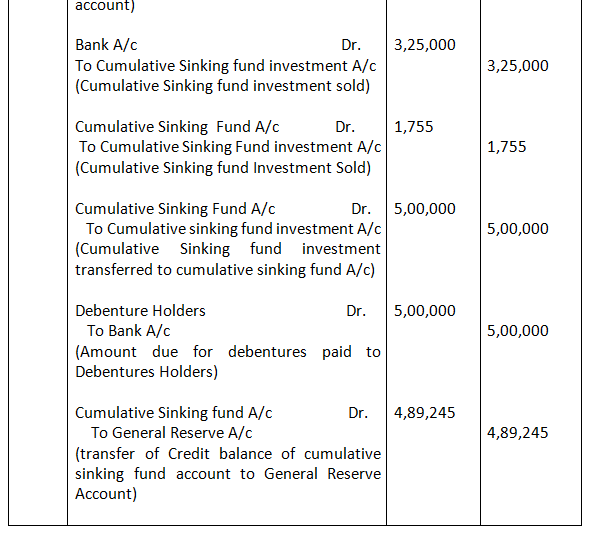

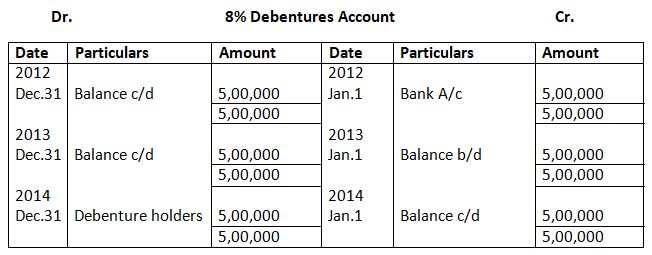

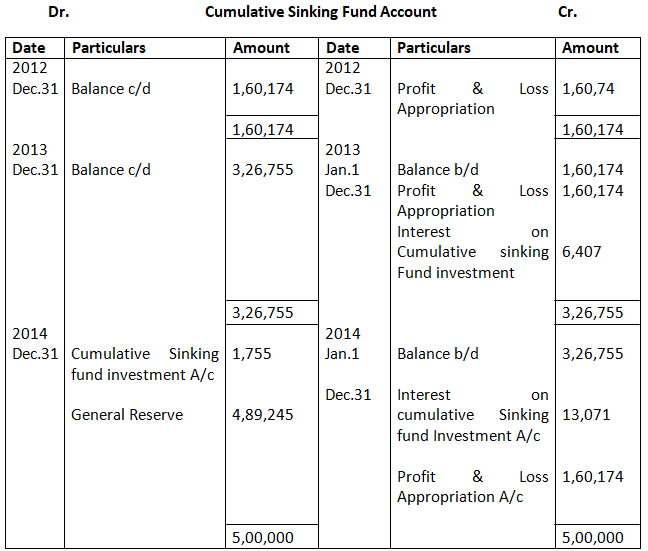

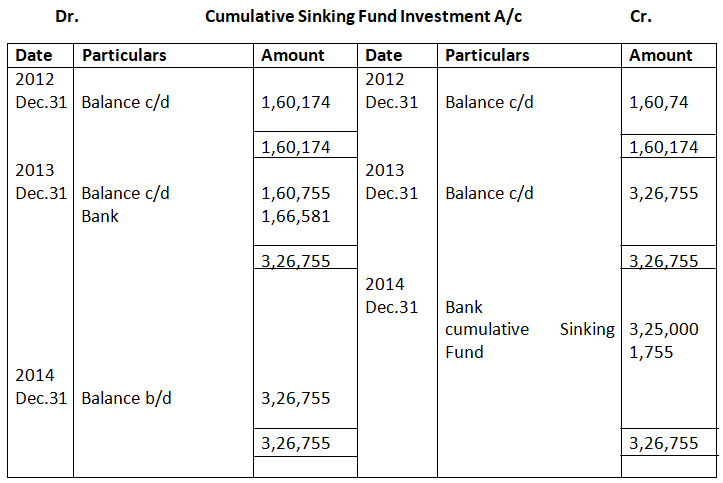

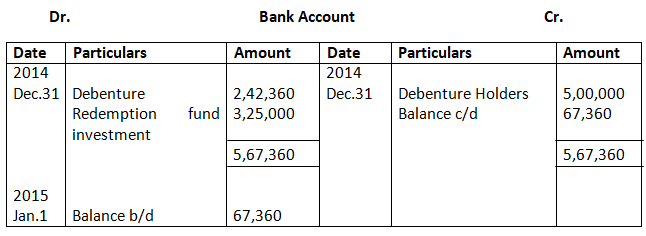

21. On January 01, 2012, X. Ltd issued 5,000, 8% Debentures of Rs.100 each repayable at par at the end of three years. It has been decided to set up a cumulative sinking fund for the purpose of their redemption. The investments are expected to realize 4% net. The Sinking fund Table shows that Rs.0,320348 amounts to one rupee @ 4% per annum in three years. On December 31, 2000 the balance at bank was Rs.2,42,360 and the investments realize Rs.3,25,000. The debentures were paid off.

Solution:-

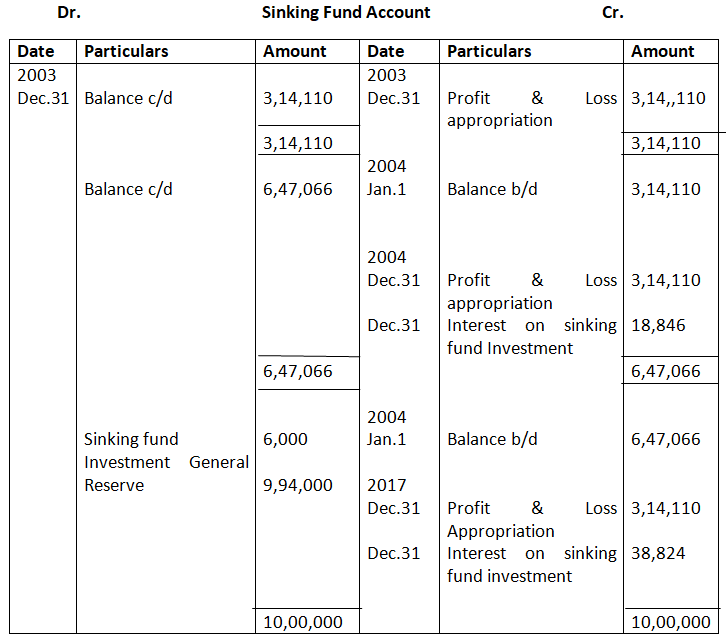

22. On January 01, 2003 a company issued 15% debentures of Rs.10,00,000 at par. The debentures were redeemable at par after three years on December 31, 2003. A sinking fund was set up to raise funds for redemption of debentures. The amount for the purpose was invested in 6% Government securities of Rs.100 each available at par. The sinking fund table shows that if investments earn 6% per annum, to get Rs.1 at the end of 3 years, one has to invest Rs.0.31411 every year together with interest that will be earned. On December 31, 2005, all the Government securities were sold at a total loss of Rs.6,000 and the debentures were redeemed at par. Prepare Debentures Account Sinking Fund Account, Sinking Fund Investment Account and Interest on Sinking Fund Investment Company closes its books of accounts every year on December 31.

Solution:-

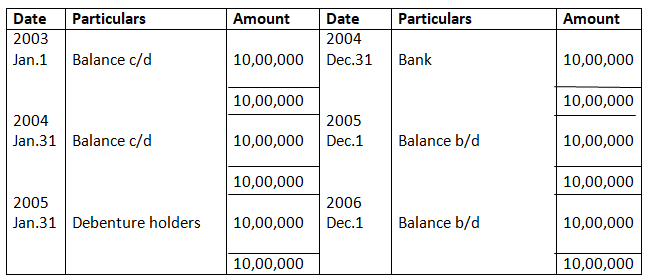

Dr. 15% Debenture Account Cr.

Ledger

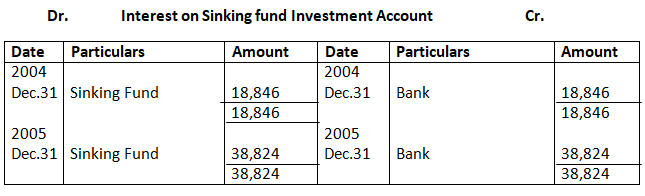

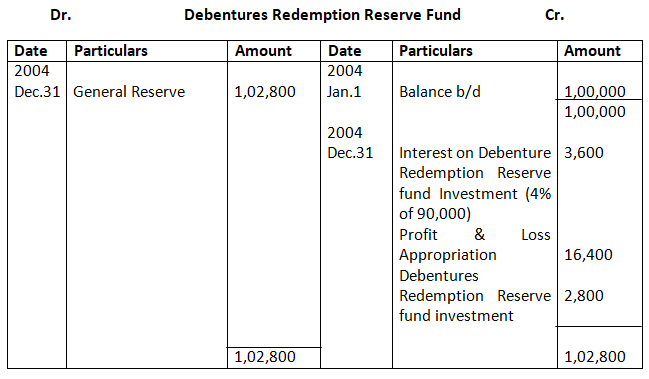

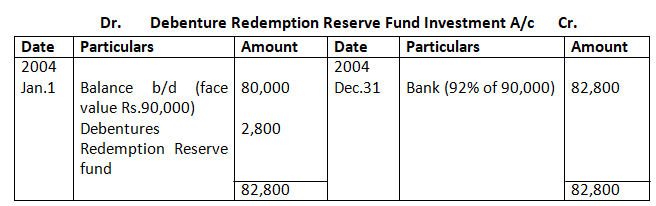

23. On January 01, 2004 the following balance appeared in the books of Z. Ltd.:

6% Debentures Rs.1,00,000

Debentures Redemption Reserve Fund Rs.80,000

D.R. Reserve Fund Investments Rs.80,000

The investments consisted of 4% Government securities of the face value of Rs.90,000.

The annual installment was Rs.16,400. On December 31, 2004, the balance at Bank was Rs.26,000 (after receipt of interest on D.R. Reserve fund investment). Investments were realized at 92% and the Debentures were redeemed. The interest for the year had already been paid. Show the ledger accounts redemption.

Solution:-

Dr. Book of Z. Ltd. 6% Debentures account Cr.

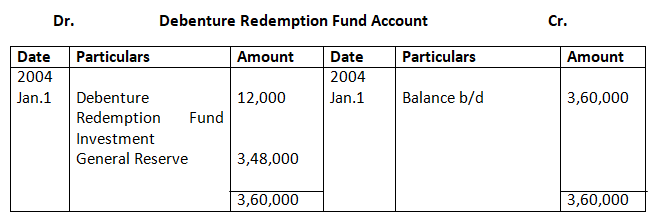

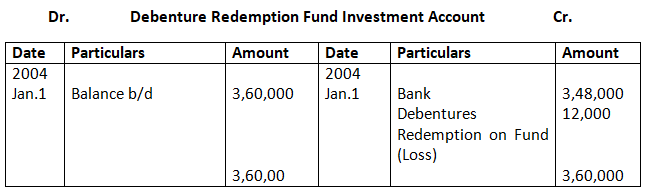

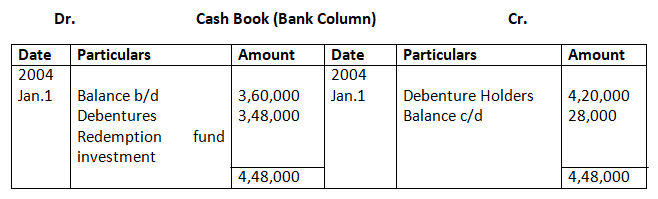

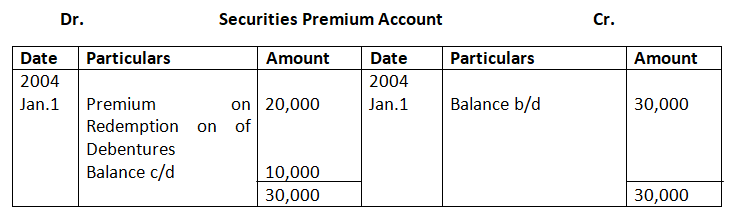

24. The following balances appeared in the books of A. Ltd. On January 01, 2004

12% Debentures Rs.4,00,000

Debentures Redemption Fund Rs.3,60,000

Debentures Redemption fund investment Rs.3,60,000

Securities Premium Rs.30,000

Bank Balance Rs.1,00,000

On January 01, 2004, the company redeemed all the debentures at 105 per cent out of funds raised by selling all the investments at Rs.3,48,000. Prepare the necessary ledger accounts.

Solution:-

Dr. Books of A. Ltd. 12% Debenture Account Cr.

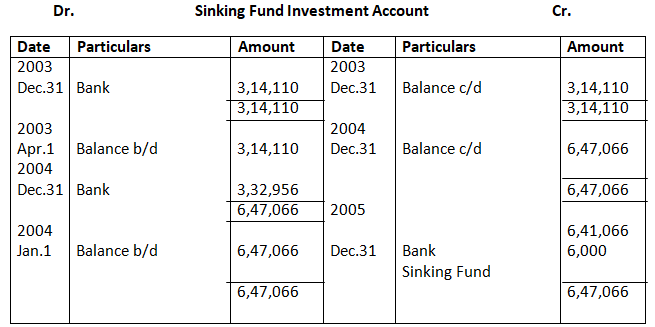

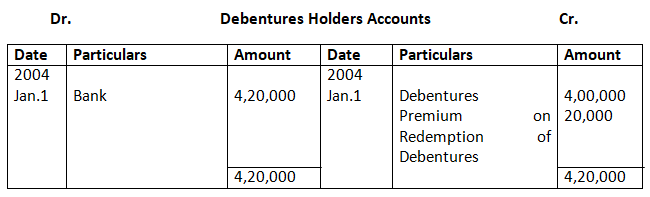

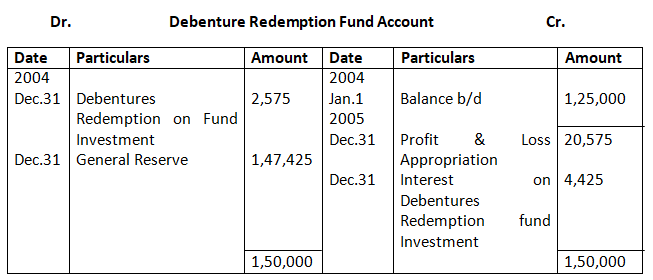

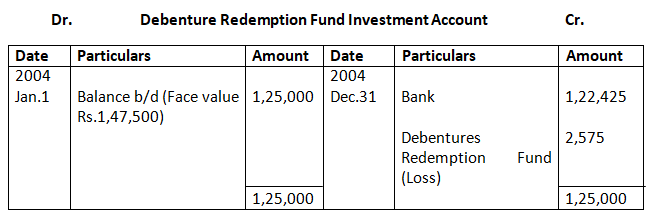

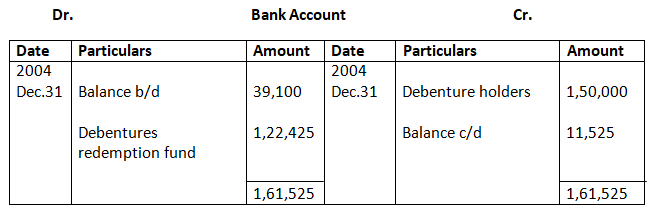

25. The following balances appeared in the books of Z. Ltd. On January 01, 2004

12% Debentures Rs.1,50,000

Debentures Redemption Fund Rs1,25,000

Debentures Redemption fund investment Rs.1,25,000

(Represented by Rs.1,47,500, 3% Govt. Securities Rs.1,25,000

The annual installment added to the fund is Rs.20,575. On December 31, 2004, the bank balance after the receipt of interest on the investment was Rs.39,100. On that date, all the investments were sold at 83 per cent and the debentures were duly redeemed. Show the necessary ledger accounts for the year 2004.

Solution:-

Books of Z. Ltd.

Dr. 12% Debentures Account Journal Cr.

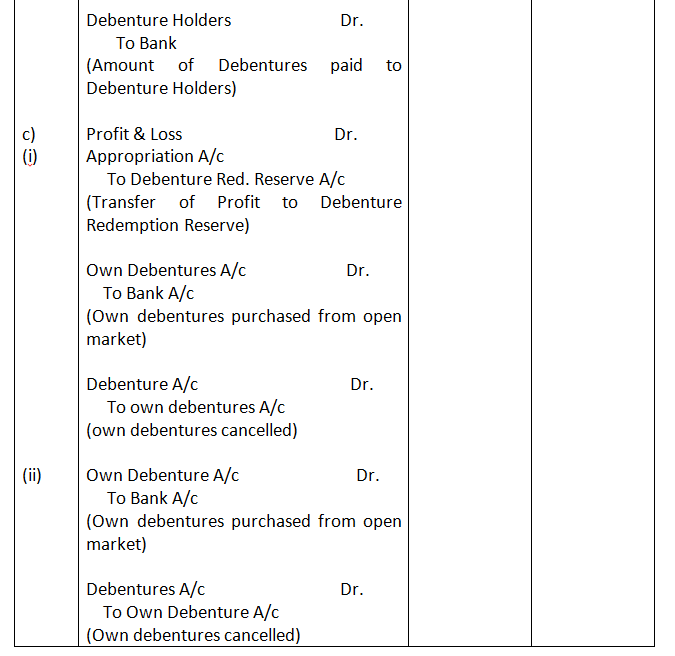

26. What entires for the redemption of debentures will be done when; a) debentures are redeemed by annual drawings out of profits; b) debentures are redeemed by drawing a lot out of capital; and c) debentures are redeemed by purchasing them in the open market when sinking fund for the redemption of debentures is not maintained- i) when out of profit, and ii) when out of capital?

Solution:-

27. A. Ltd. Company issued Rs.5,00,000 Debenture at a discount of 5% repayable at par by annual drawings of Rs.1,00,000. Make the necessary ledger accounts in the books of the company for the first year.

Solution:-

Books of A. Ltd.

Dr. Debenture Account Cr.

28. X. Ltd issued 5,000, 15% debentures of Rs.100 each on January 01, 2004 at a discount of 10%, redeemable at a premium of 10% in equal annual drawings in 4 years out of capital. Give journal entries both at the time of issue and redemption of debentures. . (Ignore the treatment of loss on issue of debentures and interest.)

Solution:-

Books of X. Ltd.

Journal

29. Z. Ltd issued 2,000, 14% debentures of Rs.100 each on January 01, 2005 at a discount of 10%, redeemable at a premium of 10% in equal annual drawings in 4 years out of profits. Give journal entries both at the time of issue and redemption of debentures. (Ignore the treatment of loss on issue of debentures and interest.)

Solution:-

Books of Z Ltd.

Journal

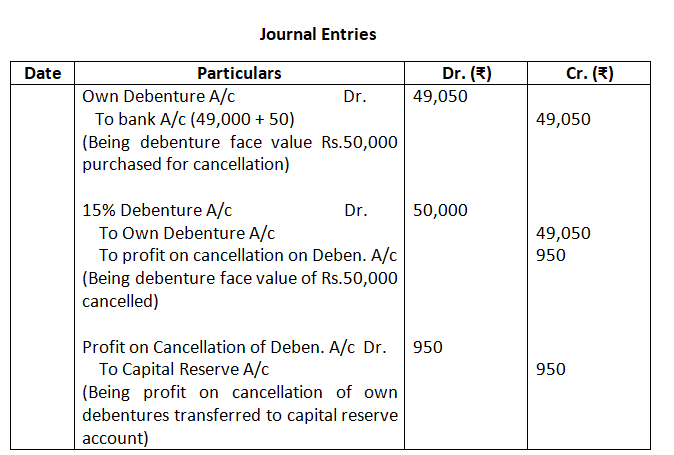

30. A. Ltd purchased for cancellation of the face value of RS.2,00,000 from the open market for immediate cancellation at Rs.92. Pass the journal entries.

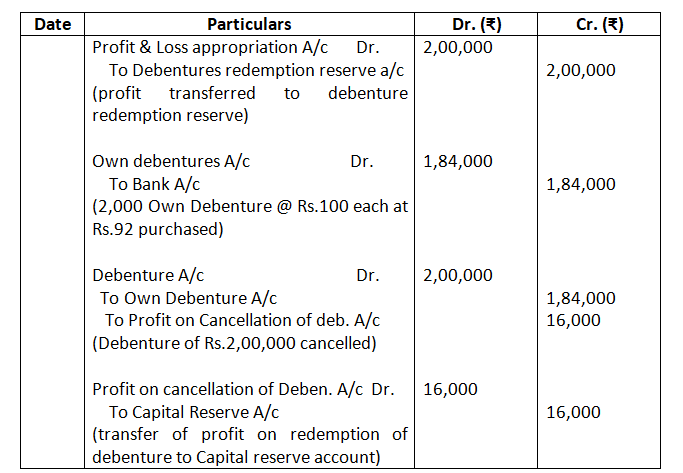

Solution:-

In the books of A. Ltd.

31. A. Ltd purchased for cancellation Rs.50,000 of its 15% debentures at Rs.98. The expenses of purchase amounted to Rs.50. On January 01, 2002, X. Ltd issued 40,000, 9% debentures of Rs.100 each at Rs.95. The terms of issue provided that, beginning with 1999, Rs.2,00,000 debentures should be redeemed either by drawings at par or by purchases in the open market every year. The expenses of issue amounted to Rs.12,000 which were written-off in 2002. The company also wrote off Rs.40,000 every year from Discount on Debentures Account. At the end of 2004, debentures to be redeemed were repaid by drawings. During 2005, the company purchased for cancellation 2,000 debentures at the market price of Rs.98 on December 31, the expenses being Rs.400. Interest on debentures is payable at the end of every calendar year. Pass the journal entries in the books of the company to record these transactions.

Solution:-

Working Note:

Number of Debenture purchased = 50,000 / 100 = 500

Profit on purchase = (100 – 98) x 500 = 1000

Less: expenses of purchase = 50

Profit on cancellation = 950

32. A. Ltd redeemed 8,000, 12% debentures of Rs.100 each which were issued at a discount of 5%, by converting them into equity shares of Rs.10 each at par.

Solution:-

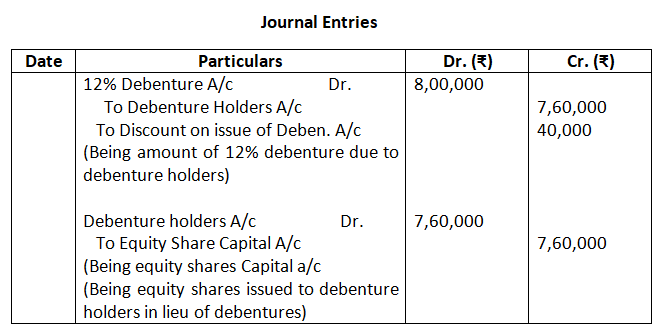

33. Y. Ltd redeemed 4,800, 12% debentures of Rs.100 each which were issued at par, at 110% by converting them into equity shares of Rs.10 each issued at a discount of 4%. Journalise.

Solution:-

Working Note

Number of shares to be issued = Amount due to debenture holders/Agreed price of share

= 7,60,000/10

= 76,000 Shares

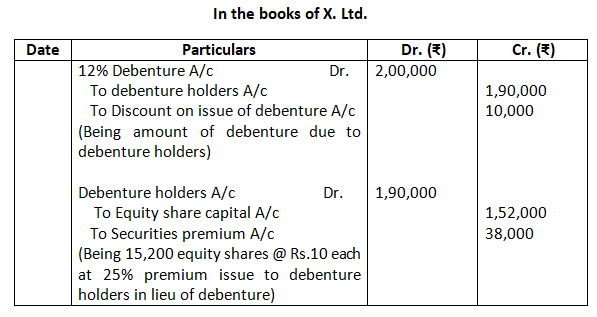

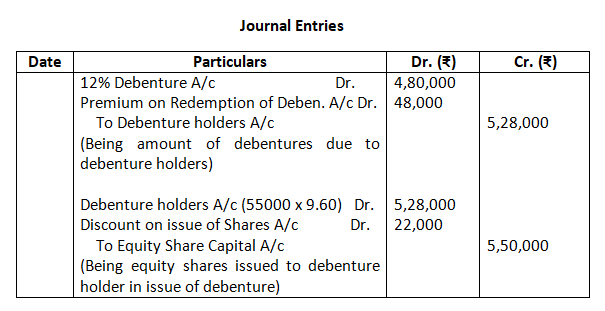

34. Z. Ltd redeemed 2,000, 12% debentures of Rs.100 each which were issued at a discount of 5%, by converting them into equity shares of Rs.10 each issued at a premium of 25%. Journalise.

Solution:-

Working Note:

Amount due to debenture holders = 4,800 x 110 = Rs.5,28,000

Number of shares to be issued = amount due to debenture holders / Agreed Price of Share

= 5,28,000 / 9.60 = 55,000 shares

35. X. Ltd redeemed 1,000, 12% debentures of Rs.50 each by converting them into 15% New Debentures of Rs.100 each. Journalise.

Solution:-