- What are the heads in the Equity and Liabilities part of the Balance Sheet as per Schedule III?

Ans. :-

- Shareholders’ Funds;

- Share Application Money Pending Allotment;

- Non-current Liabilities;

- Current Liabilities.

2. Under which major head will the following be show:

- Share Capital; and

- Money Received Against Share Warrants?

Ans. :-

- Shareholder’s Funds;

- Shareholder’s Funds.

3. List any five items that are shown under Reserve and Surplus.

Ans. :-

Capital Reserve;

Capital Redemption Reserve;

Debentures Redemption Reserve;

Securities Premium Reserve and Surplus, i.e., Balance is Statement of Profit and Loss.

4. Under which sub-head will the following be classified or shown:

- Long-term Borrowings;

- Deferred Tax Liabilities (Net); and

- Long-term Provision?

Ans. :- Non-current liabilities.

5. Name the items that are shown under Long-term Borrowings.

Ans. :- Bonds;

Debentures;

Long-term Loan from Bank;

Long-term Loans from Others;

Public Deposits.

6. State giving reason whether Trade Receivables are classified as Current Assets or Non-current Assets in the Balance Sheet of a Company as per Schedule III of the Companies Act, 2013 in the following cases:

Ans. :-

- Current Assets;

- Current Assets;

- Non-current Assets;

- Current Assets;

- Non-current Assets.

7. State giving reason whether Trade Payables are classified as Current Liabilities or Non-current Liabilities in the Balance Sheet of a Company as per Schedule III of the Companies Act, 2013 in the following cases:

- Current Liabilities;

- Current Liabilities;

- Non-current Liabilities;

- Current Liabilities;

- Non-current Liabilities.

8.Under which head and how are the following items shown in the Balance Sheet of a company under Schedule III;

- Calls-in-Arrears;

- Share Application Money Pending Allotment;

- Unpaid Dividend; and

- Dividend not paid on Cumulative Preference Shares?

Ans.:-

- Calls-in-Arrears is shown under Shareholder’s Funds by way of deduction from ‘Subscribed but not fully paid-up’ under Subscribed Capital.

- Share Application Money Pending Allotment is shown as a separate line item between Equity and Non-current Liabilities.

- Unpaid Dividend is shown as Other Current Liabilities under Current Liabilities.

- Dividend not paid on cumulative Preference Shares is shown as Contingent Liability in the Notes to Accounts.

9.Under which head and sub-head of Equity and Liabilities part of the Balance Sheet are the following items classified or shown:

- Bonds;

- Debentures;

- Public Deposits;

- Capital Redemption

- Forfeited Shares Account;

- Sundry Creditors;

- Interest Accrued but Not Due on Debentures;

- Interest Payable.

Ans.:-

- Long-term borrowings under Non-Current Liabilities;

- Long term Borrowings under Non-current Liabilities;

- Long term Borrowings under Non-current Liabilities;

- Reserve and Surplus under Shareholder’s Funds;

- Subscribed Capital under the sub-head Share Capital under the main head Shareholders’ funds (Shown by way of addition to Subscribed Capital);

- Trade Payable under Current Liabilities;

- Other Current Liabilities under current Liabilities.

10.State any two items that are included in the following major head under which liabilities of a company are shown:

- Reserves and Surplus;

- Long-term Borrowings;

- Short-term Borrowings;

- Other Current Liabilities.

Ans.:-

- Reserve and surplus: Capital Reserve; Capital Redemption Reserve;

- Long-term Borrowings: Debentures; Term Loans from bank; Long-term Loans from Others; Public Deposits;

- Short-term Borrowings: Bank Overdraft; Cash Credit from Bank;

- Other Current Liabilities: Unpaid Dividend; Current Maturities of Long-term Debts; Interest Accrued and Due on borrowings.

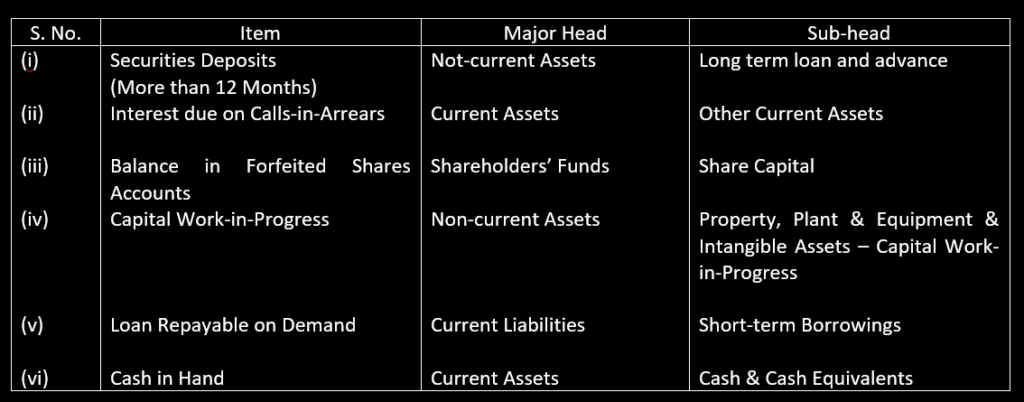

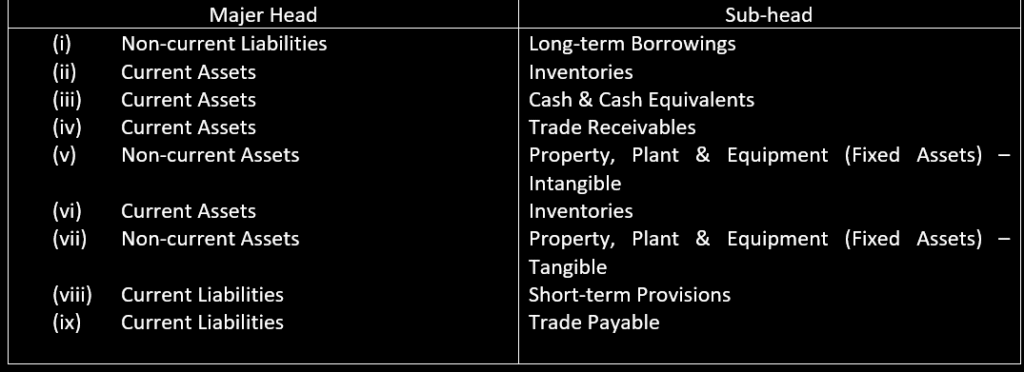

11. Classify the following items under Major heads and Sub-heads (if any) in the Balance Sheet of a company as per Schedule III of the Companies Act 2013:

- Securities Deposits (More than 12 months);

- Interest due on Calls-in-Arrears;

- Balance in Forfeited Shares Account;

- Capital Work-in-Progress;

- Loan Repayable on Demand;

- Cash in Hand.

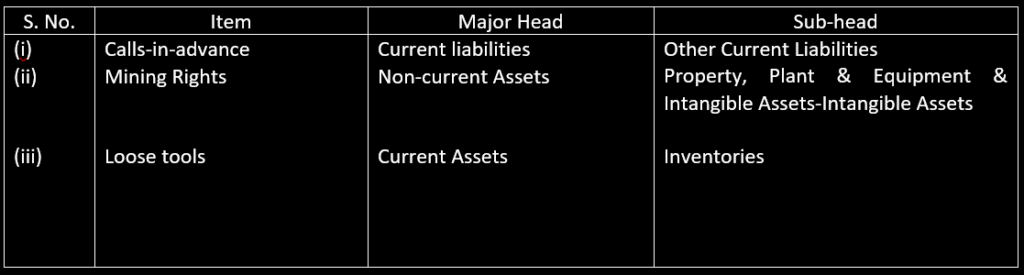

12.Classify the following items under major heads and sub-heads (if any) in the Balance Sheet of a company as per Schedule III, Part I of the Companies Act, 2013:

- Calls in advance;

- Mining rights;

- Loose tools.

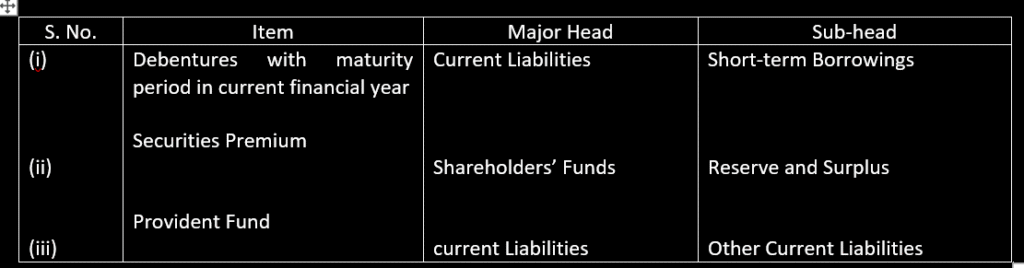

13. Under which major heads and sub-heads will the following items be placed in the Balance Sheet of the company as per Schedule III, Part I of the Companies Act, 2013?

Debentures with maturity period in current financial year;

Securities Premium;

Provident Fund.

14. Under which heads the following items on the Assets part of the Balance sheet of a company will be shown:

- Sundry Debtors;

- Patents and Trademark;

- Shares in Quoted Companies;

- Advances recoverable in cash;

- Prepaid Insurance; and

- Work-in-Progress?

Ans.:- Head (Sub-head, if any):

- Current Assets (Trade Receivables);

- Non-current Assets, Property, Plant and Equipment (fixed Assets) – Intangible Asset);

- Non-current Asset (Non – current Investments);

- Current Assets (Short-term Loans and Advances);

- Current Assets (Other Current Assets);

- Current Assets (Inventories).

15.

Under which of the major heads will the following items be shown in the Balance Sheet of a company as per Schedule III of the Company Act, 2013:

- 10% Debentures;

- Stock-in-Trade;

- Cash at Bank;

- Bills Receivables;

- Goodwill;

- Loose Tools;

- Truck;

- Provision for Tax; and

- Interest Accrued and due on unsecured Loan?

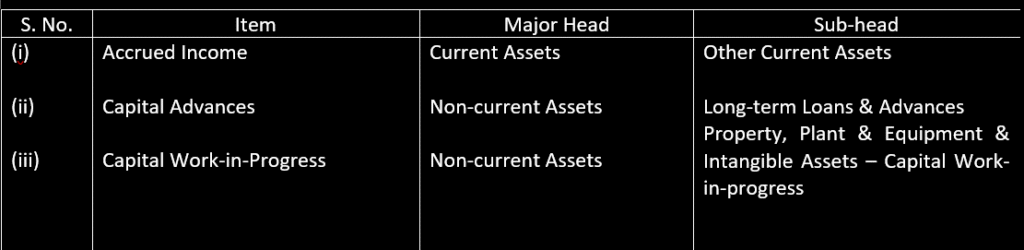

16.Classify the following items under Major Heads and Sub-heads (if any) in the Balance Sheet of a company as per Schedule III, Part of the Company Act, 2013:

- Accrued Income;

- Capital Advance;

- Capital work-in-Progress.

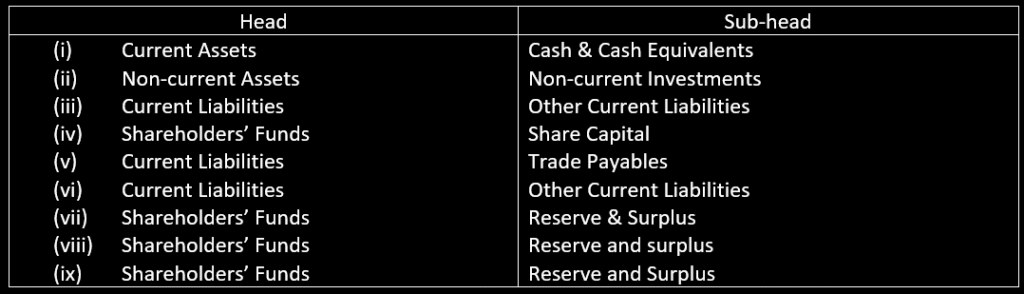

17. Under which heads will the following items be shown in the Balance Sheet of a Company;

- Bank Balance;

- Investments (Long-term);

- Outstanding Salary;

- Subscribed and paid-up Capital

- Bills Payable;

- Unclaimed Dividends;

- Shares Option Outstanding Account; and

- General Reserve;

- Uncalled Liability on Shares?

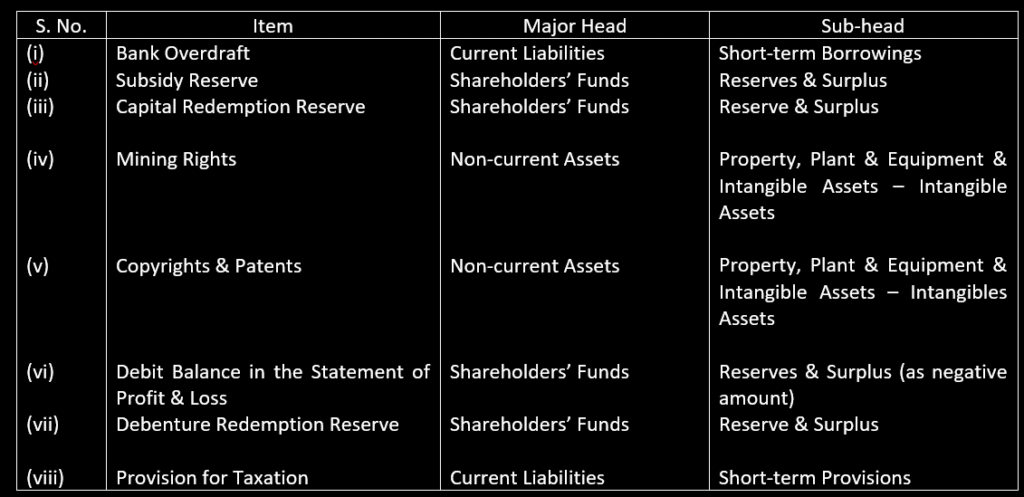

18. Under which major heads and sub-heads will the following items be presented in the Balance Sheet of the company as per Schedule III, Part I of the Company Act, 2013?

Bank Overdraft

Subsidy Reserve

Capital Redemption Reserve

Mining Rights

Copyrights and Patents

Debit balance in the Statement of Profit & Loss

Debenture Redemption Reserve

Provision for Taxation

19. Under which heads following are shown in a company’s Balance Sheet;

- Public Deposits;

- Office Furniture;

- Prepaid Rent;

- Outstanding Salaries;

- Computer Software;

- Interest Accrued on Investment;

- Trade Payable payables after 12 months from the date of Balance Sheet?

Ans.:-

- Long-term Borrowings under Non-current Liabilities;

- Property, Plant & Equipment & Intangible Assets – Property, Plant & Equipment under Non-current Assets;

- Other Current Assets under Current Assets;

- Other Current Liabilities under Current Liabilities;

- Property, Plant & Equipment & Intangible Assets – Intangible Assets under Non-current Assets;

- Other Current Assets under Current Assets;

- Other Long-term Liabilities under Non-current Liabilities.

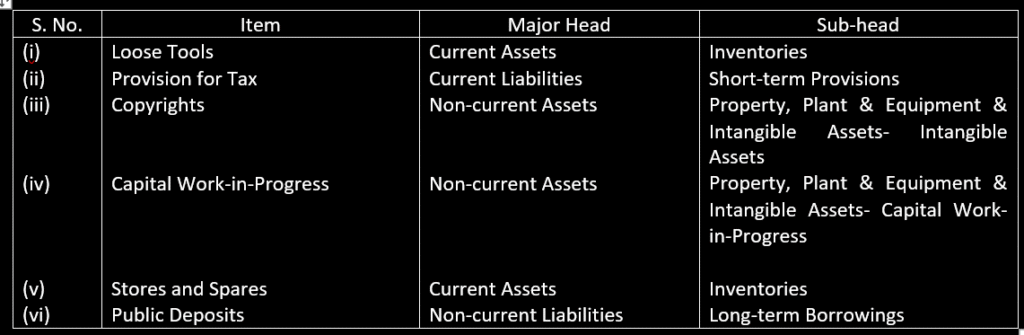

20. Classify the following items under major heads and sub-heads (if any) in the Balance sheet of the company as per Schedule III, Part I of the companies Act, 2013:

- Loose tools

- Provision for Tax

- Copyrights

- Capital Work-in-Progress

- Stores and Spares

- Public Deposits

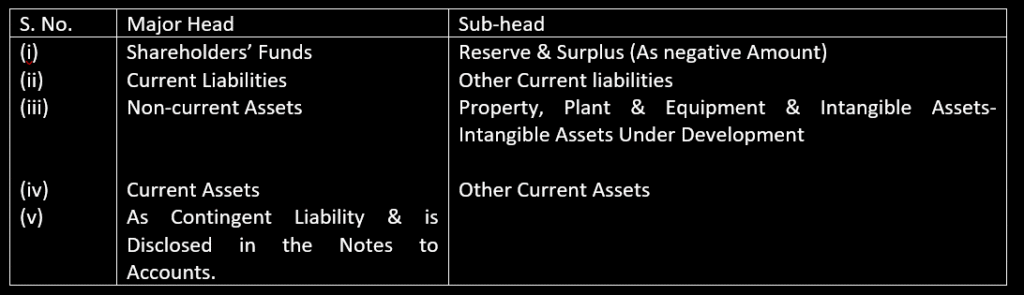

21.How are the following items shown while preparing Balance Sheet of a company;

- Surplus, i.e., Balance in Statement of Profit & Loss (Dr.);

- Interest accrued and due on Debentures;

- Computer Software under development;

- Interest accrued on Investment;

- Arrears of dividends on Cumulative Preference Shares?

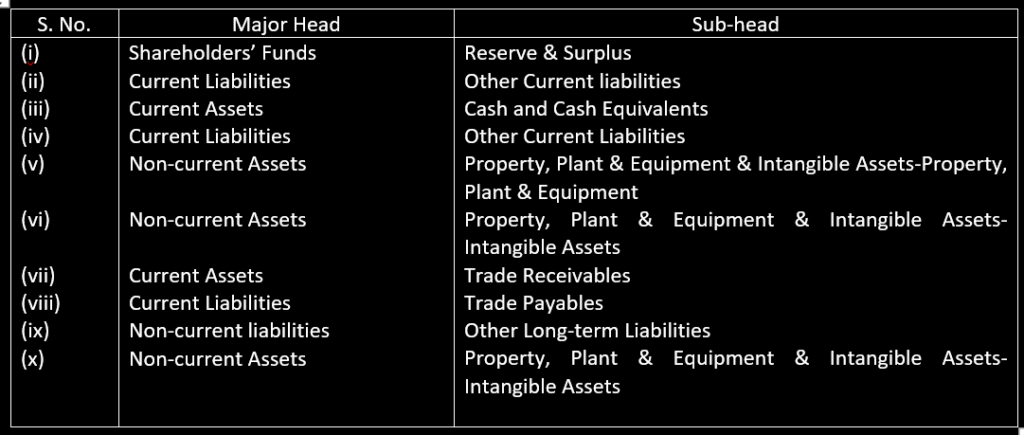

22. Under which heads and sub-heads are the following items shown in the Balance Sheet of a Company as per Schedule III, Part I of the Companies Act, 2013?

Securities Premium

Interest accrued and due on secured loans

Cash and Bank balance

Interest accrued but not due

Building

Mining Rights

Sundry Debtors

Sundry Creditors

Premium on Redemption of Debentures

Mastheads and Publishing Title

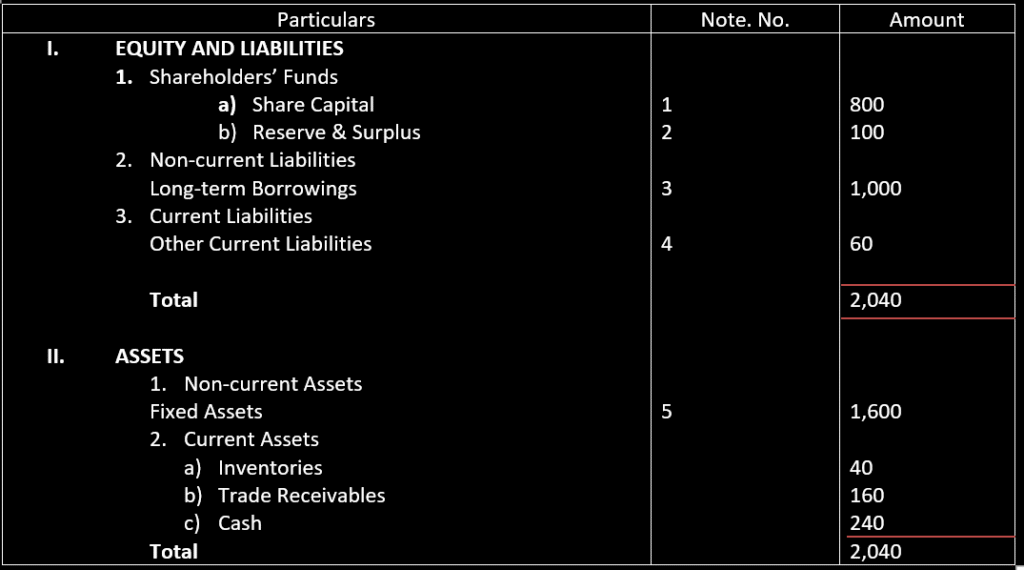

23.Prepare Balance Sheet of Recovery Ltd. As per Schedule III of the companies Act, 2013:

10% Debentures of Rs.100 each Rs.1,90,000

Stock-in-Trade (Inventories) Rs.40,000

Goodwill Rs.20,000

Provision for Tax Rs.6,000

Totaling of Balance Sheet is not required.

Ans.:- Long-term Borrowings (10% Debentures): Rs.1,90,000

Short-term provisions (Provision for Tax): Rs.6,000

Property, Plant & Equipment & Intangible Assets

-Intangible Assets (Goodwill): Rs.20,000

Current Assets (Inventories): Rs.40,000

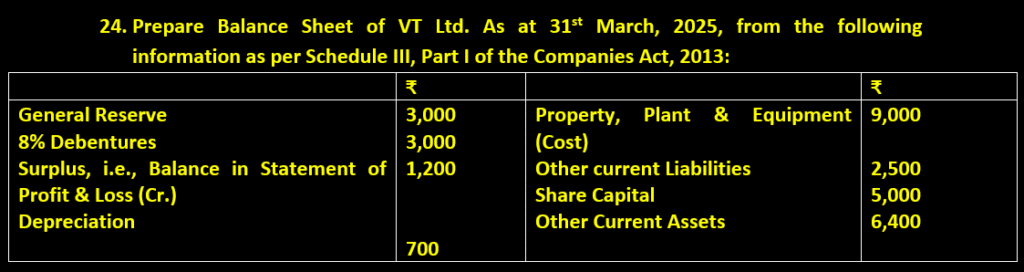

24.

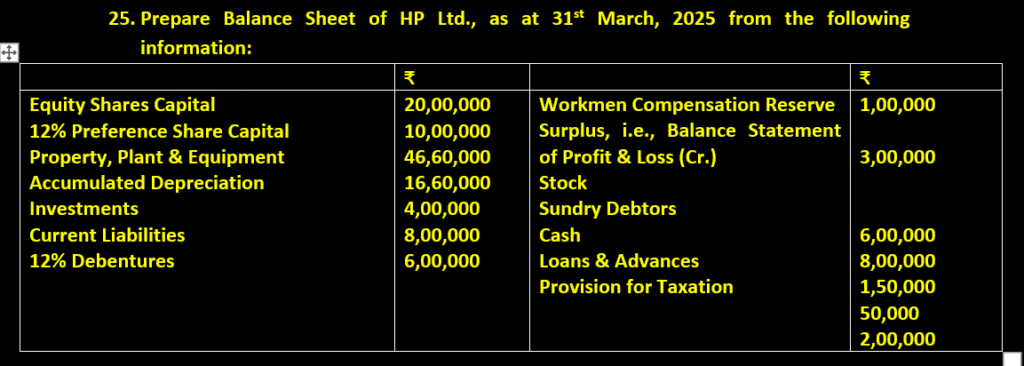

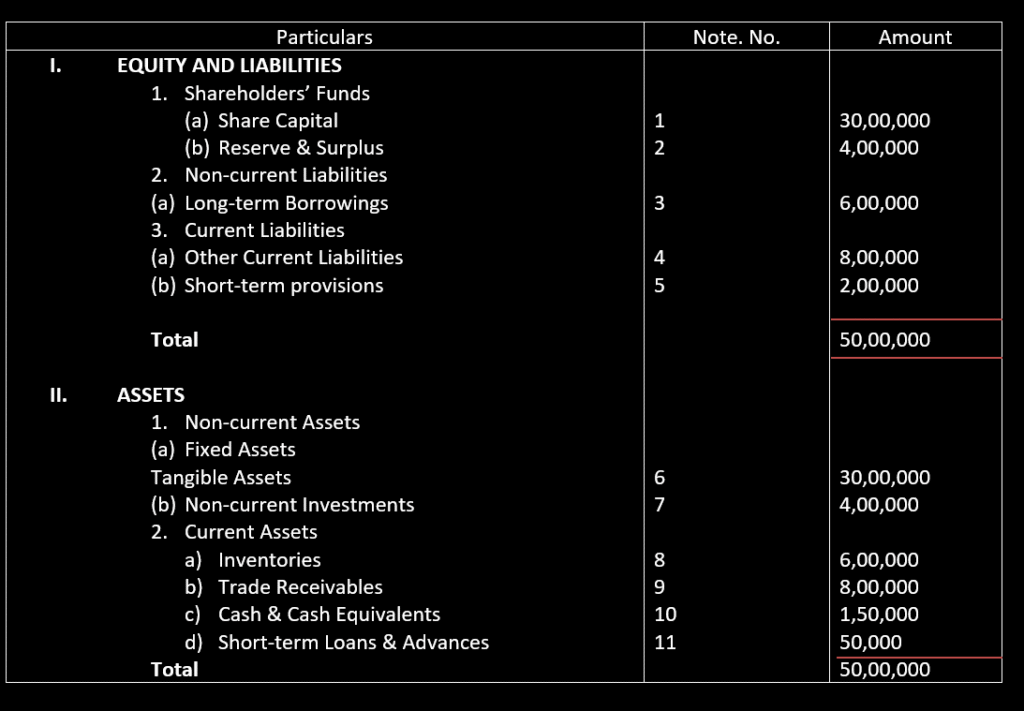

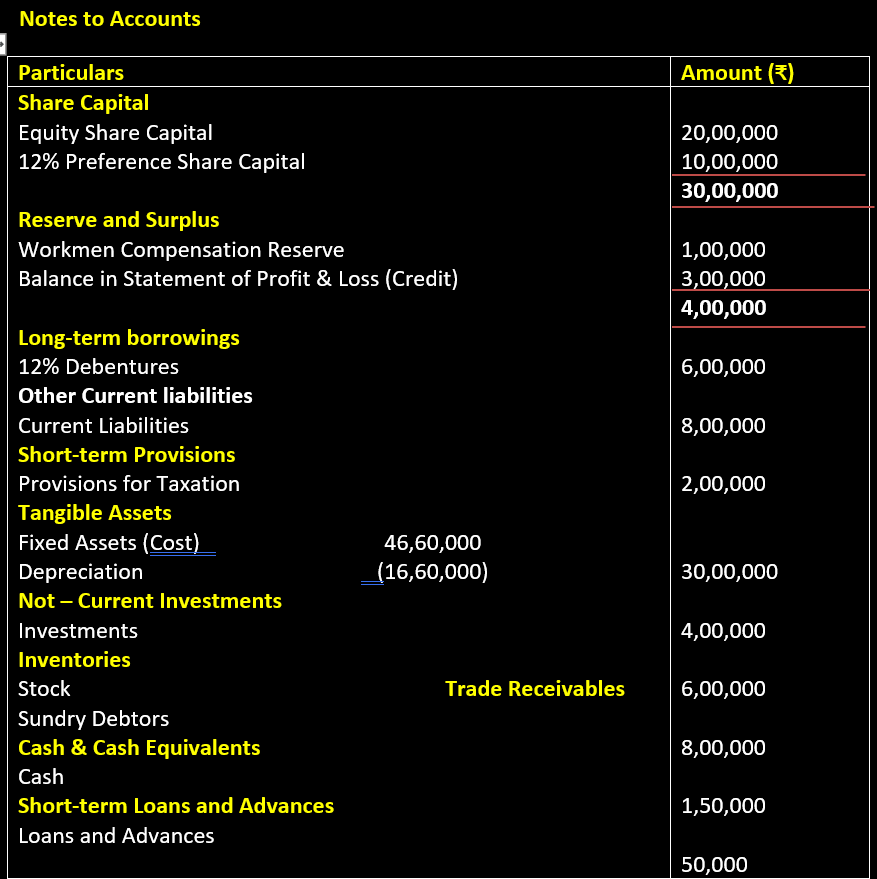

25.

26. From the following information extracted from the books of Howrach Ltd., prepare Balance Sheet of the company as at 31st March, 2025 as per Schedule III of the Companies Act, 2013:

Revenue from Operations and Other Incomes

27.Under which head following revenue items of a non-financial company will be shown:

- Sales;

- Revenue from Services Rendered;

- Sale of Scrap;

- Interest Earned on Loans; and

- Gain (Profit) on Sale of Investment?

Ans.:-

Revenue from Operation:

- Sales;

- Revenue from Services Rendered;

- Sale of Scrap;

Other Income:

- Interest Earned on Loans;

- Gain (Profit) on Sale of Investments.

Cost of Materials Consumed

28.Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials Rs.5,00,000; Purchase of Materials Rs.25,00,000; and Closing Inventory of Materials Rs.4,00,000.

Ans.:-

Cost of Material Consumed = Opening Inventory of Material + Purchases of Materials – Closing Inventory of Materials

= 5,00,000 + 25,00,000 – 4,00,000

= 26,00,000

Cost of Materials Consumed is Rs.26,00,000.

29.Calculate Cost of Materials Consumed from the following:

Opening Inventory Materials Rs.3,50,000; Finished Goods Rs.75,000; Stock-in-Trade Rs.2,00,000; Closing Inventory Materials Rs.3,25,000; Finished Goods Rs.85,000; Stock-in-Trade Rs.1,50,000; Purchases during the year: Raw Material Rs.17,50,000; Stock-in-Trade Rs.9,00,000.

Ans.:-

Cost of Material Consumed = Opening Inventory of Materials + Purchases of Materials – Closing Inventory Materials

= 3,50,000 + 17,50,000 – 3,25,000

Cost of Materials Consumed = Rs.17,75,000

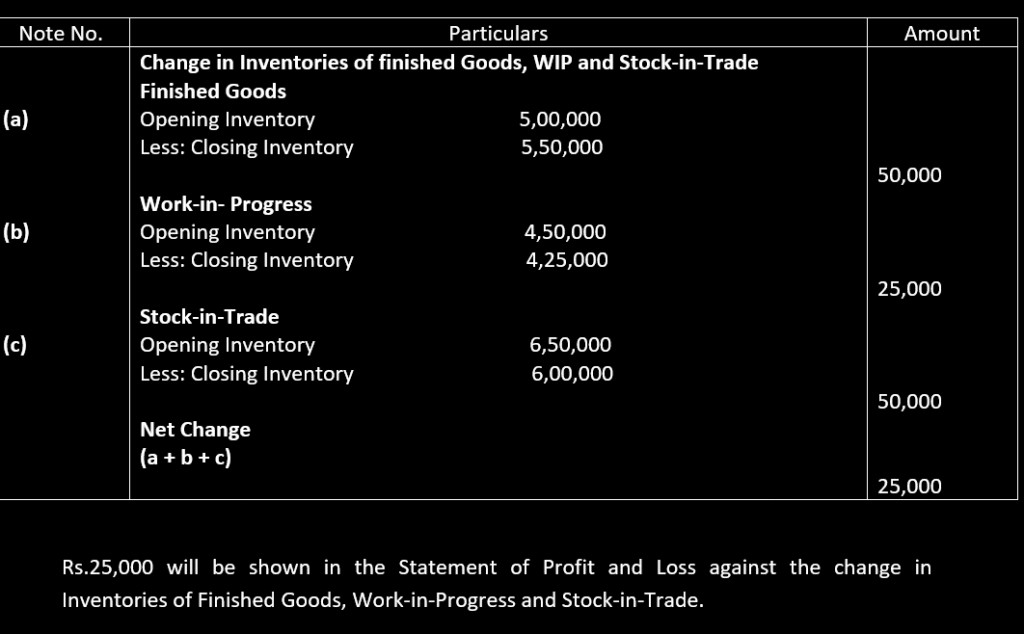

Changes in Inventories of Finished Goods, Work-in-Progress and Stock-in-Trade

30.

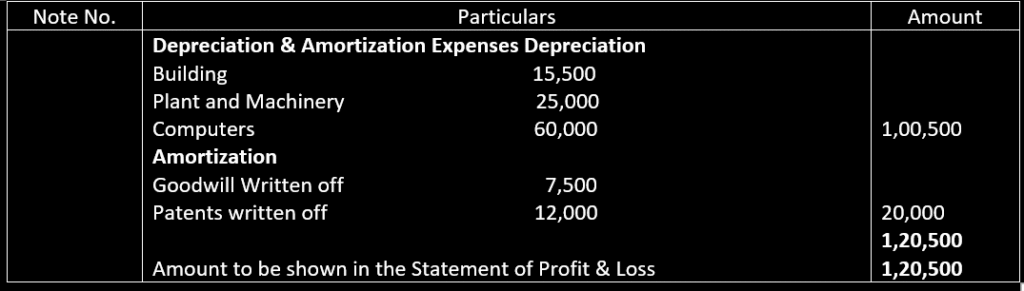

Depreciation and Amortization Expenses

31.From the following information of Best Marketing of Best Marketing Ltd., for the year ended 31st March, 2025, prepare Note to Accounts on Depreciation and Amortization Expenses:

Depreciation on: building Rs.15,500; Plant and Machinery Rs.25,000; Computers Rs.60,000; Goodwill written off Rs.7,500; Patents written off Rs.12,500.

Ans.:- Notes to Accounts

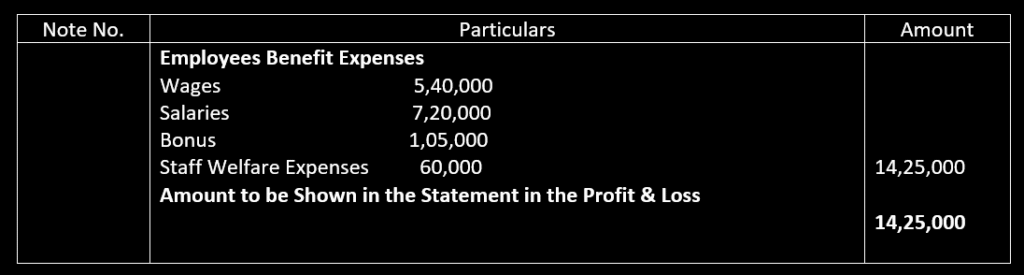

32.Employees Benefit Expenses

From the following information compute the amount to be shown in Note to Accounts on Employees Rs.60,000; and Business Promotion Expenses Rs.50,000.

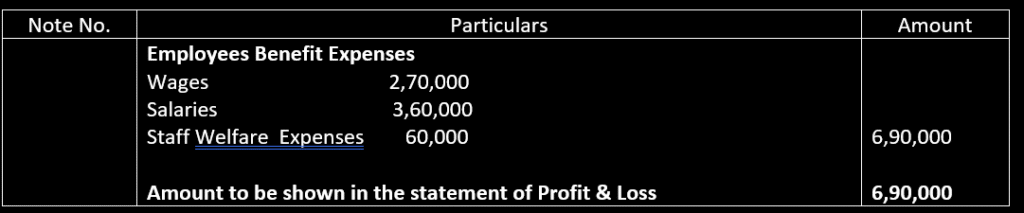

33. From the following information prepare Note to Accounts on Employees Benefit expense

Wages Rs.2,70,000; Salaries Rs.3,60,000; Staff Welfare Expenses Rs.60,000; Printing and Stationery Expenses Rs.20,000 and Building Promotion Expenses Rs.50,000.

Ans.:- Notes to Accounts