Source Documents:-

Source documents are the original records of business transactions. They are important because they prove, firs, that a transaction occurred, and they also serve as evidence of the details of that transaction should there ever be a discrepancy or dispute.

Most common source documents:-

- Cash Memo – Cash Memo is prepared by the seller when goods are sold against cash. It has details of goods sold, quantity, rate of each item and the total amount received, besides the date of transaction and other terms and conditions, if any. It is an evidence for the purchaser for, goods purchased against cash, and for the seller, it is an evidence of sales for case

Cash Memo

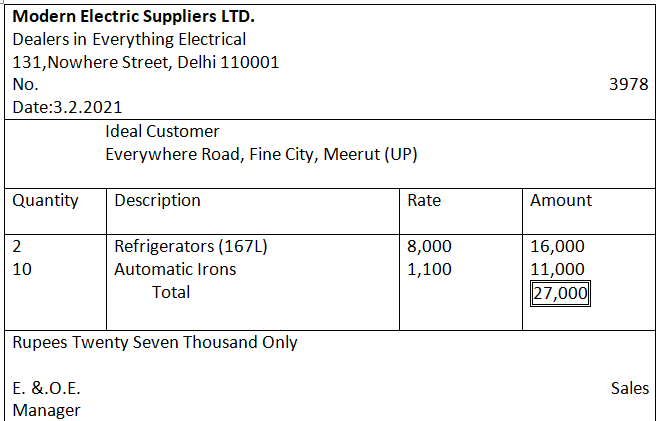

2. Invoice or Bill – An invoice or Bill is prepared by the seller when the goods are sold on credit. It has details of the party to whom goods are sold, goods sold and the total sale amount. The original copy of the sales invoice is sent to the purchaser and a duplicate copy is retained as an evidence of the sales for recording it in the books of account and for future reference.

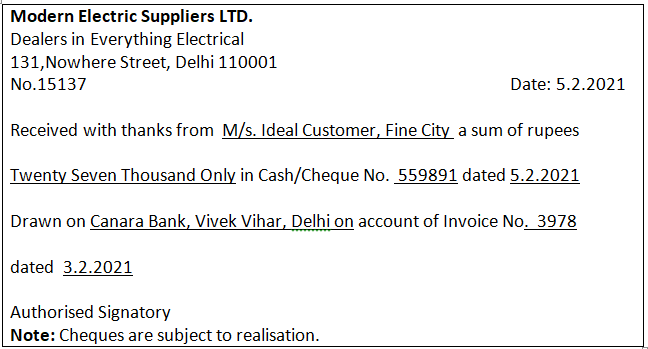

3. Receipt – When cash or cheque is received from a customer, a receipt for the amount received is issued. The receipt is prepared in duplicate. The original copy is given to the party making the payment and the duplicate is kept for record. It has details of date, amount, and name of the party and the nature of the payment.

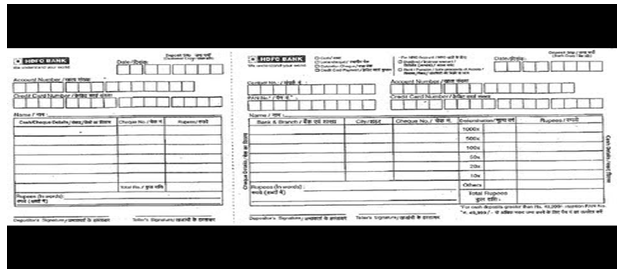

4. Pay-in-Slip – It is a source document used for depositing cash or cheques into bank. Pay-in-Slip is a form available from a bank. It has a counterfoil which is retained by the depositor. Now-a-days, banks place a box in which cheques along with the filled pay-in-slips can be dropped. In such cases, counterfoils are not signed.

5. Cheque – Cheque is a document in writing, drawn upon the bank which the account is held and is payable on or after the due date. The bank supplies the cheque forms. The name of the party to whom payment is to be made is written after the words ‘Pay To’. Then the amount is written – both in words and figures. A cheque is dated and signed by the drawer.

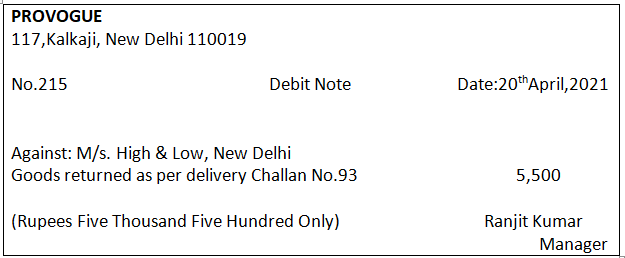

6. Debit Note – A debit Note is a document, bill or statement sent to the person to whom goods are returned. This statement informs that the supplier’s account is debited to the extent of the value of goods returned. It contains the description and details of goods returned, name of the party to whom goods are returned and the net value of the goods so returned with reason for return.

Debit Note

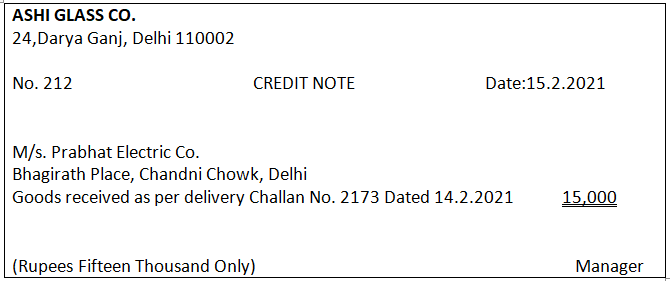

7. Credit Note – A Credit Note is prepared by the seller and sent to the buyer when goods are returned indicating that the buyer’s account is credited in respect of goods returned. Credit note is a statement prepared by a trader who receives back the goods sold from his customer. It contains details such as the description of goods returned by the buyer, quantity returned, and also their value.

Credit Note

Voucher:-

Voucher is a document evidencing a business transaction. It flows from the above definition that when a transaction is entered into evidence to that effect is also established. Such evidences are Source Documents, On the basis of Source Documents, a voucher detailing the accounts that are debited and credited is prepared.

Types of Vouchers:-

Vouchers may be categorised into:

- Source Vouchers or Source Documents or Supporting Vouchers – Source Vouchers or Source Documents or Supporting Vouchers are documents which come into existence when a transaction is entered into.

2. Accounting Vouchers – An Accountant has with him source or supporting vouchers for cash payments, cash receipts, invoices for credit purchases and sales. Yet, before recording in the books of account, these source vouchers are analysed to determine which account or accounts are to be debited and credited. The decision is recorded on a document termed ‘Accounting Voucher’. Thus, we can say that an ‘Accounting Voucher’ is a written document containing an analysis of business transactions for accounting and recording purposes, prepared by the Accountant on the basis of supporting vouchers and signed by another authorised person.

Types of Accounting Vouchers:-

Accounting Vouchers are of two types,

- Cash Vouchers – Cash voucher is the voucher prepared at the time of receipt or payment of cash and includes receipt and payment through cheques.

Cash Vouchers can be two types namely

- Credit Vouchers – Credit Vouchers are prepared when cash is received.

- Debit Vouchers – Debit Vouchers are prepared when payment is made.

2. Non- Cash Vouchers or Transfer Vouchers – Non-cash Vouchers are the Vouchers prepared for transactions not involving cash. Examples of these are Invoice or Bills, Debit and Credit Notes, etc. non-cash Vouchers are prepared for the transaction of credit sales, credit purchases, goods returned (both inwards and outwards), rectifying the errors, etc.

Compound Voucher:-

Voucher which records a transaction that entails multiple debits/credits and one credit/debit is called compound voucher

Compound Voucher may be:

- Debit Voucher

- Credit Voucher.

A Voucher showing a transaction that contains multiple debits but one credit is called Debit Voucher. A voucher showing a transaction that contains multiple credits but one debit is called Credit Voucher.

Accounting Equation

Accounting Equation is based on the Dual Aspect Concept of accounting. It means every transaction has dual aspect or two aspects – debit and credit. It holds that for every debit there is a credit of equal amount. The accounting equation, also known as the basic accounting equation or balance sheet equation is a statement that a company’s total asset is the sum of its liability and its shareholder’s equity. It ensures that the balance sheet is balanced.

We can express it mathematically as follows:

Liabilities = Assets – Capital

Or

Assets = Liabilities + Capital

Or

Capital = Assets – Liabilities

The above relationship called accounting equation

Effect of Transactions on Accounting Equation:-

A transaction may affect either both sides of the equation by the same amount or one side of the equation only, by both increasing and decreasing it by equal amounts.

- Those transactions that affect two items of the accounting equation or Balance Sheet.

Transaction affecting opposite sides are:

- Increase in asset, Increase in Liability – Transaction such as credit purchases increase asset (stock) and also increase liability (creditors). Similarly, Loan from bank increases asset (cash or bank) and also increases liability (Bank Loan)

- Decrease in Liability, Decrease in asset – Transaction of payment to a creditor decreases liability (creditor) and also reduces asset (cash or bank).

- Increase in Asset, Increase in Owner’s Capital – Introduction of capital by the proprietor increases asset (cash or bank) and also liability (owner’s capital0.

- Decrease in Owner’s Capital, Decrease in Asset – Drawings by the proprietor decrease liability (owner’s capital) and also asset (cash or bank).

Transaction affecting same side but in opposite direction are:

- Increase in asset, Decrease in another Asset – Transaction such as cash purchases or receipt from debtors increase one asset (goods and cash or bank, respectively) and decrease another asset (cash or bank and debtors).

- Decrease in Liability, Increase in Another Liability – Settlement of Creditor by issue of bill of exchange decreases a liability (creditor) and increases another liability (bill of exchange).

Transactions affecting More Than Two Items – Some transaction affect more than two items of the accounting equation or a balance sheet. For example, when a sale is made in cash for 30,000, it is made at cost (25,000) plus profit (5,000). Cost of goods (25,000) reduces asset (stock of goods): cash increases by 30,000 and the owner’s capital increases by the profit (5,000). It should be noted that profit increases the owner’s capital and loss decreases it.

Prepare Accounting Equation:-

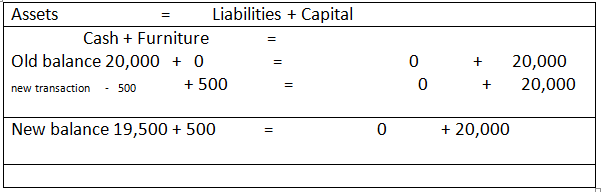

- Honey start business 20,000 as capital

2. Purchase Furniture in Cash 500

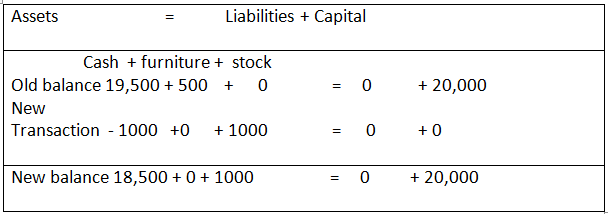

3. Purchase Goods in Cash 1000

Question Show Accounting Equation on the basis of the following transactions:

1.Gurman started business with cash 1,00,000.

2 Purchased goods in cash 50,000.

3 Purchased furniture from M/s Samrat Furnitures 20,000 on credit.

4.Sold goods costing 25,000 for 35,000 against cash.

5 M/s Samrat Furnitures was paid in cash.

Question Prepare Accounting Equation on the basis of the following:

- Started business with cash 70,000.

- Credit purchases of goods 18,000.

- Payment made to creditors in full settlement 17,500.

- Purchase of machinery for cash 20,000.

Effect of Adjustment Transactions on Accounting Equation:-

- Outstanding Expenses are those expenses which have been incurred but have not been paid. It is deducted from Capital.

- Prepaid Expenses are those expenses which have been paid in advance, i.e., they are not yet due but paid. It is deducted from cash.

- Accrued Income is that income which has been earned but not received during the current accounting period. It is add in capital.

- Unearned Income or Income Received in advance is that income which has been received but not earned during the current accounting period. It is add in cash.

Example:-

- Increase in one asset, decrease in another asset.

- Increase in asset, increase in liability.

- Increase in asset, increase in owner’s capital.

- Decrease in asset, decrease in liability.

- Decrease in asset, decrease in owner’s capital.

- Decrease in liabilities, increase in owner’s capital.

- Increase in one liability, decrease in another liability.

- Increase in liabilities, decrease in owner’s capital.

Solution:-

- Purchase of furniture for cash – Increase in furniture and decrease in cash.

- Purchase of Furniture on credit – Increase in furniture and increase in liability.

- Capital introduced by proprietor – Increase in cash and increase in capital.

- Payment to creditors – Decrease in cash and decrease in creditors.

- Cash withdrawn by proprietor – Decrease in cash and decrease in capital.

- Conversion of partner’s loan into capital – Increase in capital and decrease in loan.

- Bills payable accepted – Increase in bills payable and decrease in creditors.

- Outstanding expenses provided – Increase in creditors for outstanding expenses and decrease in capital.

Question

From the following information, calculate total assets of the business: Capital 4,00,000; Creditors 3,00,000; Revenue earned during the period 7,50,000;Expenses incurred during the period 2,00,000; Value of unsold stock 2,00,000.

Question

X started a business on 1st April, 2023 with a capital of 50.000 and a loan of 25000 taken from Y. During the year, he had introduced additional capital of 25,000 and had withdrawn 15,000 for personal use. On 31st March, 2024 his assets were 1,50.000. Find his capital as on 31st March, 2024 and profit made or loss incurred during the year ended 31st March, 2024.

Debit and Credit

Transactions are recorded in the books of account on the basis of evidences, i.e., source documents, such as invoices for purchases, invoices for sales, debit and credit notes, etc. Rules of debit and credit are applied to each transaction and recorded in the book of original entry, i.e., Journal.

The transactions recorded in the books of account are transferred to the specific account maintained in the Ledger.

At this stage, it is appropriate to define and understand the term ‘account’. Account is a record of transactions under a particular head. It records not only the amount of transactions but also their effect and direction.

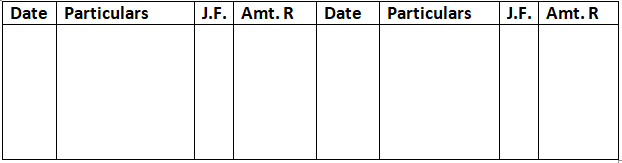

An Account is divided into two parts, i.e., debit and credit. It is usually in a “T” from and the commonly used layout of an account is as follows:

Name of the Account, e.g., salary Account

Dr. Cr.

What is Debit and Credit

Debit refers to the left side of an account and credit refers to the right side of an account. In the abbreviated form Dr. Stands for debit and Cr. stands for credit. An item recorded on the debit side of an account is said to be debited to the account. An item recorded on the credit side of an account is said to be credited to the account.

Both debit and credit may represent either increase or decrease depending upon the nature of an account. The rules of debit and credit depend on the nature of account.

Rules of Debit and Credit:-

Under Double Entry System of accounting each transaction has two aspects. One aspect is debit, i.e., receiving or incoming aspect. Another aspect is credit, i.e., giving or outgoing aspect. Debit and Credit aspects of a transaction form the basis of Double Entry System.

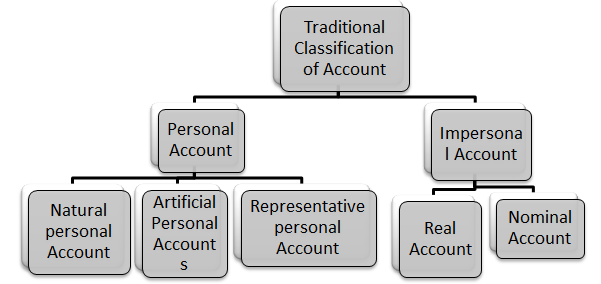

Classification of Accounts:-

Account can be classified in two ways:

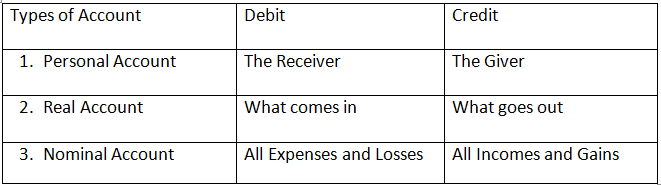

- Traditional Classification

- Modern Classification A. Traditional Classification – Under this classification, account are classified into two groups as shown below:

Personal Accounts – Accounts which relate to persons, i.e., individuals, firms, companies, debtors or creditors, etc., are Personal Account. Examples of Personal Accounts are the account of Ram & Co., a customer (debtor), or the account of Jhaveri & Co., a supplier of goods (Creditor), Capital Account and Drawings Account of the proprietor. The main purpose of preparing a Personal Account is to determine the balance due to or due from persons or organisation.

Personal Account can be classified into three categories:

- Natural Personal Accounts – the term ‘Natural Personal’ means persons who are creations of God. Therefore, these will include accounts in individual name. For example, ram account, asha account, etc.

- Artificial Personal Account – These accounts include accounts of corporate bodies or institutions which are recognised as persons in business dealings. For example, the accounts of a limited company, the account of a club or a cooperative society, etc.

- Representative Personal Accounts – These are accounts which represent a certain person or a group of persons. For example, if rent is due to the landlord, an outstanding Rent Account will be opened in the books. The outstanding Rent Account represents the amount of rent payable to the landlord.

Rule of Debit and Credit –

Debit the receiver, Credit the giver.

Impersonal Accounts – Accounts which are not personal such as Machinery Account, Cash Account, Rent Account, etc., are termed as Impersonal Accounts. These can be further sub-divided into two accounts:

- Real Accounts – Real Account are the Accounts which relate to tangible or intangible assets of the firm (excluding debtors). Examples of tangible assets are: Land, Building, Investments, Plant and Machinery, Stock or cash in hand. Example of intangible assets is: Goodwill, Patents and Trademarks

Rule of Debit and Credit –

Debit what comes in, credit what goes out.

II. Nominal Account – Accounts which relate to expenses, Losses, Gains, Revenue, etc., are termed as Nominal Accounts. These are Salary Account, Purchases Account, Interest Paid Account, Sales Account and Commission Received Account.

Rule of Debit and Credit – Debit all expenses and losses, Credit all income and Gains.

Rules of Debit and Credit (Traditional Classification)

Examples:-

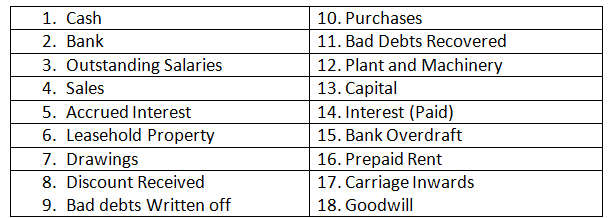

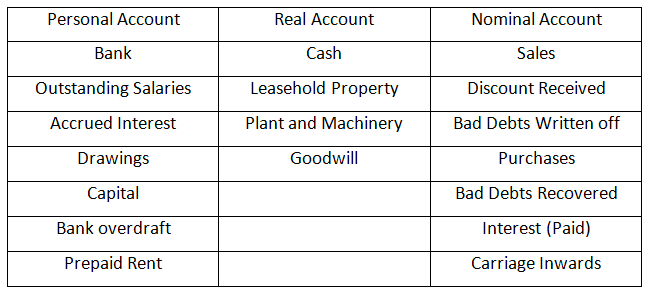

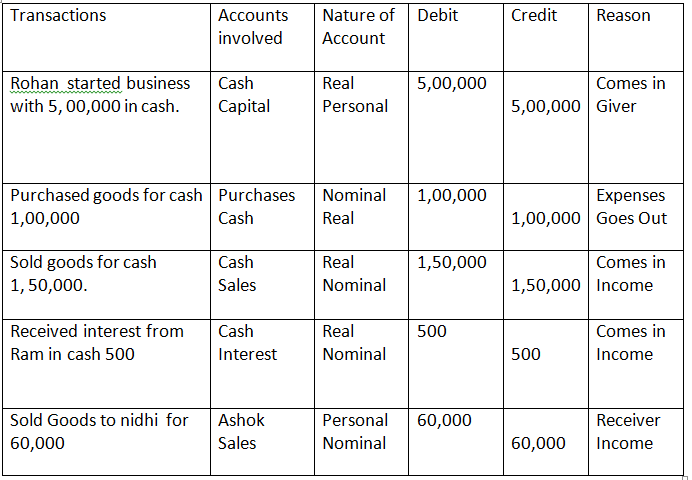

- Classify the following accounts into Personal, Real and Nominal Accounts:

Solution:

II. From the following transaction, state the nature of accounts and state which account will be debited and which account will be credited:

- Rohan started business with cash 5,00,000

- Purchased goods for cash 1,00,000

- Sold goods for cash 1,50,000

- Received interest from Ram in cash 500

- Sold goods to nidhi 60,000

Solution: Analysis of Transactions

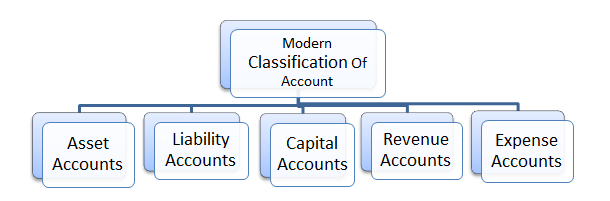

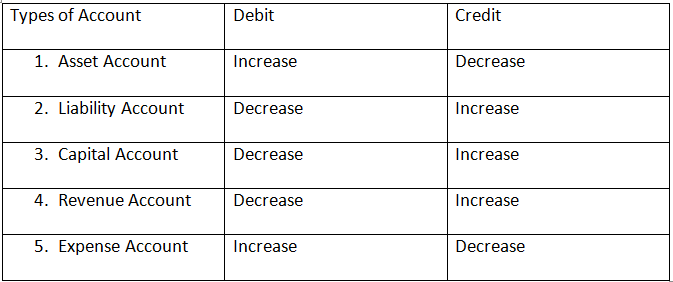

B. Modern Classification – Under this Classification, all the accounts are Classified into the following five Categories:

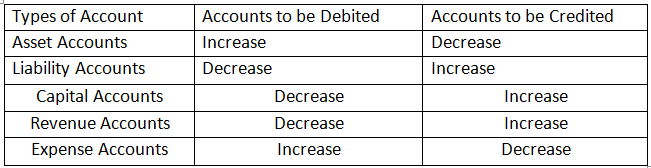

- Asset Accounts – Asset accounts are those accounts which relate to the economic resources of an enterprise such as Land and Building, Plant and Machinery, Furniture, Patents, Inventory, Bank and Cash, etc.

Rule of Debit and Credit – Debit the increases and Credit the Decreases.

2. Liability Accounts – Liability Account Are accounts of Lenders, Creditors for goods, outstanding expenses, etc.

Rule of Debit and Credit- Debit the decreases and Credit the increases.

3. Capital Accounts – These are the accounts of Proprietors/Partners who have invested amount in the business. It includes both Capital and Drawings Account.

Rule of Debit and Credit – Debit the decreases and credit the increases.

4. Revenue Accounts – These are accounts of incomes and gains. Examples are: Sales, Discount received, Interest received, commission received, bad debts recovered, etc.

Rule of Debit and Credit – Debit the decreases and Credit the increases.

5. Expense Accounts – These are the accounts of expenses or Losses incurred in carrying the business. Examples are: Purchases, Wages, Salaries, and Depreciation, Discount allowed and rent, etc.

Rule of Debit and Credit – Debit the increases and credit the decreases.

Rules for Debit and Credit (Modern Classification)

Example:-

- On which side will the increase in following accounts be recorded? Also, mention the nature of the account on the basis of Modern Classification of Accounts:

Solution –

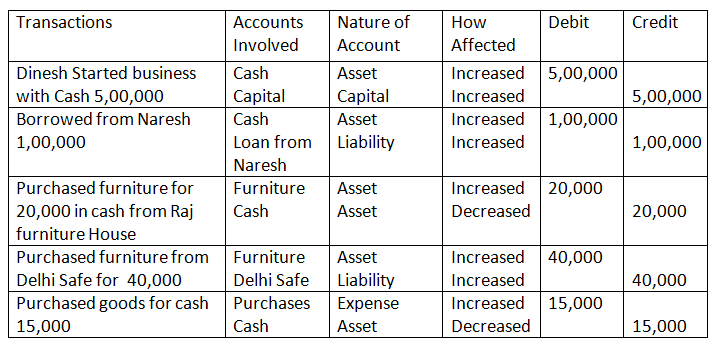

2. Analyse the following Transactions, state the nature of accounts and state which account will be debited and which account will be credited on the basis of modern Classification of Account;

- Dinesh Started business with cash 5,00,000

- Borrowed from Naresh 1,00,000

- Purchased furniture for cash from Raj Furniture House 20,000

- Purchased furniture from Delhi Safe 40,000

- Purchased goods for cash 15,000

Solution: – Analysis of Transaction

Books of Original Entry

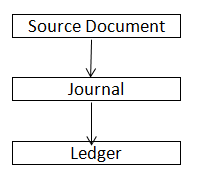

In the preceding pages, you learnt about debits and credit and observed how transactions affect accounts. This process of analysing transactions and recording their effects directly in the accounts is helpful as a learning exercise. However, real accounting systems do not record transactions directly in the accounts. The book in which the transaction is recorded for the first time is called journal or book of original entry.

Journal

Journal is a book of primary entry or a book of original entry in which transactions are first recorded in a chronological order from the accounting vouchers that are prepared on the basis of source documents, i.e., cash memo, invoices, purchase bills, etc. The transactions can be recorded in one journal.

Terms of Journal

- Book of Original Entry – Journal is called a Book Of Original Entry (also called Book of Primary Entry) because a transaction is first recorded or written in this book and thereafter transferred, i.e., posted in the Ledger Accounts.

- Journal Entry – An entry recorded in the Journal is called a Journal Entry.

- Journalising – The process of recording a transaction in a Journal is known as Journalising.

- Posting – The transfer of Journal entry to Ledger Accounts is called Posting.

Rules of Debit and Credit:-

Based on Traditional Classification of Accounts:-

Based on Modern Classification of Accounts:-

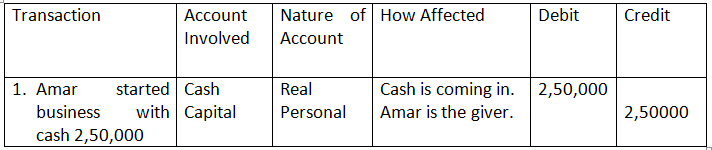

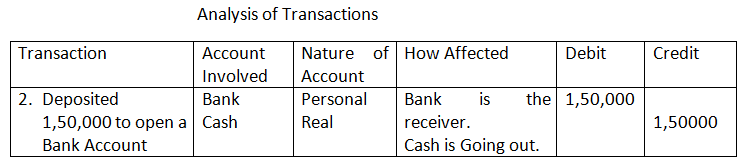

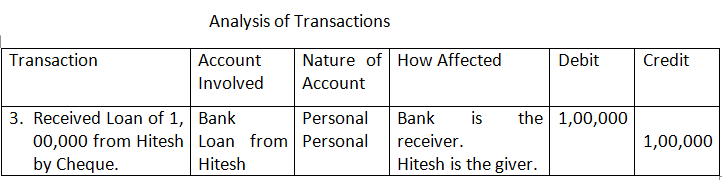

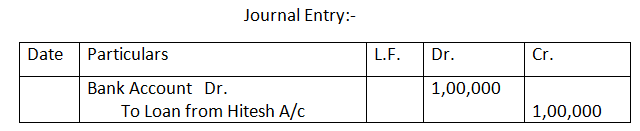

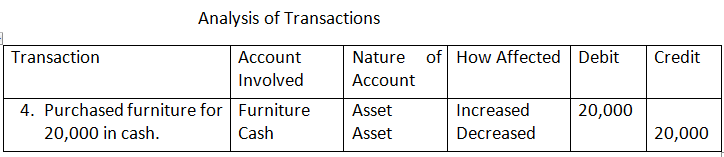

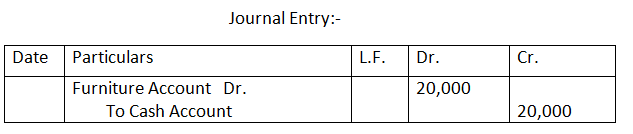

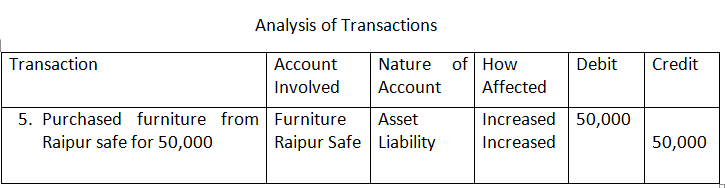

Example

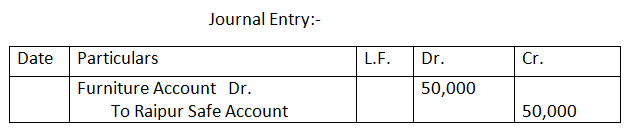

- Analyse the following transactions, state the nature of accounts and the account that will be debited and credit as per the Traditional Classification of Account

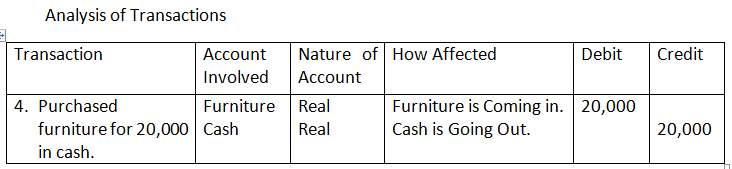

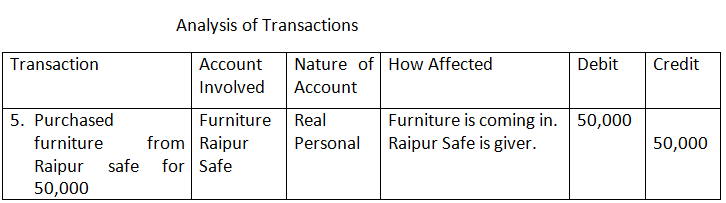

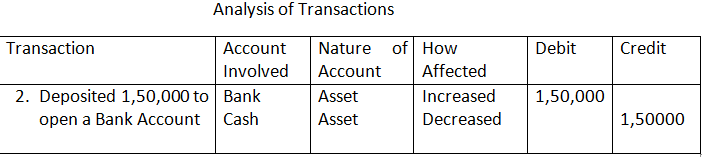

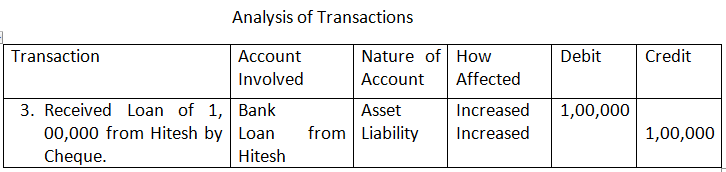

- Amar started business introducing capital of 2, 50,000 in cash.

- Opened a Bank Account by depositing 1, 50,000 in cash.

- Received Loan of 1, 00,000 from Hitesh by Cheque.

- Purchased furniture for 20,000 in cash from Sunny Furniture House.

- Purchased furniture from Raipur safe for 50,000.

Solution: – Traditional Classification of Account:-

Analysis of Transactions

Morden Classification of Account:-

Analysis of Transactions

Journal Entries are two types:

- Simple (Journal) Entry

- Compound (Journal) Entry.

- Simple (Journal) Entry – Simple (Journal) entry is a Journal entry in which one account is debited and another account is credited with an equal amount. For example, purchase of goods of 5,000 in cash.

Journal entry is:

Purchases Account …Dr. 5,000

To Cash Account 5,000

2. Compound (Journal) Entry – Compound (Journal) entry is a Journal entry in which one or more accounts is debited and/or one or more accounts are credited or vice versa. For example, sale of goods to Ankit for 6,000. 4,000 are received in cash and balance to be received later.

Entry for the transaction is a compound entry as follows:

Cash/Bank Account …Dr. 4,000

Ankit Account …Dr. 2,000

To Sales Account 6,000

Discount

Discount is an allowance given by the seller of goods and can be of three types:

- Trade Discount

- Cash Discount

- Rebate

- Trade Discount – Trade Discount is a discount allowed by the seller at the time when goods are purchased in large quantity. It is normally allowed by the seller to the purchaser who sells the goods further. For example, Amit sells goods to Vikas of 10,000 allowing him trade discount of 20%. The invoice will be prepared as follows:

List Price 1, 00,000

Less: Trade Discount (20%) 20,000

Sale Value 80,000

Amit will pass following Journal entry in his books of Account:

Vikas …Dr 80,000

To Sales A/c 80,000

(Goods sold to Vikas)

Vikas will pass following Journal entry in his books of account:

Purchases A/c …Dr 80,000

To Amit 80,000

(Goods purchased from Amit)

2. Cash Discount – Cash Discount is allowed by the seller of goods to encourage prompt or early payment. Thus, it is allowed if the payment is received within the specified time. For example, Param sells goods of 100,000 allowing 10% Trade Discount and 2% Cash Discount. Cash Discount will be calculated as follows:

List Price 1, 00,000

Less: Trade Discount (10%) 10,000

Sale Value 90,000

Less: Cash Discount (2% of 90,000) 1,800

Amount Received 88,200

Cash discount is allowed on receipt of amount in cash or by cheque. It is an Expense for the business allowing it and gain for the business receiving it.

- When Cash Discount is Received:

Creditors A/c ….Dr

To Cash or Bank A/c

To Discount Received A/c

II. When Cash Discount is allowed:

Cash or Bank A/c ….Dr

Discount Allowed A/c ….Dr

To Debtors A/c

Rebate

Rebate is also a discount allowed by the seller of goods but for the reasons other than for which trade discount and cash discount are allowed. For example, rebate may be allowed for poor quality of goods, goods sold being not as per specification, etc. it is different from Trade Discount as trade discount is allowed in higher volume of goods purchased by the purchaser and rebate is allowed for reasons other than higher volume of goods purchased. Goods sold by Amit to Vikas were of poor quality and therefore, Amit allowed him rebate of 5,000.

Amit Will pass following entry for rebate allowed:

Rebate Allowed A/c …Dr 5,000

To Vikas 5,000

(Rebate allowed on goods sold to vikas)

Rebate allowed will be deducted by the seller from Sale Value in the

Trading Account

Vikas will pass following Journal entry for rebate received:

Amit …Dr 5,000

To Rebate Received A/c 5,000

(Rebate received from Amit)

Rebate received will be deducted by the purchase from Purchases in the Trading Account.

Accounting Entries of Some Specific Transaction:-

- Bad Debts:-

If an amount, say of credit sales, is not recoverable or is partially recoverable then the amount not recoverable is Bad Debt. It being a loss for the business is debited to the Bad Debts Account and credited to the personal account of the debtors. The Journal entries passed are:

- When the total due amount is not recoverable:

Bad debts A/c …Dr

To Debtors (Personal) A/c

II. When a part of the debt is recorded:

When a debtor pays a part of due amount in settlement, the amount not realised is a loss to the business. The Journal entry passed is:

Cash or Bank A/c ….Dr

Bad Debts A/c …Dr

To Debtor (Personal) A/c

2. Bad Debts Recovered :-

A debtor whose account was earlier written off as ‘Bad Debts’ may pay the amount partly or fully, The amount received is a gain to the business because the Debtor’s Account was earlier written off as a bad debt, i.e., loss. Amount received against bad debts earlier written off is recorded (Credited) in an account titled Bad Debts Recovered Account and not to the personal account of the debtor from whom the amount is received.

The entry of Bad Debts Recovered is:

Cash or Bank A/c ……Dr.

To Bad Debts Recovered A/c

Bad Debts Recovered Account is shown in the Credit side of Profit and Loss Account.

3. Banking Transactions – Businesses normally make and receive payments through a Bank Account. Payments by Cheque, cheques received, withdrawal of cash from bank, deposits into bank, bank charges and interest charged on overdraft by bank, etc., are examples of banking transactions.

Cash deposit in bank

Bank a/c Dr. Dr. is receiver

To cash a/c cr. What goes out

Cash withdraw

Cash a/c Dr. Dr. what comes in

To bank a/c cr. The giver

4. Goods Given As Charity or Goods Donated – The amount of purchases is reduced with the purchase cost of goods given as Charity or Donation. Purchases are reduced because the goods are not sold. The Journal entry passed is:

Charity/Donation A/c ….Dr

To Purchases A/c

4. Goods Given As Samples – Goods are given as samples to encourage sales. It is not a sale but part of the advertisement or sales promotion expense, hence, it is debited to the Advertisement (Sales Promotion) Expenses Account or Samples Account and Deducted from, i.e., Credited to purchases. The Journal entry is:

Advertisement (Sales Promotion) Expenses/Samples A/c ….Dr

To Purchases A/c

6. Loss of Stock by Theft or Fire – In both the cases, it is loss of goods and loss to business. The following entry is passed:

Loss of Stock by Theft or Fire A/c ….Dr

To Purchases A/c

7. Drawings – Drawings means amount or goods withdrawn by the proprietor for personal use.

- Drawings in cash – Cash withdrawn by proprietor or amount paid for personal expenses of the proprietor (say for Life Insurance Premium, Income Tax, purchase of refrigerator etc.) is debited to Drawings Account since it is withdrawn for personal use and not for business.

The Journal entry passed is:

Drawings A/c …Dr

To Cash A/c

II. Drawings of Goods – Goods taken by the proprietor for personal use is debited to Drawings Account and credited to purchases Account at its purchase cost since it is not a sale.

The Journal entry passed is:

Drawings A/c …Dr

To purchases A/c

8. Purchase and Sale of Fixed Assets – Fixed assets such as Machinery, Furniture and Fixtures, etc., are purchased to increase the earning capacity of the business and not for resale like goods. Following entries are passed to record purchase and sale of fixed assets:

On Purchase of Fixed Asset:

Fixed Asset A/c

To Cash/Bank A/c

To Supplier A/c

On Sale of Fixed Asset:

Cash/Bank A/c …Dr

Purchaser A/c …Dr

Loss on Sale of Fixed Asset A/c …Dr

To Fixed Asset A/c

To Gain (Profit) On Sale of Fixed Asset A/c

Adjustment Entries:-

- Closing Stock or Inventory – Closing Stock or Inventory means stock of unsold goods at the end of accounting period

- Outstanding Expenses – Outstanding expenses are the expenses that are of the current year bur have not been paid till the year end.

- Prepaid or Unexpired Expenses – Expenses paid in advance, i.e., expenses that are of next year but paid in the current year are called prepaid expenses.

- Accrued Income or Income Earned but not Received – Income which has been earned but is not received or has not become due is called Accrued income.

- Income Received in Advance or Unearned Income – Income received but not earned, i.e., against which sale of goods or services is yet to be made, is called income received in advance.

- Depreciation – Due to use of fixed assets, value of these assets decreases every year. This fall in value is called Depreciation.

- Interest on Capital – Funds invested by a proprietor in the business is ‘Capital’.

- Interest on Drawings – Amount withdrawn by the proprietor from business for personal use against profit for the year is ‘Drawings’.

Introduction of Ledger

Meaning

Ledger is the collection of different accounts of assets, liabilities, capital, revenue and expenses. When transaction are recorded in the journal (Book of original Entry), these are transferred or posted to their respective accounts in Ledger. These are also called Book of Secondary or Final Entry. A ledger is a book which contain in a summarised and classified form, a permanent record of all transaction.

Features of Ledger

- Ledger is a master record of all accounts of the business.

- It is prepared from Journal.

- Ledger Accounts show the current balance in all accounts.

- Trial Balance and Final Accounts are prepared from Ledger Accounts.

- Ledger Accounts summarise the effect of transactions upon assets, liabilities, capital, incomes and expenditures.

Utilities of Ledger:-

- Provides Complete Information of a Particular Account – Complete information relating to a particular account is available at one place in the Ledger.

- Information of income and Expenses – In Ledger, a separate account is maintained for each income and expense. The amount of total income and total expenses are Known from the Ledger Account.

- Preparation of Trial Balance – Ledger helps in preparing Trail Balance which ensures arithmetical accuracy of the transactions recorded in books of account.

- Helpful in Preparing Final Accounts – After preparing Trial Balance, Final Accounts are prepared to know the profitability and financial position of the business.

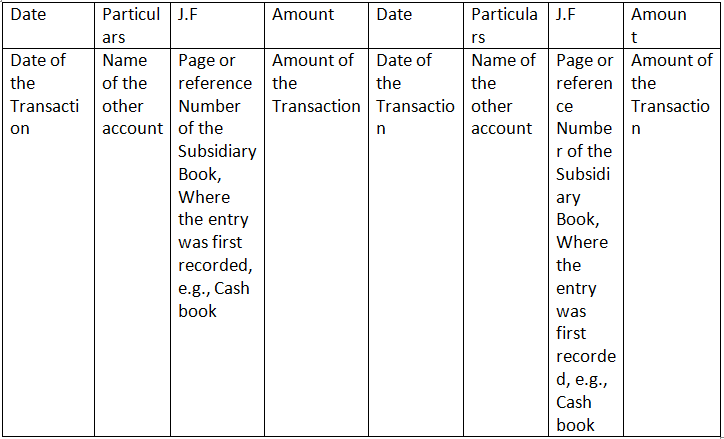

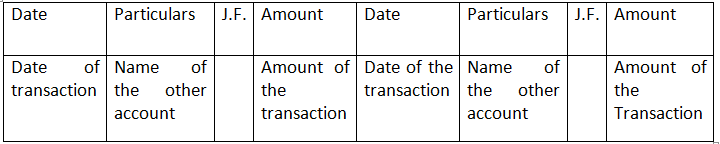

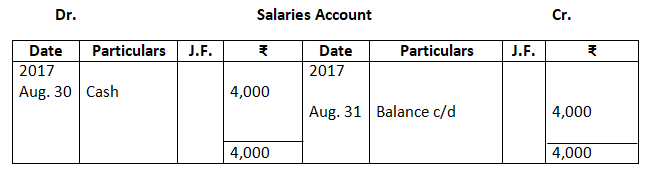

Format of Ledger Account

The format of Ledger account has been explained in an earlier Chapter. For convenience it is being repeated here.

Dr NAME OF THE ACCOUNT, e.g., WAGES ACCOUNT Cr

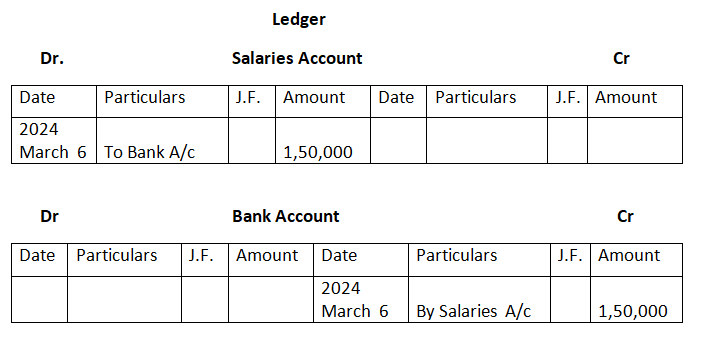

Posting the Entries:-

The process of transferring the transaction written in the Journal to a Ledger is called Posting. In other words, the process of transferring of debits and credits from the Journal to the Ledger Accounts is called Posting. Posting is necessary as it summarises all transactions relating to the account at one place and also shows how transactions have changed the account balances.

Posting of Journal Entry:-

Consider the following entry to illustrate the above process:

Journal

Posting Of Compound Entry:-

In a simple entry, only one account is debited and one account is credited. When in a Journal entry, two or more accounts are debited and one or more accounts are credited or vice versa, the entry is known as Compound Journal Entry.

Let us understand the posting of compound entry with the help of the following example:

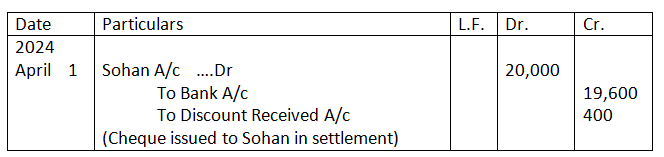

Example: – On 1st April, 2021, Rohan paid to Sohan by cheque 19,600 in settlement of 20,000. Pass journal entry and post it in Ledger Accounts of Rohan

Journal

Ledger Accounts of Rohan will be as follows

Dr. Sohan Account Cr

Posting of Opening Entry:-

The balances of assets and liabilities in the Trail Balance are transferred in the Balance Sheet as at the end of the accounting year. These assets and liabilities are brought forward in the beginning of the next year. The entry passed to record such closing balances of the previous year in the current year is called Opening Entry.

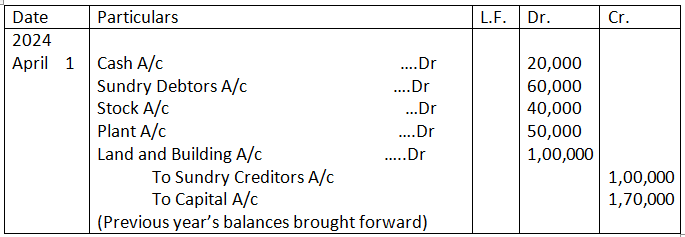

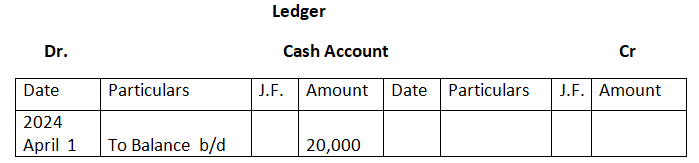

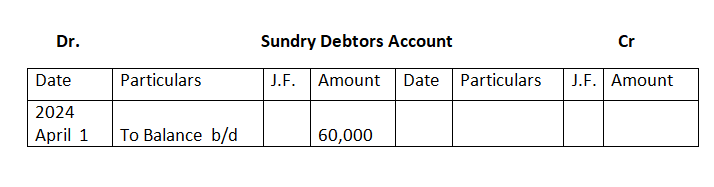

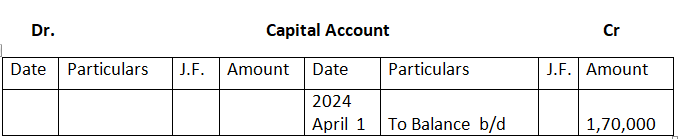

Example: – Pass the opening Entry on 1st April, 2021 on the basis of the following information taken from the books of Akash. Also, post the opening entry.

Cash in Hand 20,000

Sundry Debtors 60,000

Stock of Goods 40,000

Plant 50,000

Land and Building 1, 00,000

Sundry Creditors 1, 00,000

Solution – In the book of Akash

Journal

Short Answers

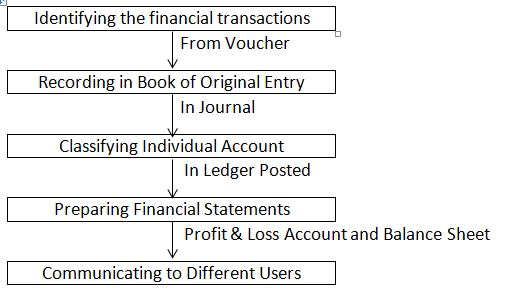

- State the tree fundamental steps in the accounting process.

Answer: The fundamental steps in the accounting process are diagrammatically presented below.

2. Why is the evidence provided by source documents important to accounting?

Answer: The evidence provided by the source document is important in the following manners:

- It provides evidence that a transaction has actually occurred.

- It provides important and relevant information about date, amount, parties involved and other details of a particular transaction.

- It acts as a proof in the court of law.

- It helps in verifying transactions during the auditing process.

3. Should a transaction be first recorded in a journal or ledger? Why?

Answer: A transaction should be recorded first in a journal because journal provides complete details of a transaction in one entry. Further, a journal forms the basis for posting the transactions into their respective accounts into ledger. Transactions are recorded in journal in chronological order, i.e. in the order of occurrence with the help of source documents. Journal is also known as ‘book of original entry’, because with the help of source document, transactions are originally recorded in books. The process of recording the transactions in journal and then in ledger is presented in the below given flow chart.

4. Are debits or credits listed first in journal entries? Are debits or credits indented?

Answer: As per the rule of double entry system, there are two columns of ‘Amount’ in the journal format namely ‘Debit Amount’ and ‘Credit Amount’. The way of recording in a journal is quite different from normal recording. Journal entry is recorded in journal format in which the ‘Debit Amount’ column is listed before the ‘Credit Amount’ column.

Credits are indented. Indentation is leaving a space before writing any word. Journal entry has its own jargon. While journalising, in the ‘Particulars’ column of journal format, debited account is written first and credited account is in the next line leaving some space, which is indentation.

5. Why are some accounting systems called double accounting systems?

Answer: Some accounting systems are called double accounting systems because under this system there are two aspects of every transaction, i.e., every transaction has dual effect. Every transaction affects two accounts simultaneously, that is represented by debiting one account and crediting the other account. It is based on the fact that if there is receiver, there should be a giver.

6. Give a specimen of an account.

Answer:-

Dr. ______ Account Cr.

7. Why are the rules of debit and credit same for both liability and capital?

Answer:

Every business acquires funds from internal as well as from external sources. According to the business entity concept, the amount borrowed from the external sources together with the internal sources like, capital invested by the proprietor, is termed as liability to the business. Business entity concept treats business and business owner separately. Capital of the owner is treated as liability to the business because the business has to repay the amount of capital to the owner, in case of closure of the business. As liability incurred is credited, in the same way, fresh capital introduced and net profit increases the owner’s capital, and so, capital is credited. On the other hand, if liability is paid, it reduces liability, and so, it is debited. Similarly, drawings from capital and net loss reduce the capital, and so, capital is debited. Thus the rules of debit and credit are same for both liability and capital.

8. What is the purpose of posting J.F numbers that are entered in the journal at the time entries are posted to the Accounts.

Answer: J.F. number is the number that is entered in the ledger at the time of posting entries into their respective accounts. It helps in determining whether all transactions are properly posted in their accounts. It is recorded at the time of posting and not at the time of recording the transactions.

The purpose of entering J.F. number in the ledger is because of the below given benefits.

1. J.F. number helps in locating the entries of accounts in the journal book. In other words, J.F number helps to locate the position of the related journal entry and subsidiary book in the journal book.

2. J.F. number in accounts ensures that recording in the books of original entry has been posted or not.

9. What entry (debit or credit) would you make to : (a) increase revenue (b) decrease in expense, (c) record drawings (d) record the fresh capital introduced by the owner.

Answer:

1. Increase in revenue

Increase in revenue is credited as it increases the capital. Capital has credit balance and if capital increases, then it is credited.

2. Decrease in expense

Decrease in expense is credited as all expenses have debit balance. If expense decreases, then it is credited.

3. Record drawings

Capital has credit balance; if the capital increases, then it is credited. If capital decreases, then it is debited. Drawings are debited as they decrease the capital.

4. Record of fresh capital introduced by the owner- credit

Capital has credit balance, if capital increases, then it is credited. The introduction of fresh capital increases the balance of capital, and so, it is credited.

10. If a transaction has the effect of decreasing an asset, is the decrease recorded as a debit or as a credit? If the transaction has the effect of decreasing a liability, is the decrease recorded as a debit or as a credit?

Answer: If a transaction has a decreasing effect on an asset, then this decrease is recorded as credit. This is because, as all assets have debit balance and if assets decrease, then it is credited. For example, sale of furniture results in decrease in furniture (asset); so, the sale of furniture will be credited.

If a transaction has a decreasing effect on a liability, then this decrease is recorded as debit. This is because all liabilities have credit balance. If the liability increases, then it is credited and if the liability decreases, then it is debited. For example, payment to the creditors results in a decrease in the creditors (liability); so, the creditors account will be debited.

Long Answers

- Describe the events recorded in accounting systems and the importance of source documents in those systems?

Ans. It is beyond human capabilities to memorise each financial transaction and that is why, source documents have their own importance in accounting system.

They are considered as an evidence of transactions and can be presented in the court of law. Transactions supported by evidence can be verified. Source documents also ensure that transactions recorded in the books are free from personal biases.

A few events that are supported by source document are given below:

- Sale of goods worth Rs.200 on credit, supported by sales invoice/bill

- Purchase of goods worth Rs.500 on credit, supported by purchase invoice/bill

- Cash sales worth Rs.1,000, supported by cash memo Cash memo

- Cash purchase of goods worth Rs.400, supported by cash memo

- Goods worth Rs.100 returned by customer, supported by credit note

- Return of goods purchased on credit worth Rs.200, supported by debit note

- Payment worth Rs.1,200 through bank, supported by cheques

- Deposits into bank worth Rs.500, supported by pay-in slips.

Out of the above events, only those events that can be expressed in monetary terms, are recorded in the books of accounts.

Source document in accounting is important because of the below given reasons:

- It provides evidence that transaction has actually occurred.

- It provides information about the date, amount and parties involved and other details of a particular transactions.

- It acts as and evidence in the count of law.

- It helps in verifying the transaction during the auditing process.

2. Describe how debits and credits are used to analyse transaction.

Ans. Debit originated from the Italian word debito, which in turn is derived from the Latin word debeo, which means ‘owed to proprietor’ and credit comes from the Italian word credito, which is derived from the Latin word credo, which means belief, i.e., ‘owed by proprietor’.

According to the dual aspect concept, all the business transaction that are recorded in the books of account, have two aspects- debit and credit.

The dual aspect can be better understood by the help of an example; bought goods worth Rs.500 on cash.

This transaction affects two accounts with the same amount simultaneously.

As goods are brought in exchange of cash, so the cash balances in the business reduce by Rs.500, i.e. why the cash account is credited. Simultaneously, the amount of goods increases by Rs.500, so purchases account will be debited.

Debit and credit depend on the nature of accounts involved; such as assets, expenses, income, liablilities and capital.

There are five types of Accounts:

- Assets – these include all properties or legal rights owned by a firm for its operations, such as cash in hand, plant and machinery, bank, land, building, etc.

All assets have debit balance. If assets increase, they are debited and if assets decrease, they are credited.

For example, furniture purchased and payment made by cheque.

The journal entry is:

Furniture A/c Dr.

To Bank A/c

Here, furniture and bank balance, both are assets to the firm.

As furniture is purchased, so furniture account will increase, and will be debited.

On the other hand, payment of furniture is being made by cheque that reduces the bank balance of the business, so bank account will be credited.

- Expense – It is made to run business smoothly and to carry day to day business activites.

All expenses have debit balance.

If an expense is incurred, it must be debited.

For example, rent paid.

The journal entry is:

Rent A/c Dr.

To Cash A/c

Here, rent is an expense. All expenses have debit balance.

Hence, rent is debited. On the other hand, as rent is paid in cash that reduced the cash balances, so cash account is credited.

- Liability – Liability is an obligation of business.

Increase in liability is credited and decrease in liability is debited.

For example, loan taken from bank.

The journal entry is:

Bank A/c Dr.

To Bank Loan A/c

Here, loan from bank is a liability to the firm.

As all liabilities have credit balance, so loan from bank has been credited because it increases the liabilities.

- Income – Income means profit during an accounting period from any source. Income also means excess of revenue over its cost during an accounting period.Income has credit balance because it increases the balance of capital.

For example, Rent received from tenant.

The journal entry is:

Cash A/c Dr.

To Rent A/c

Here, rent is an income; hence, rent account has been credited and cash has been debited, as rent received increases the cash balances.

- Capital – Capital is the amount invested by the proprietor in the business. Capital has credit balance.

Increase in capital is credited and decrease in capital is debited

For example, additional capital introduced by owner.

The journal entry is:

Cash A/c Dr.

To Capital A/c

As additional capital is introduced, so the amount of capital will increase, i.e. why, capital account is credited.

On the other hand, as capital is introduced in from of cash, so the cash balance decrease, i.e. why, cash account is debited.

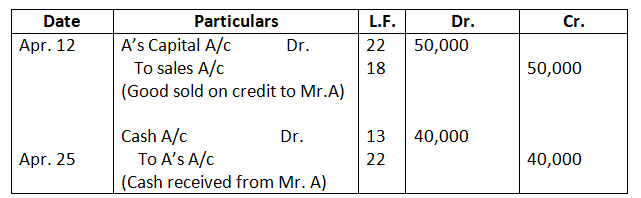

3. Describe how accounts are used to record information about the effects of transactions?

Answer:- Every transaction is recorded in the original book of entry (journal) in order of their occurrence; however, if we want to know that haw much we receive from our debtors or how much to pay to the creditors, it is not possible to determine at a single movement.

Hence, we prepare accounts to know the position of business activities in the meantime. There are some steps to record transactions in accounts; it can be easily understood with the help of an example.

Sold goods to Mr. A worth Rs.50,000 on 12th April and received payment Rs.40,000 on 25th April.

The following journal entries will be recorded:

Step 1 – Locate the account in ledger, i.e., Mr. A’s Account.

Step 2 – Enter the date of transaction in the date column of the debit side of Mr. A’s Account.

Step 3 – In the ‘Particulars’ column of the debit side of Mr. A’s Account, the name of corresponding account is to be written. i.e., ‘Sales’.

Step 4 – Enter the page number of the ledger in the journal Folio (J.F) column of Mr. A’s Account.

Step 5 – Enter the amount in the ‘Amount’ column.

Step 6 – Same steps are to be followed to post entries in the credit side of Mr. A’s Account.

Step 7 – After entering all the transactions for a particular period, balance the account by totalling both sides and write the difference in shorter side, as ‘Balance c/d’.

Step 8 – total of account is to be written on either sides.

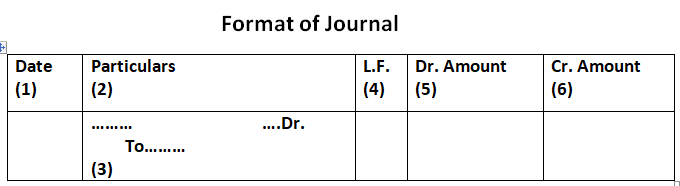

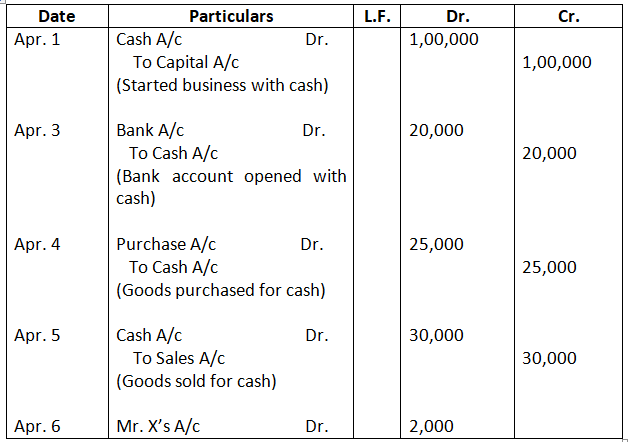

4. What is a journal? Give a specimen of journal showing at least five entires.

Answer :- Journal is derived from the French word Jour, means daily records. In this book, transactions are recorded in order of their occurrence, i.e., in chronological order from the source document. It is also termed as the book of original entry and each transaction is termed as journal entry.

Performa of Journal

In the books of _____

Date – Date of transaction is recorded in the order of their occurrence.

Particulars – Details of business transaction like, name of the parties involved and the name of related accounts, are recorded.

L.F. – Page number of ledger account when entry is posted.

Debit Amount – Amount of debit account is written.

Credit Amount – Amount of credit account is written.

Book of Mr. A

Journal

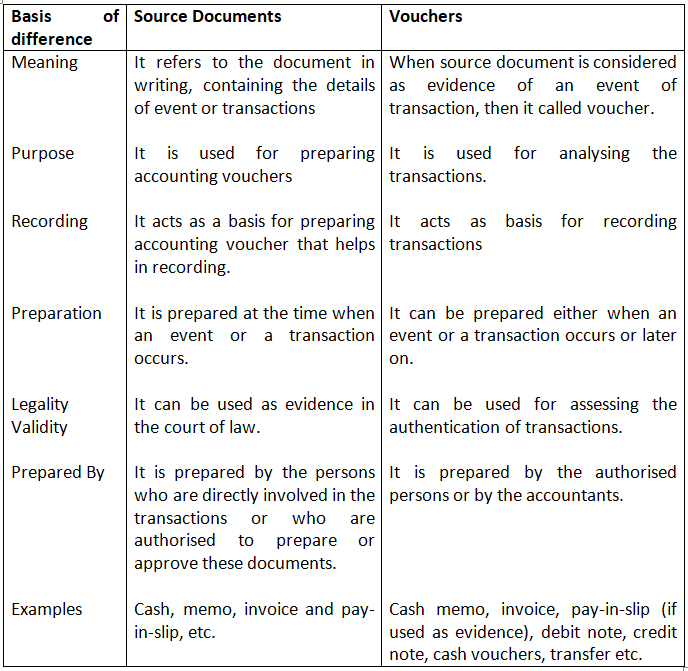

5. Differentiate between source documents and vouchers.

Answer:-

6. Accounting equation remains intact under all circumstances. Justify the statement with the help of an example.

Answer:- The double entry accounting system states that or every debit there is an equal amount of credit. Hence there is unlikely to be the equality of the total assets with the total claims of the business and the accounting equation will persist to be Assets = Liabilities + Capital,

Hence this equation will remain intact under all the circumstances.

The example for the same are as follows:

- Mr. A started a business with cash Rs.100,000

Assets = Liabilities + Capital

Cash increases by 1,00,000

1,00,000 = 0 + 1,00,000

b. Purchased goods on credit for Rs.30,000

Assets (Inventory) = 30,000

Creditors = 30,000

Assets = Liabilities + Capital

30,000 = 30,000 + 0

7. Explain the double entry mechanism with an illustrative example.

Answer:- As per the double entry system of accounting every transaction has two aspects debit and credit. Hence the double entry accounting system states that or every debit there is an equal amount of credit. Thus the ledger account always shows the debit on one side and the other side to abide by the dual aspect concept

The three golden rules of accounting must be known in passing an entry:

- Personal Account – Debit the receiver/Credit giver

- Real Account – Debit what comes in/Credit what goes out

- Nominal Accounts – Debit the expenses/Losses/Credit the income gain

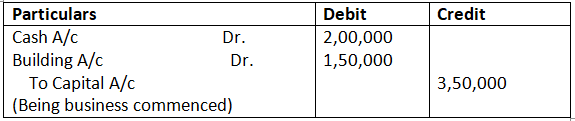

Illusstrative example: Mr. Shham commenced business with cash Rs.2,00,000 and building Rs.150,000.

Analysis: In the above transaction in-hand cash comes in Rs.2,00,000 and building comes in Rs.150,000.

On the other hand liability to be paid to the proprietor i.e. capital increase is Rs.350000.

Journal Entry in the books of Shyam

Numerical Questions

Analysis of Transactions

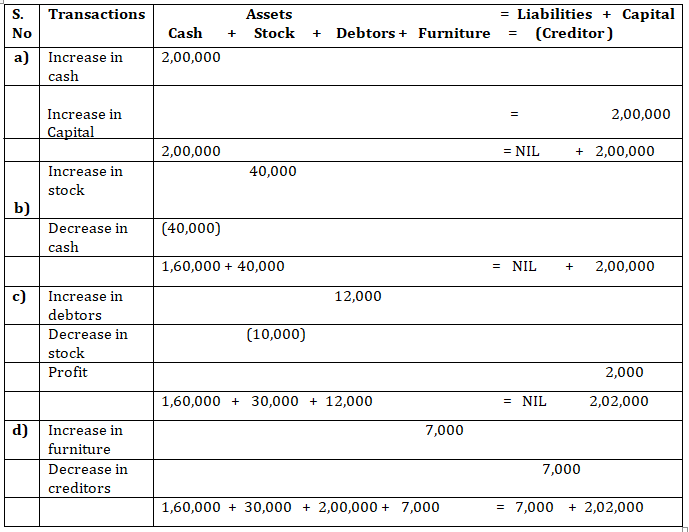

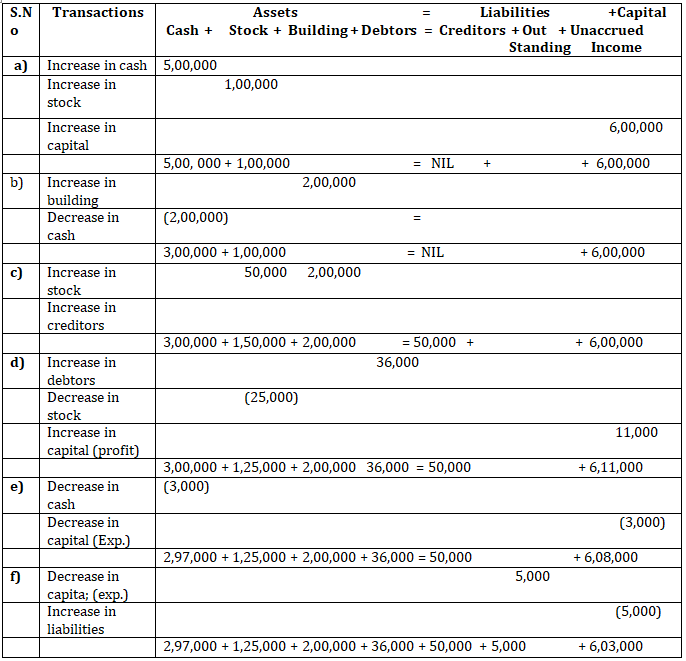

- Prepare accounting equation on the basis of the following :

- Harsha started business with Cash Rs.2,00,000.

- Purchased goods from Naman for Cash Rs.40,000.

- Sold goods to Bhanu costing Rs.10,000/- Rs.12,000.

- Bought furniture on credit Rs.7,000

Solution:-

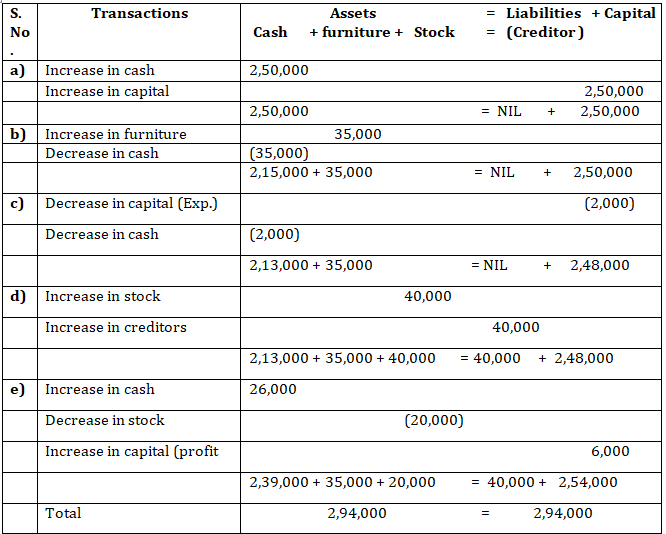

2. Prepare accounting equation from the following:

- Kunal started business with cash Rs.2,50,000.

- He purchased furniture for cash Rs.35,000.

- He paid commission Rs.2,000.

- He purchases goods on credit Rs.40,000.

- He sold goods (Costing Rs.20,000) for cash Rs.26,000.

Solution :-

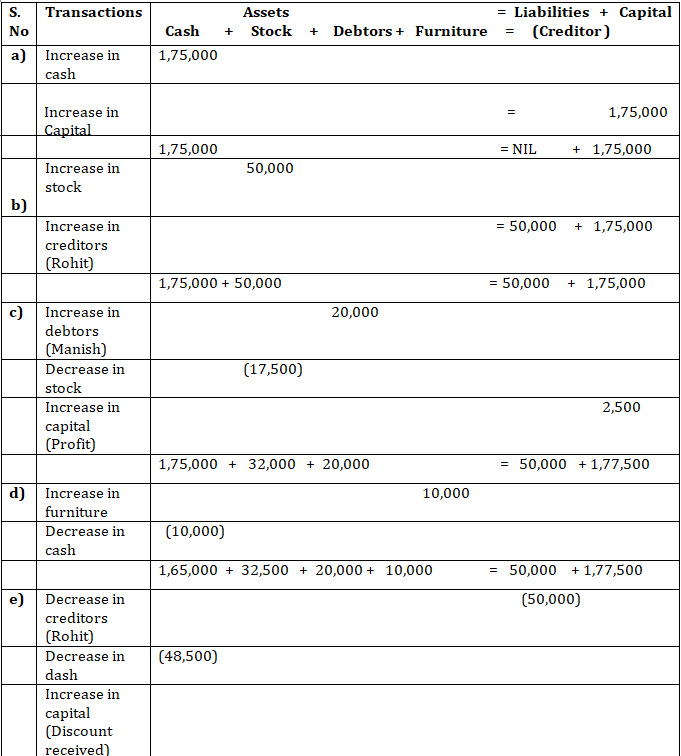

3. Mohit has the following transactions, prepare accounting equation:

Rs.

- Business started with cash 1,75,000

- Purchased goods from Rohit 50,000

- Sales goods on credit to Manish (Costing Rs.17,500) 20,000

- Purchased furniture for office use 10,000

- Cash paid to Rohit in full settlement 48,000

- Cash received from Manish 20,000

- Rent paid 1,000

- Cash withdrew for personal use 3,000

Solution:-

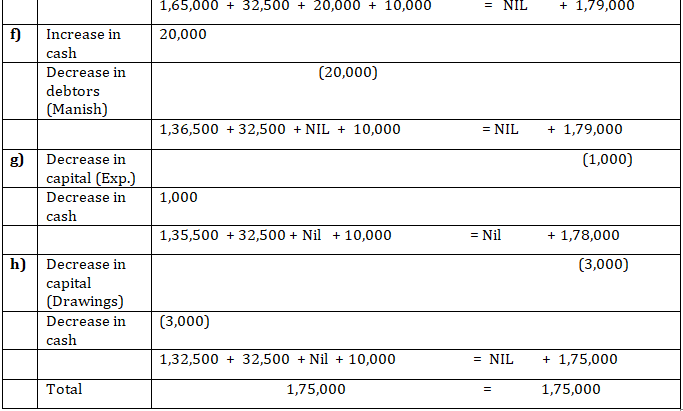

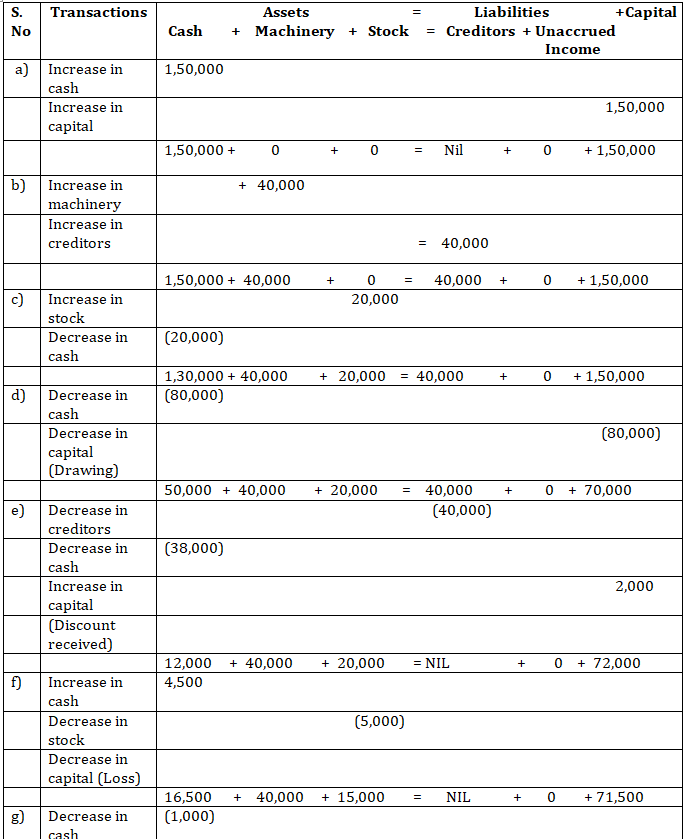

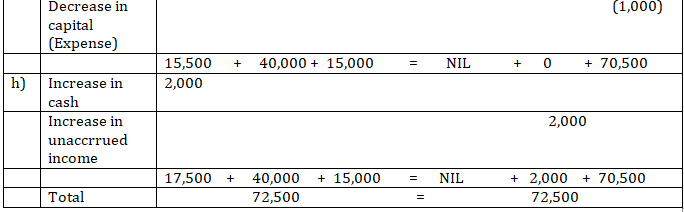

4. Rohit has the following transactions:

Rs.

- Commenced business with cash 1,50,000

- Purchased machinery on credit 40,000

- Purchased goods for cash 20,000

- Purchased car for personal use 80,000

- Paid to creditors in full settlement 38,000

- Sold goods for cash costing Rs.5,000 4,500

- Paid rent 1,000

- Commission received in advance 2,000

Prepare the Accounting Equation to show the effect of the above transactions on the assets, liabilities and capital.

Solution:-

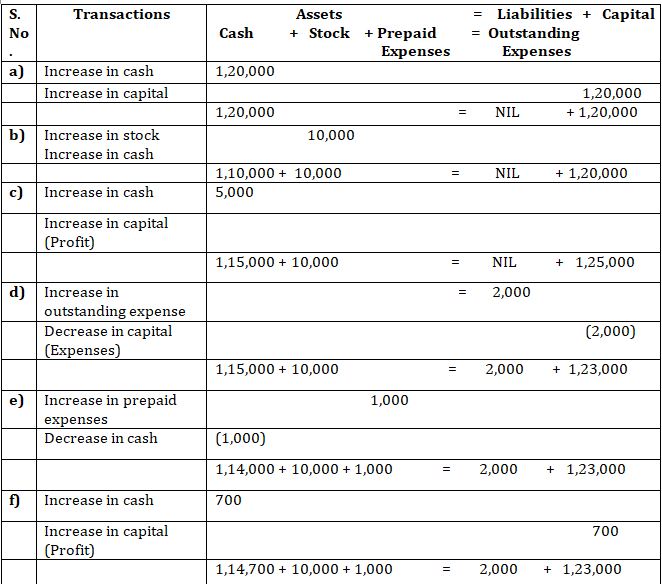

5. Use accounting equation to show the effect of the following transaction of M/s Royal Traders:

Rs.

- Started business with cash 1,20,000

- Purchased goods for cash 10,000

- Rent received 5,000

- Salary outstanding 2,000

- Prepaid Insurance 1,000

- Received interest 700

- Sold goods for cash (Costing Rs.5,000) 7,000

- Goods destroyed by fire 500

Solution:-

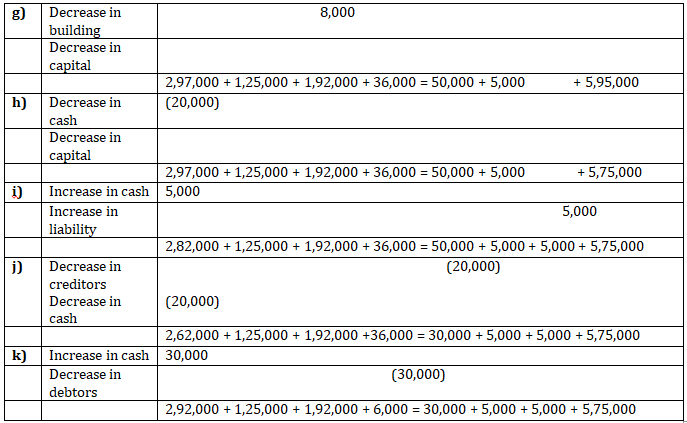

6. Show the accounting equation on the basis of the following transaction:

a. Udit started business with:

- Cash Rs.5,00,000

- Goods Rs.1,00,000

b. Purchased building for cash Rs.2,00,000

c. Purchased goods from Himani Rs.50,000

d. old goods to Ashu (Cost Rs.25,000) Rs.36,000

e. Paid insurance premium Rs.3,000

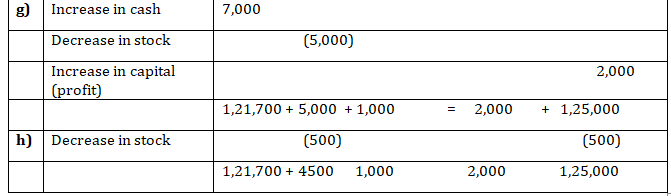

f. Rent outstanding Rs.5,000

g. Depreciation on building Rs.8,000

h. Cash withdrawn for personal use Rs.20,000

i. Rent received in advance Rs.5,000

j. Cash paid to Himani on account Rs.20,000

k. Cash received from Ashu Rs.30,000

Solution:-

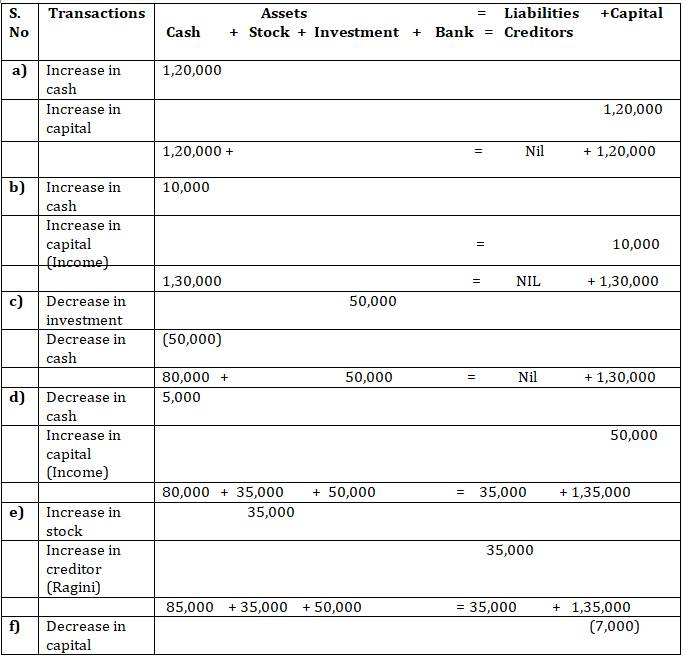

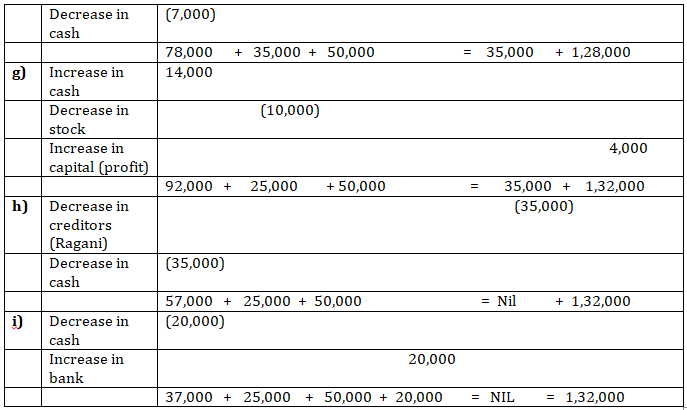

7. Show the effect of the following transactions on Assets, Liabilities and Capital through accounting equation:

- Started business with cash Rs.1,20,000

- Rent received Rs.10,000

- Invested in shares Rs.50,000

- Received dividend Rs.5,000

- Purchase goods on credit from Ragani Rs.35,000

- Paid cash for house hold Expenses Rs.7,000

- Sold goods for cash (costing Rs.10,000) Rs.14,000

- Cash paid to Ragani Rs.35,000

- Deposited into bank Rs.20,000

Solution:-

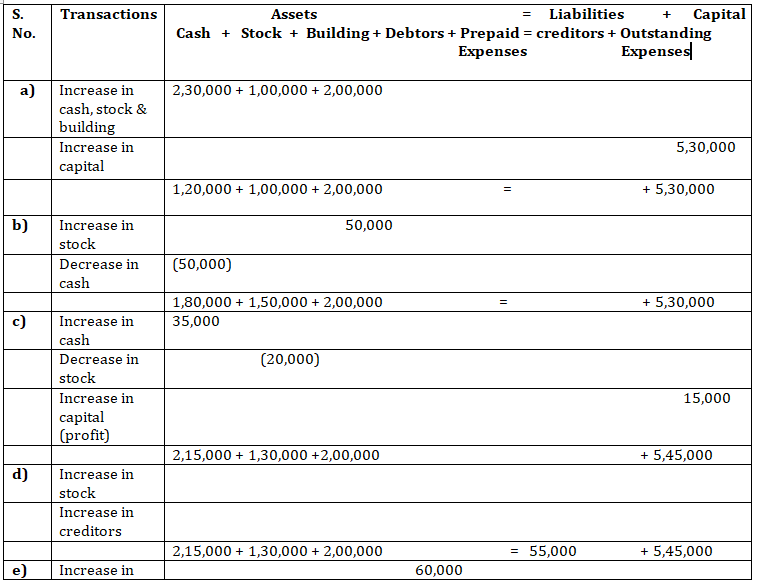

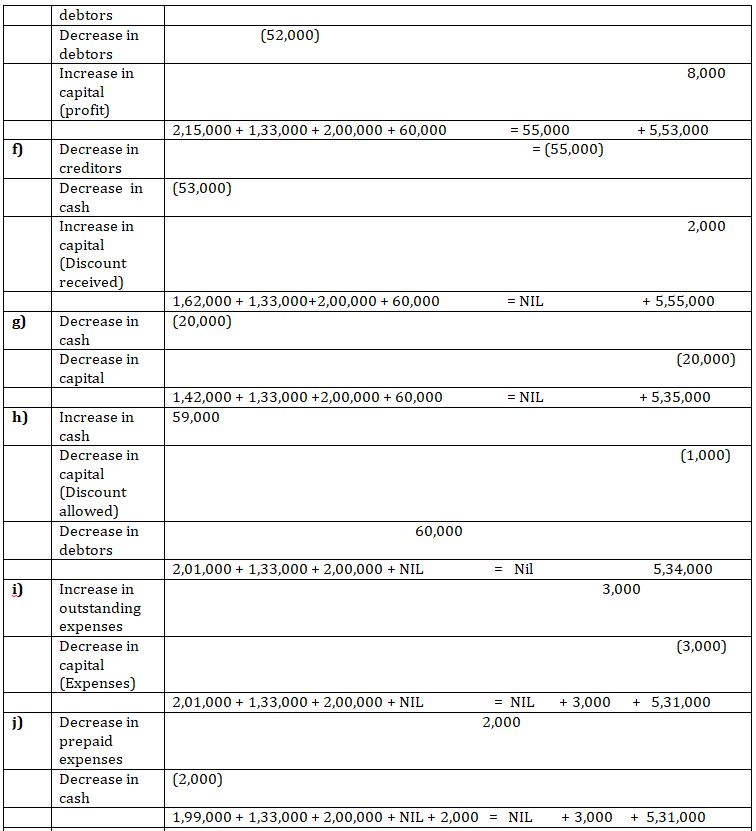

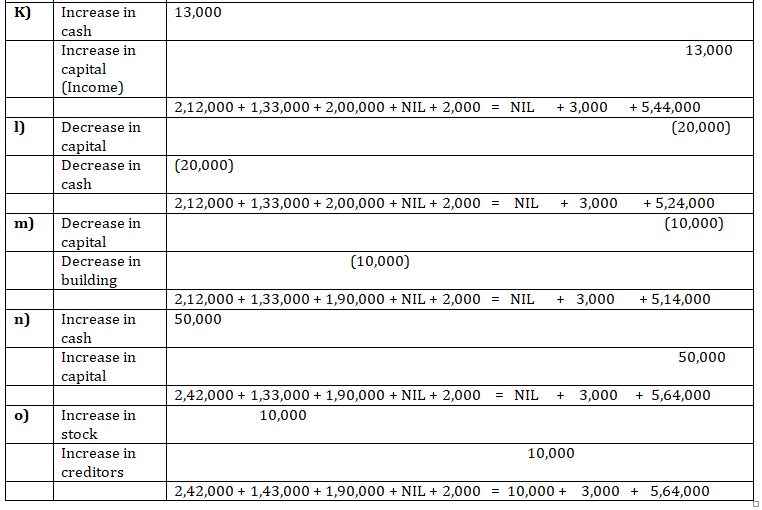

8. Show the effect of following transaction on the accounting equation:

a. Manoj started business with

- Cash Rs.2,30,000

- Goods Rs.1,00,000

- Building Rs.2,00,000

- He purchased goods for cash Rs.50,000

- He sold goods (costing Rs.20,000) Rs.35,000

- He purchased goods from Rahul Rs.55,000

- He sold goods to Varun (Costing Rs.52,000) Rs.60,000

- He paid cash to Rahul in full settlement Rs.53,000

- Salary paid by him Rs.20,000

- Received cash from Varun in full settlement Rs.59,000

- Rent outstanding Rs.3,000

- Prepaid Insurance Rs.2,000

- Commission received by him Rs.13,000

- Prepaid Insurance Rs.20,000

- Depreciation charge on building Rs.10,000

- Fresh capital invested Rs.50,000

- Purchased goods from Rakhi Rs.10,000

Solution:-

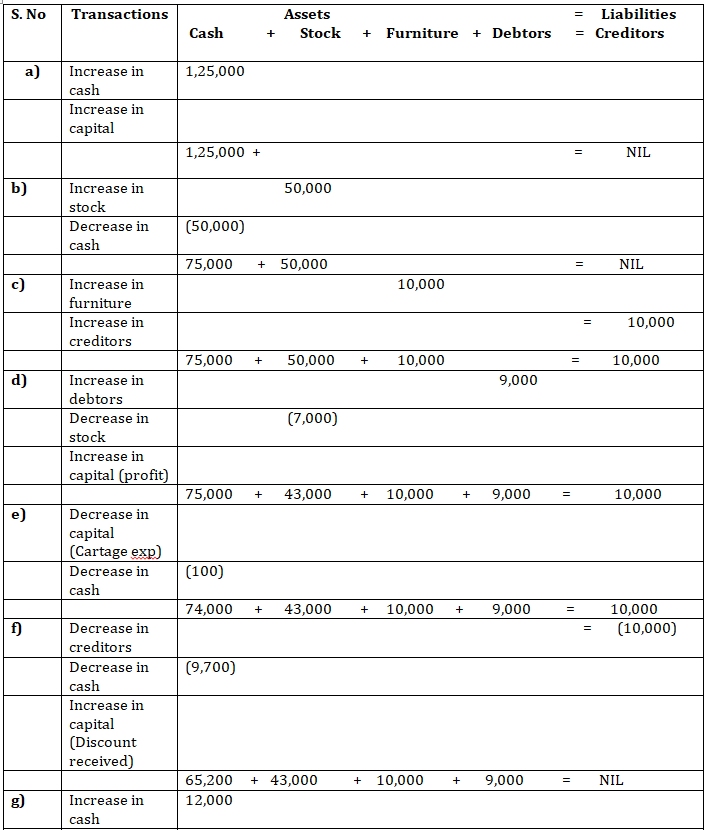

9. Transactions of M/s Vipin Traders are given below.

Show the effects on Assets, Liabilities and Capital with the help of accounting Equation.

- Business started with cash Rs.1,25,000

- Purchased goods for cash Rs.50,000

- Purchased furniture from R.K. Furniture Rs.10,000

- Sold goods to Parul Traders (Costing Rs.7,000 vide bill no. 5674) Rs.9,000

- Paid cartage Rs.100

- Cash paid to R.K. furniture in full settlement Rs.9,700

- Cash sales (costing Rs.10,000) Rs.12,000

- Rent received Rs.4,000

- Cash withdrew for personal use Rs.3,000

Solution:-

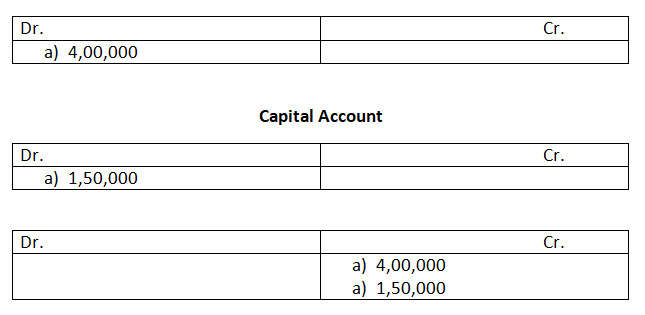

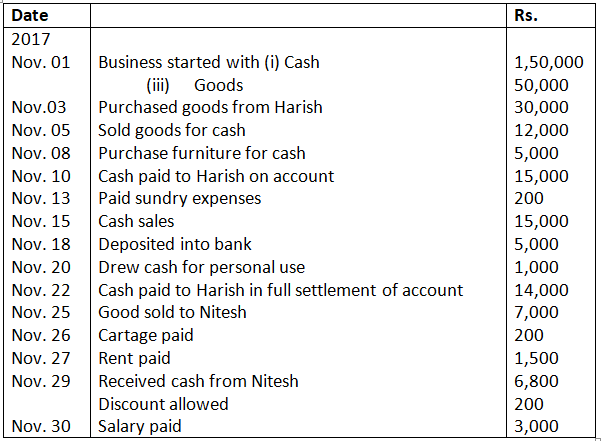

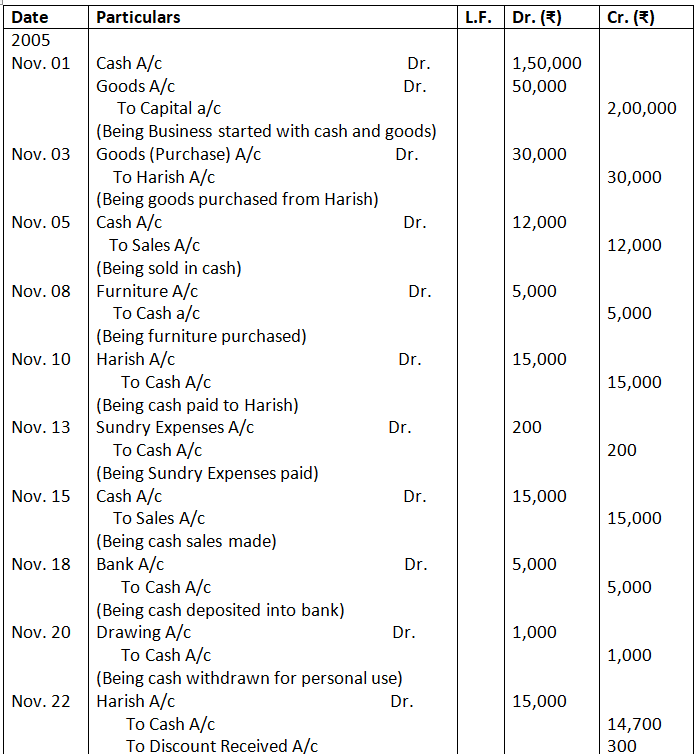

10. Bobby opened a consulting firm and completed these transactions during November, 2017:

- Invested Rs.4,00,000 cash and office equipment with Rs.1,50,000 in a business called Bobbie Consulting.

- Purchased land and a small office building. The land was worth Rs.1,50,000 and the building worth Rs.3,50,000. The purchase price was paid with Rs.2,00,000 cash and a long term note payable for Rs.3,00,000.

- Purchased office supplies on credit for Rs.12,000.

- Bobbie transferred title of motor car to the business. The motor car was worth Rs.90,000.

- Purchased for Rs.30,000 additional office equipment on credit.

- Paid Rs.75,000 salary to the office manager.

- Provided services to a client and collected Rs.30,000.

- Paid Rs.4,000 for the month’s utilities.

- Paid supplier created in transaction c.

- Purchase new office equipment by paying Rs.93,000 cash and trading in old equipment with a recorded cost of Rs.7,000.

- Completed services of a client for Rs.26,000. This amount is to be paid within 30 days.

- Received Rs.19,000 payment from the client created in transaction K.

- Bobby withdrew Rs.20,000 from the business.

Analyse the above stated transactions and open the following T-accounts:

Cash, client, office supplies, motor car, building, land, long term payables, capital, withdrawals, salary, expense and utilities expense.

Solution:-

a)

Office Equipment Account

b)

Land Account

Journalising

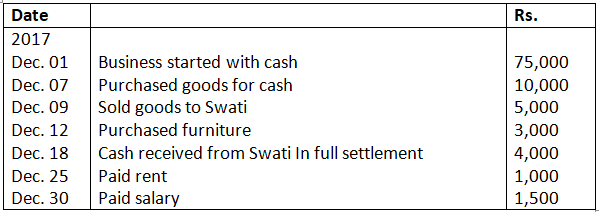

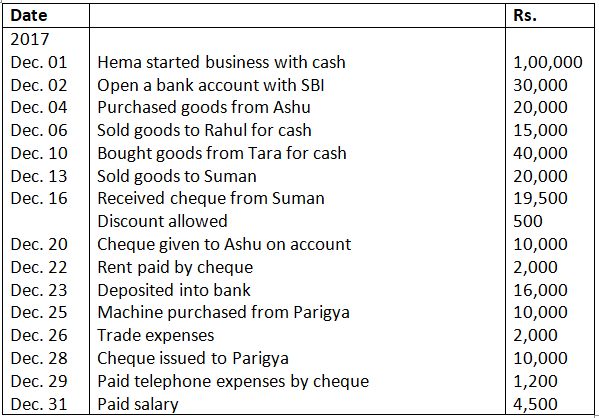

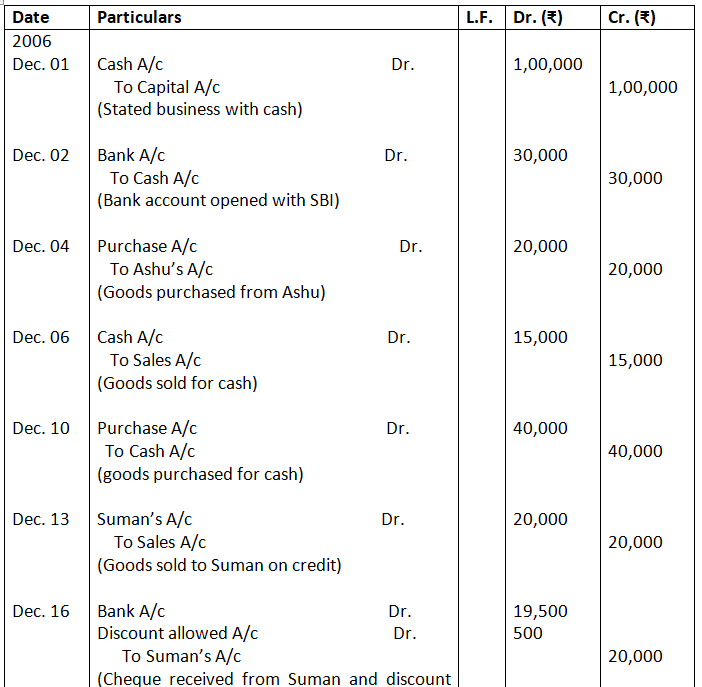

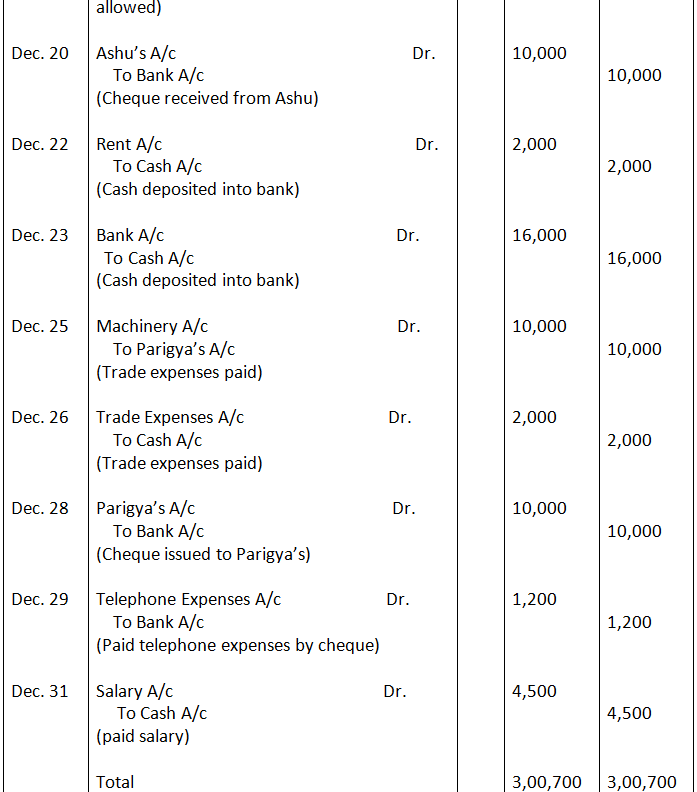

11. Journalise the following transactions in the books of Himanshu:

Solution:-

12. Enter the following Transactions in the Journal of Mudit:

Solution:-

13. Journalise the following transactions:

Solution:-

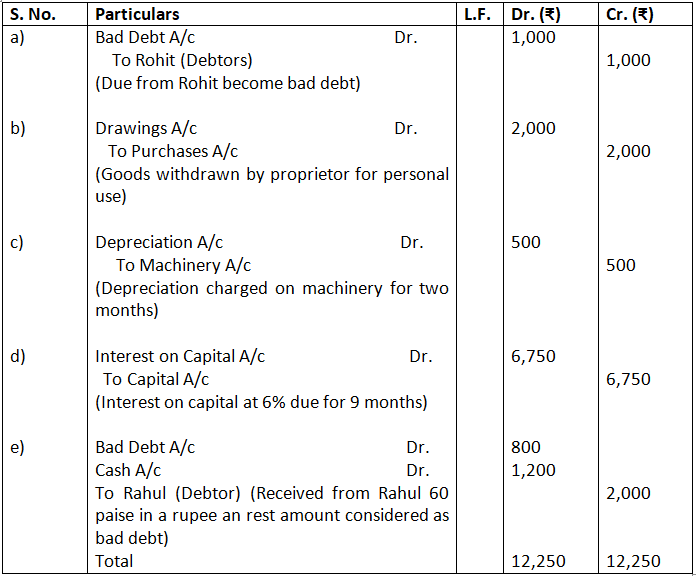

14. Journalise the following transactions in the books of Harpreet Bros.:

- Rs.1,000 due from Rohit are now bad debts.

- Goods worth Rs.2,000 were used by the debts.

- Charge depreciation @ 10% p.a. for two month on machine costing Rs.30,000

- Provide interest on capital of Rs.1,50,000 at 6% p.a. for 9 monthrs.

- Rahul become insolvent, who owed is Rs.2,000 a final dividend of 60 paise in a rupee is received from his estate.

Solution:-

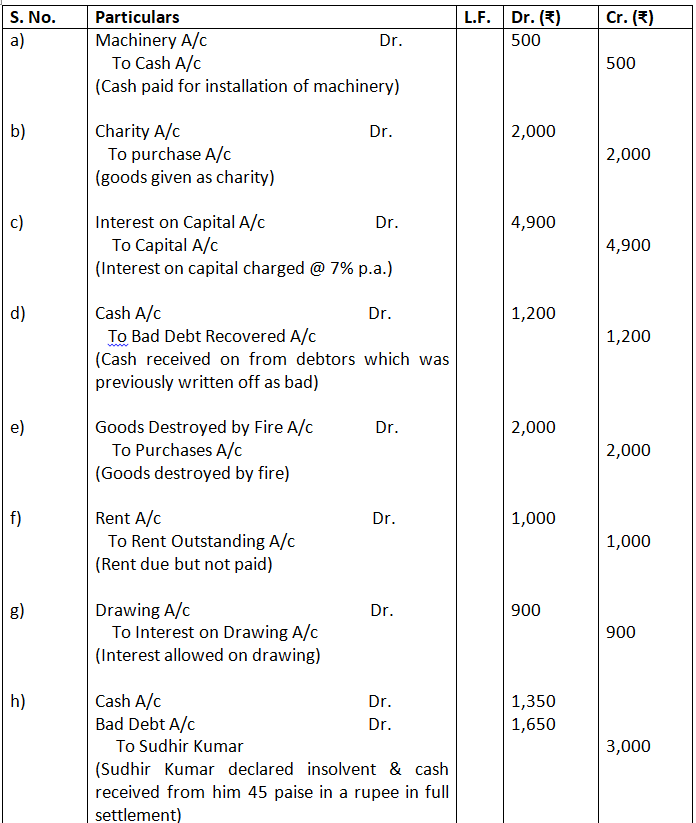

15. Prepare Journal from the transactions given below:

- Cash paid for installation of machine Rs.500

- Goods given as charity Rs.2,000

- Interest charge on capital @ 7% p.a. when total capital were Rs.70,000

- Received Rs.1,200 of a bad debts written-off last year.

- Goods destroyed by fire Rs.2,000

- Rent outstanding Rs.1,000

- Interest on drawings Rs.900

- Sudhir Kumar who owed me Rs.3,000 has failed to pay the amount. He pays me a compensation of 45 paise in a rupee.

- Commission received in advance Rs.7,000

Solution:-

Posting

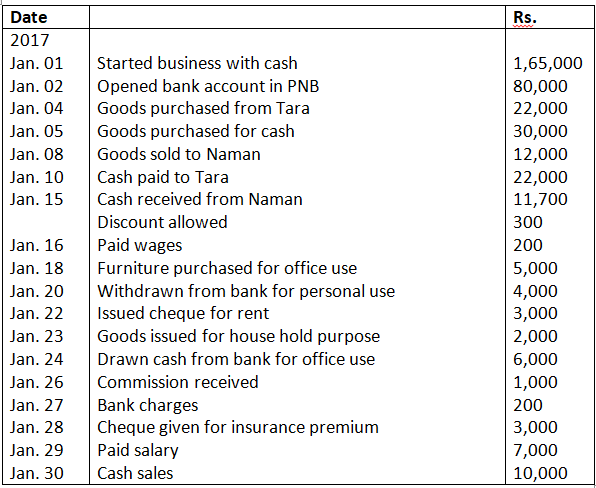

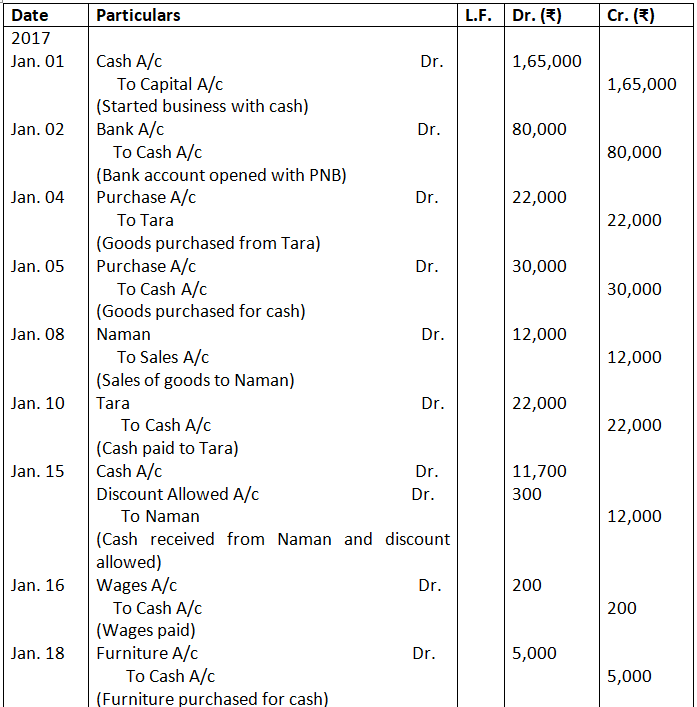

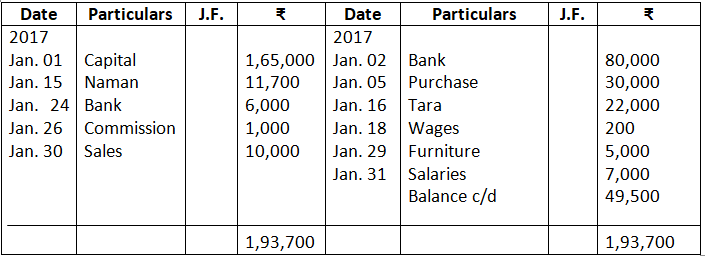

16. Journalise the following transactions, post to the ledger:

Solution:-

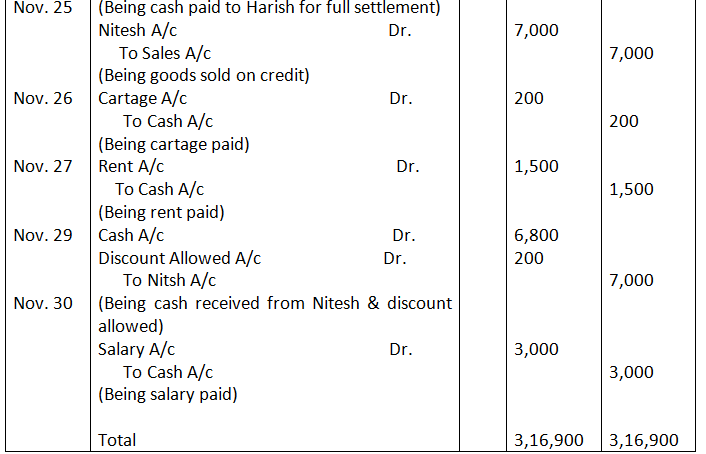

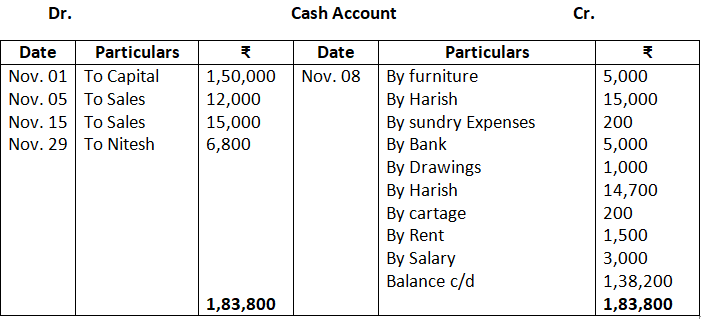

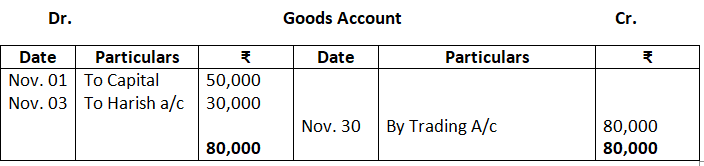

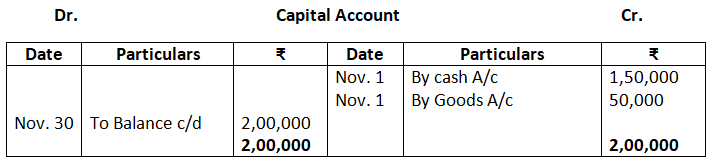

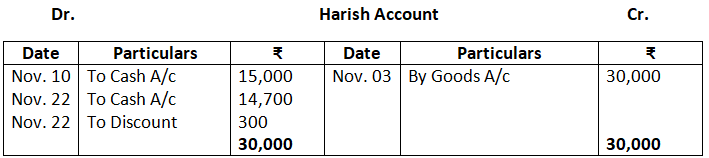

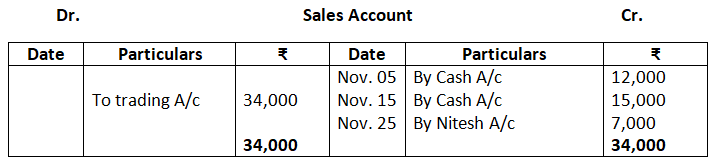

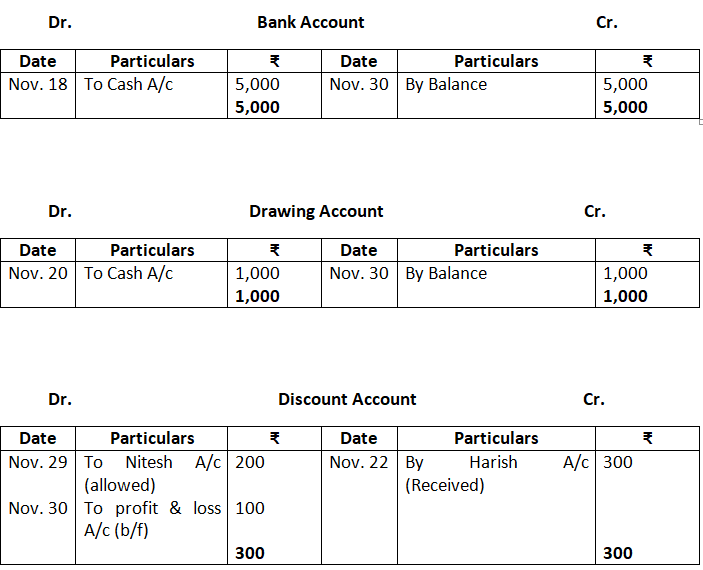

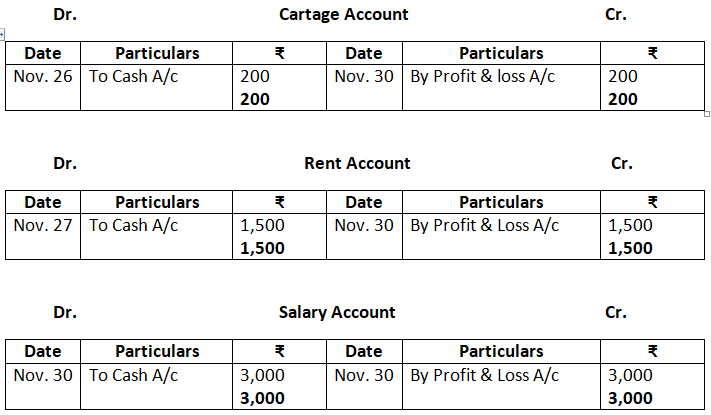

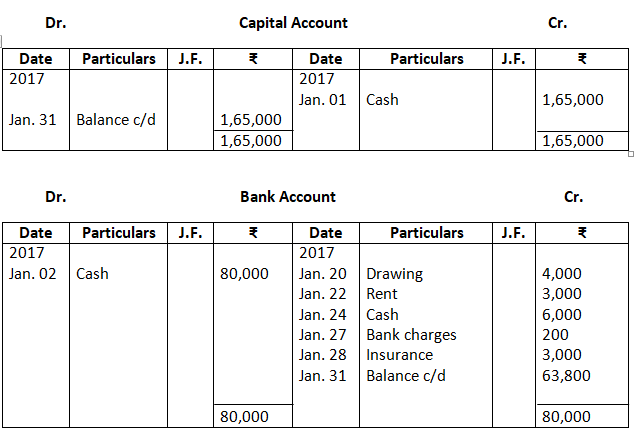

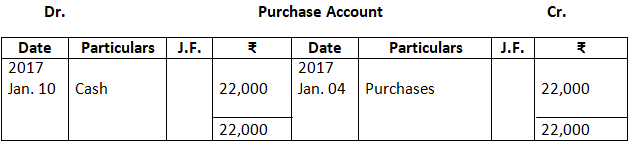

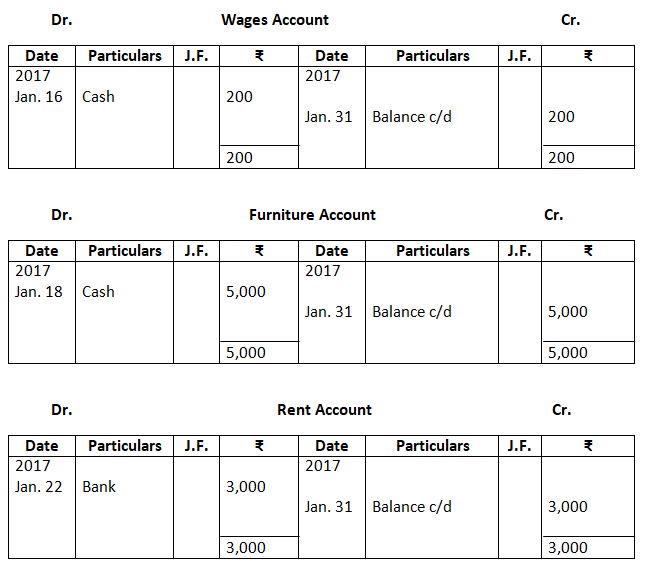

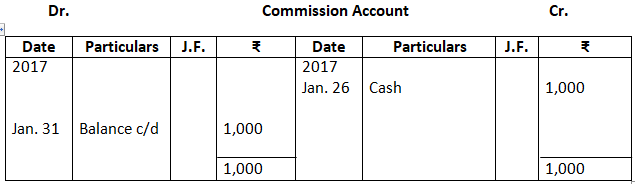

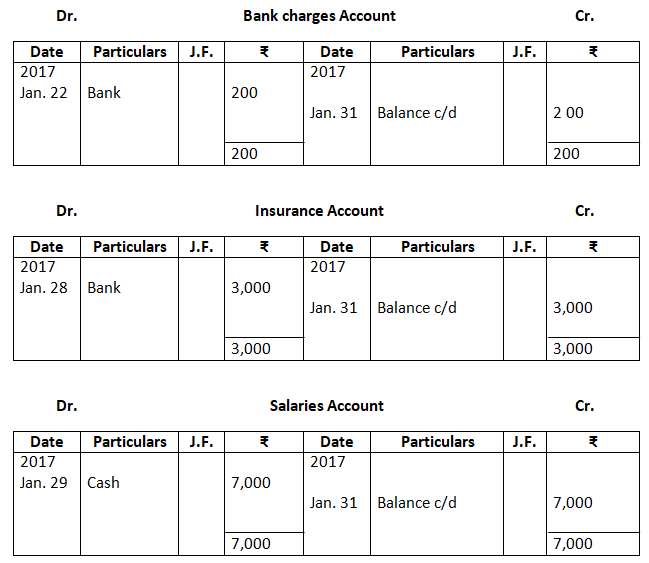

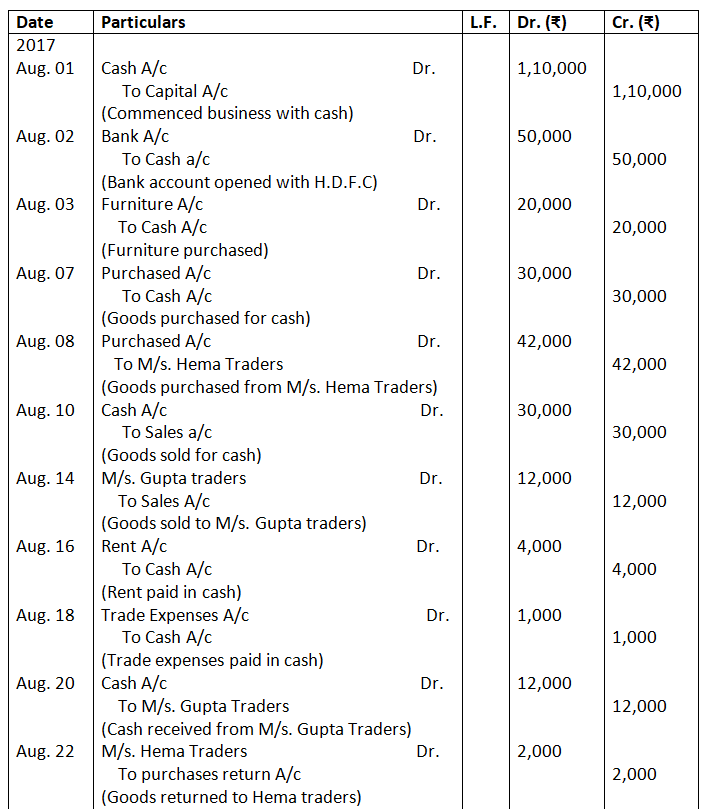

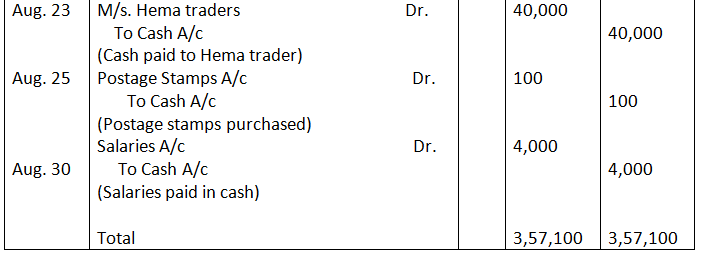

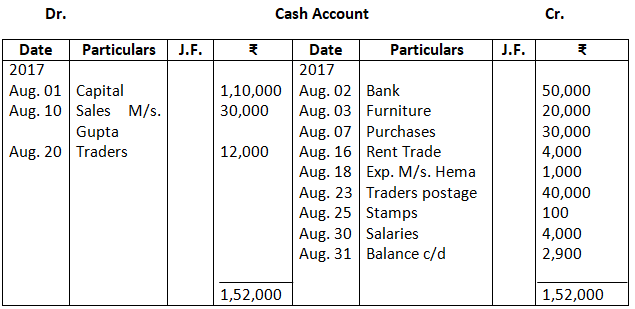

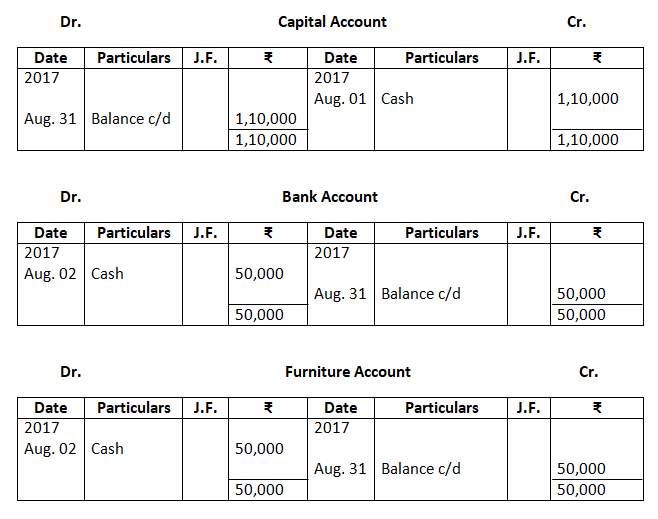

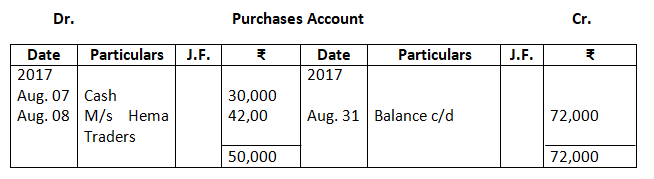

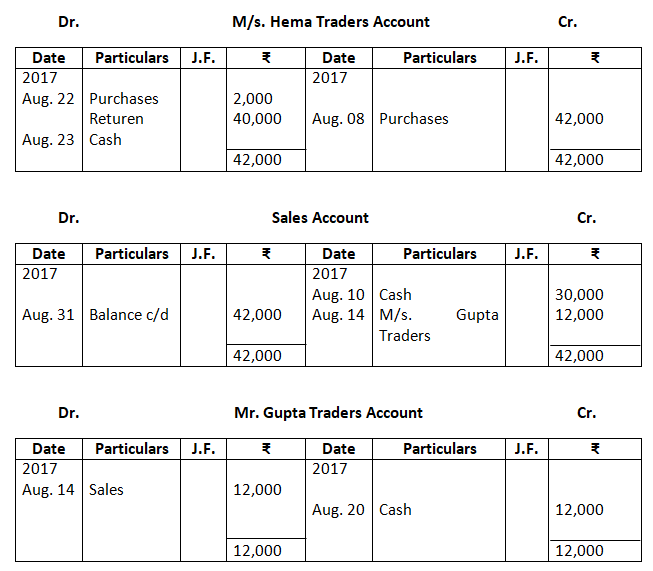

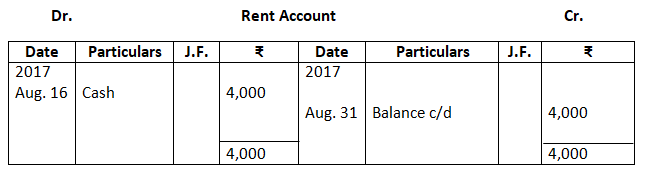

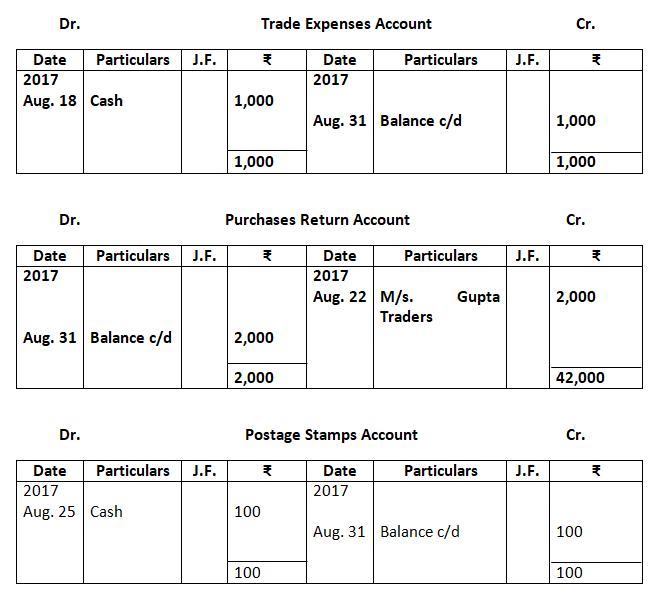

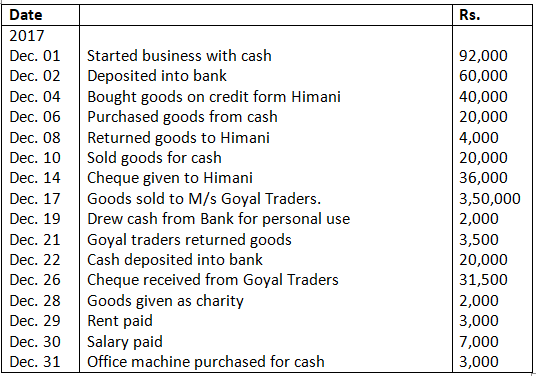

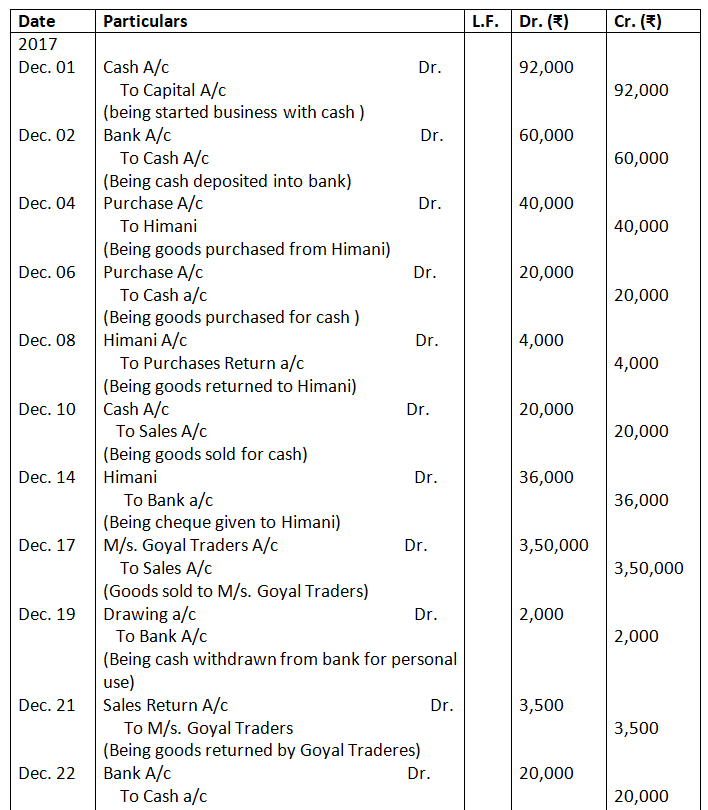

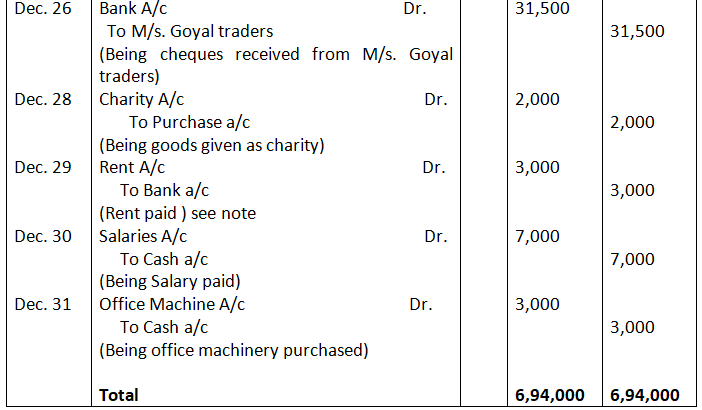

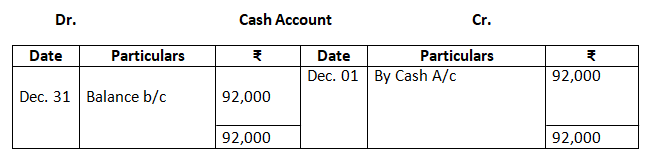

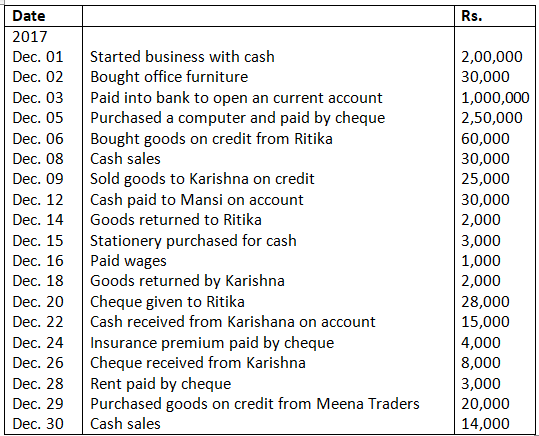

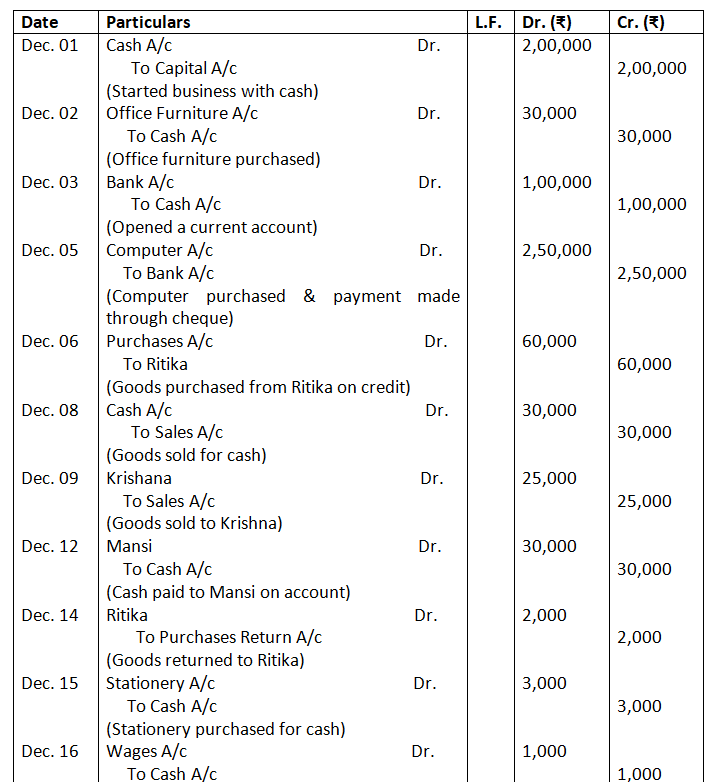

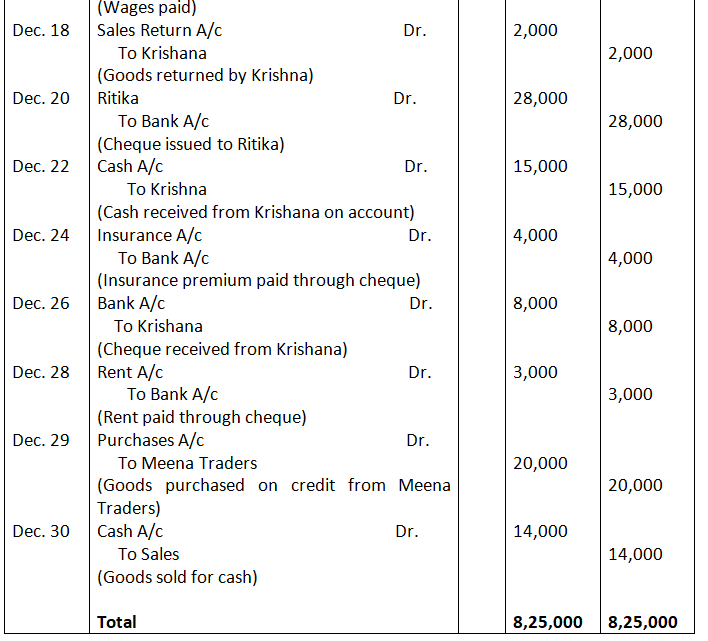

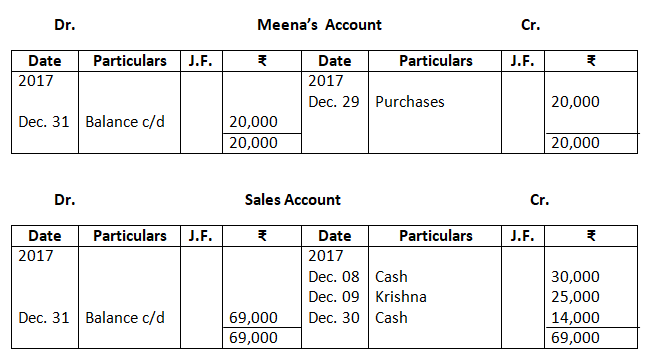

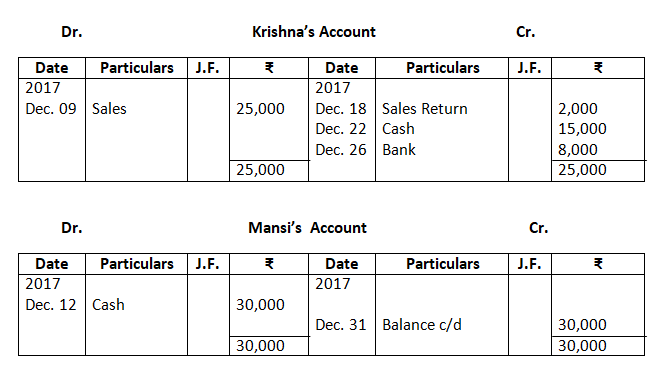

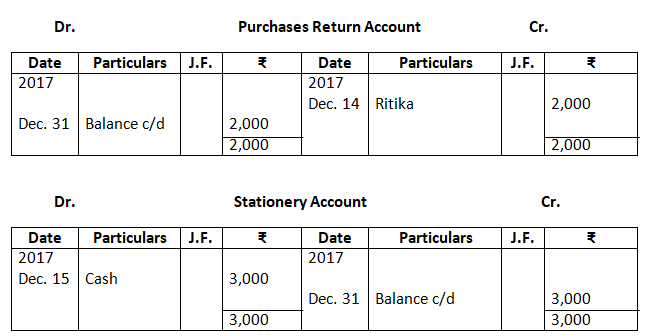

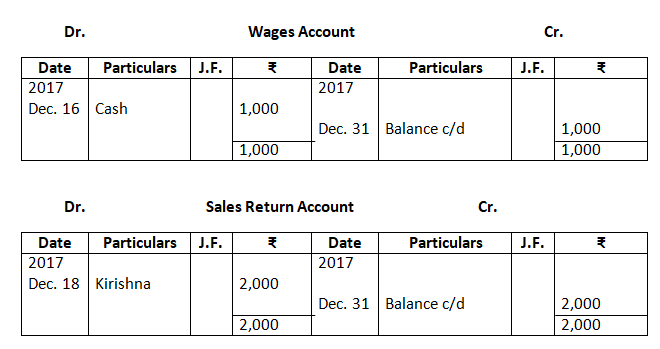

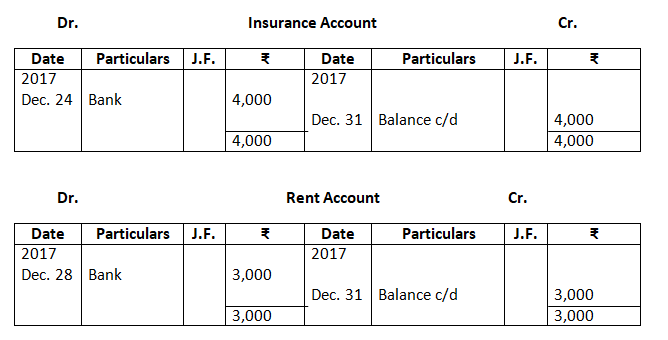

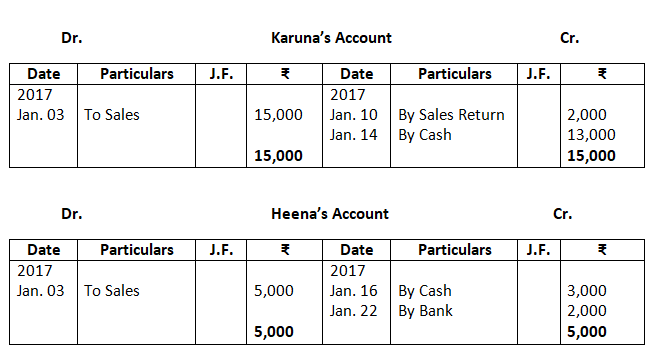

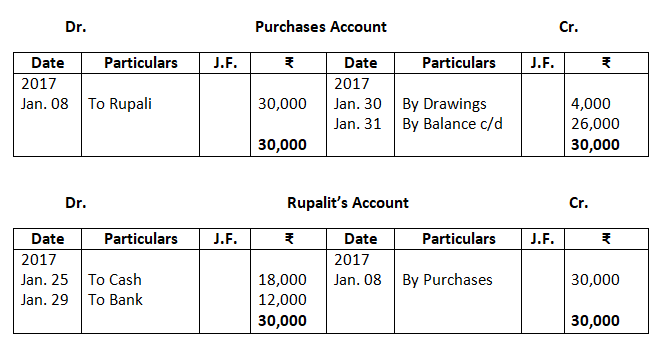

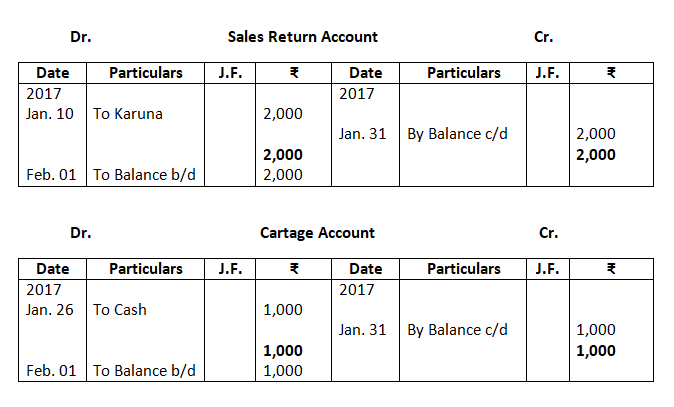

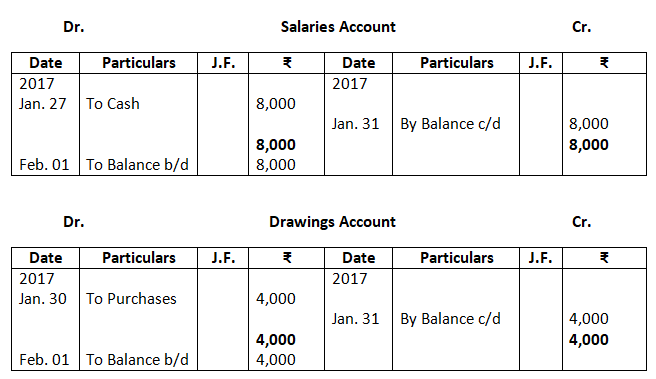

17. Journalise the following transactions is the journal of M/s Goel Brother and post them to the ledger.

Solution:-

Books of M/S. Goel Brothers

Journal

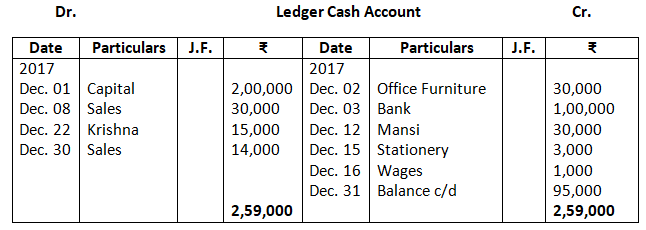

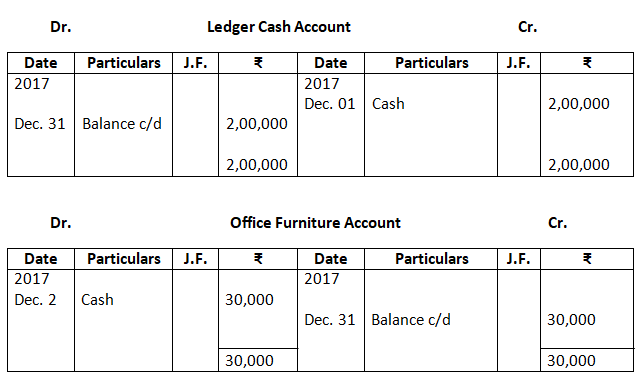

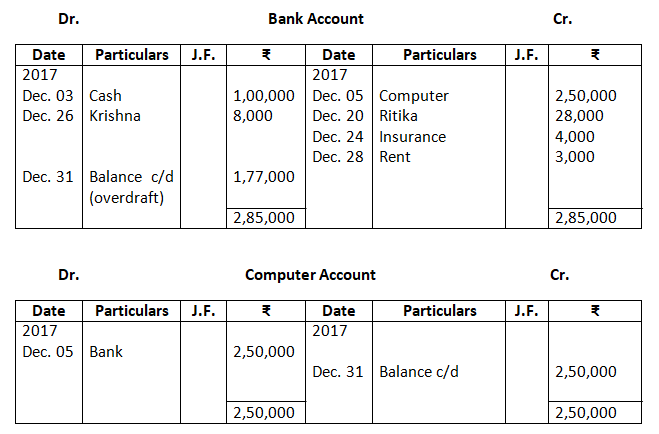

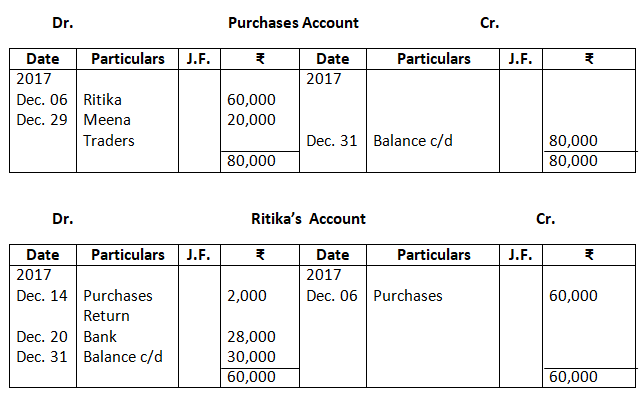

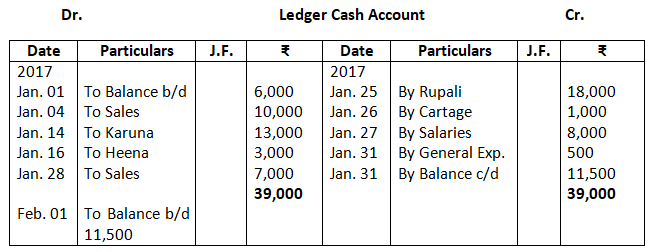

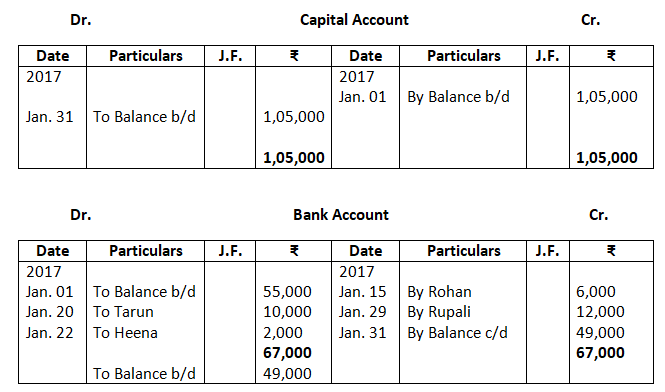

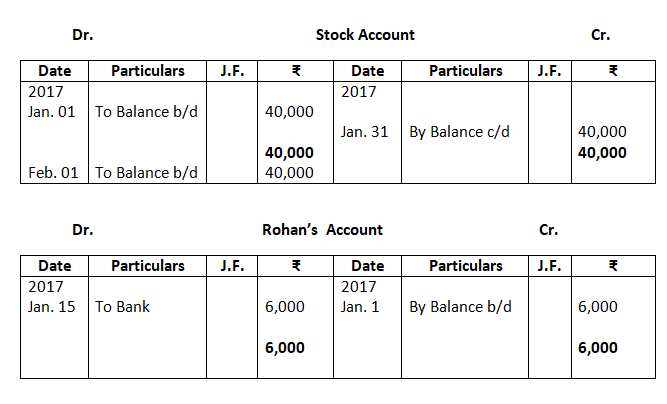

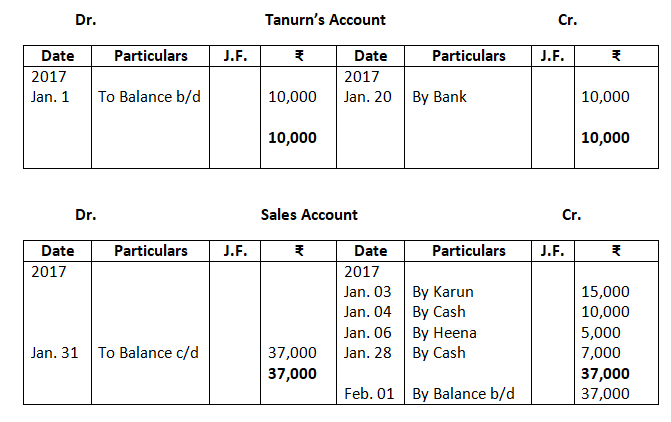

Dr. Ledger Cash Account Cr.

18. Give journal entries of M/s Mohit traders, Post them to the Ledger from the following transactions :

Solution:-

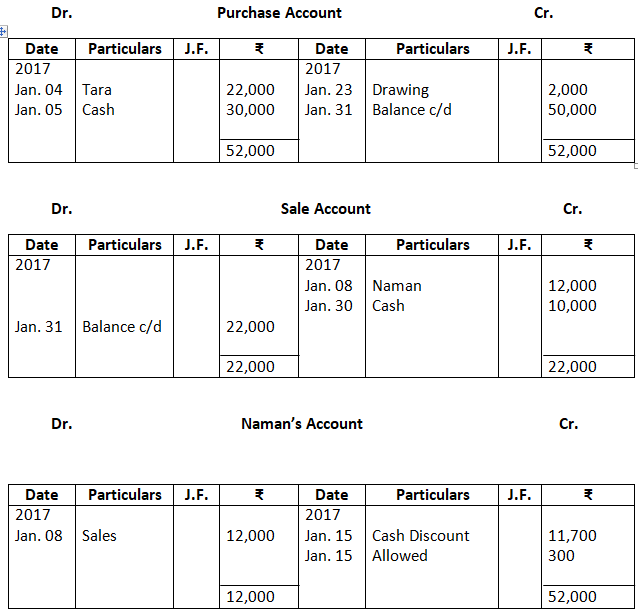

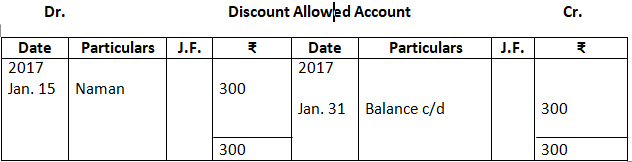

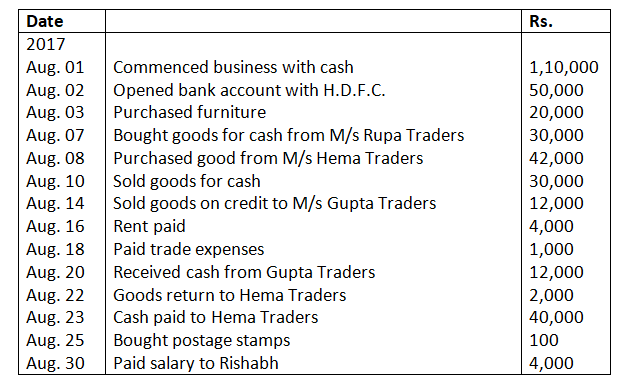

19. Journalise the following transaction in the Books of the M/s Bhanu Traders and post them into the ledger.

Solution:-

Books of M/s. Bhanu Traders

Journal

20. Journalise the following transaction in the book of M/s Beauti traders. Also post them in the ledger.

Solution:-

Books of Beauti Traders

Journal

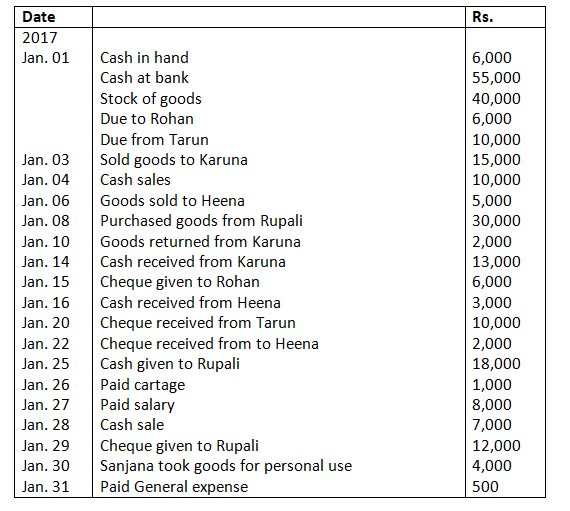

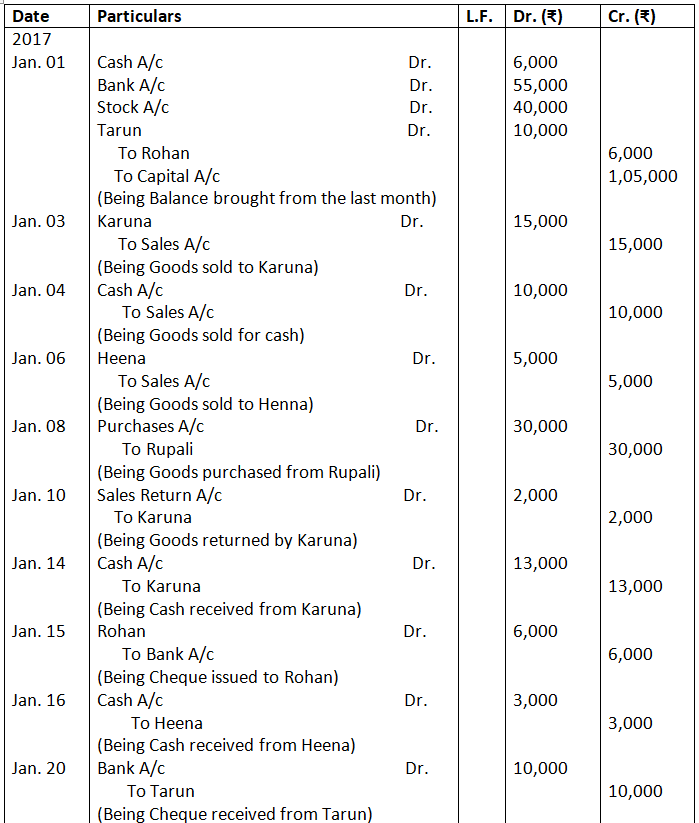

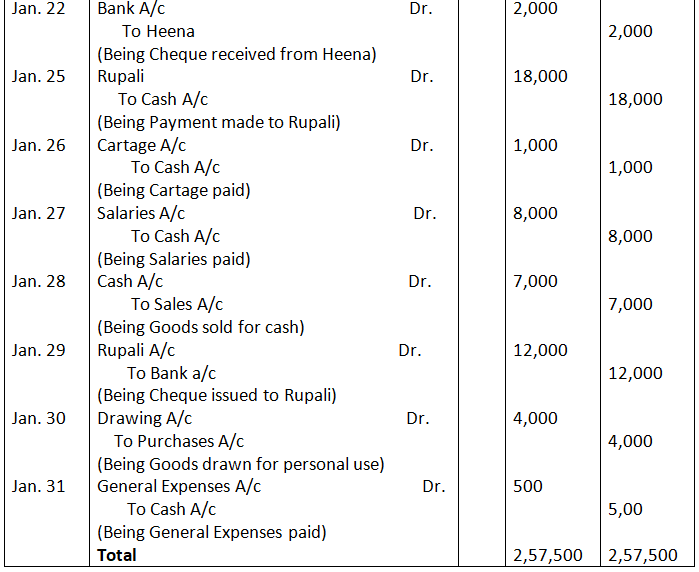

21. Journalise the following transaction in the books of Sanjana and post them into the ledger:

Solution:-

22. Record journal entries for the following transactions in the books of Anudeep of Delhi:

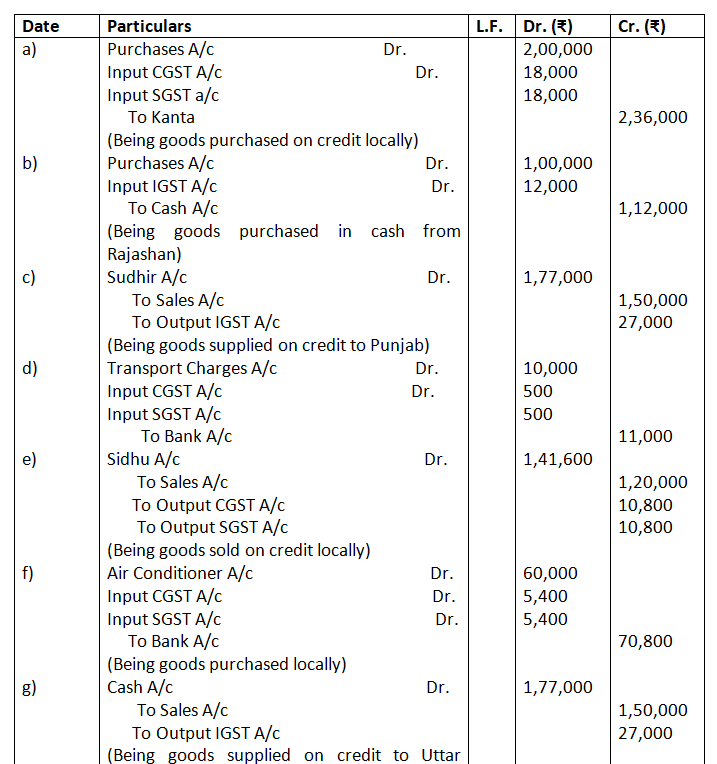

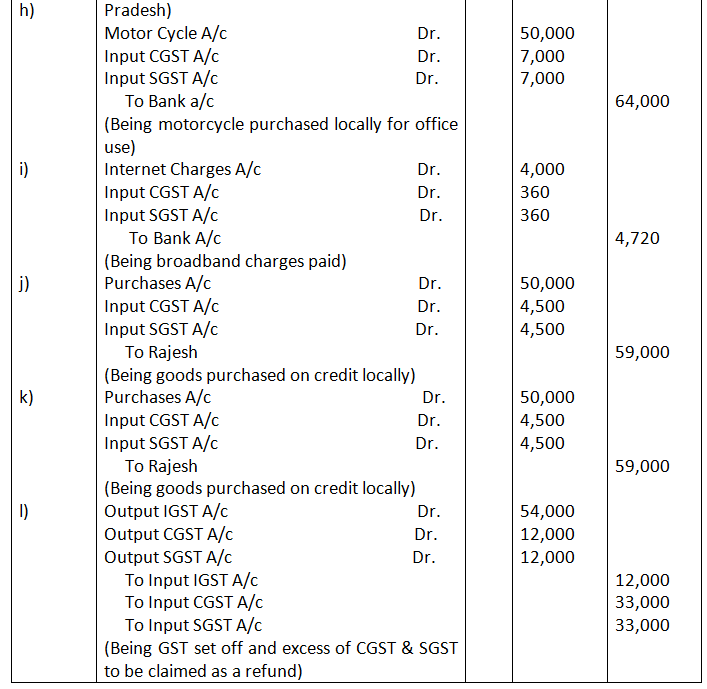

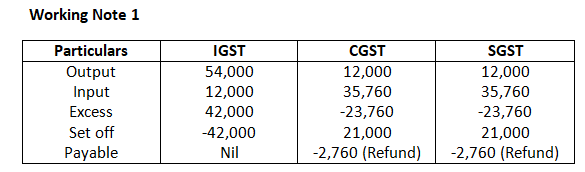

- Bought goods Rs.2,00,000 form Kanta of Delhi (CGST @ 9%, SGST @ 9%)

- Bought goods Rs.1,00,000 for cash from Rajasthan (IGST @ 12%)

- Sold goods Rs.1,50,000 to Sudhir of Punjab (IGST @ 18%)

- Paid for Railway Transport Rs.10,000 (CGST @ 5% , SGST @ 5%)

- Sold goods Rs.1,20,000 to Sidhu of Delhi (CGST @ 9%, SGST @ 9%)

- Bought Air-Condition for office use Rs.60,000 (CGST @ 9%, SGST @ 9%)

- Sold goods Rs.1,50,000 for cash to Sunil to Uttar Pradesh (IGST 18%)

- Bought Motor Cycle for business use Rs.50,000 (CGST 14%, SGST @ 14%)

- Paid for Broadband services Rs.4,000 (CGST @ 9%, SGST @ 0%)

- Bought goods Rs.50,000 from Rajesh, Delhi (CGST @ 9%, SGST @ 9%)

Solution:-